.avif)

Your mortgage doesn't have to remain frozen in time, locked into the terms you accepted when you first bought your home. Life changes, financial situations evolve, and market conditions shift—yet many homeowners continue making the same monthly payment on the same loan structure year after year, unaware that refinancing could save them thousands of dollars or help them achieve important financial goals. Whether you're seeking lower monthly payments, wanting to pay off your home faster, or looking to tap into your home's equity, mortgage refinancing offers powerful opportunities to optimize your largest monthly expense.

This comprehensive guide demystifies mortgage refinancing, walking you through everything from fundamental concepts to strategic decision-making frameworks that help you determine whether refinancing serves your financial interests—and if so, how to execute it successfully for maximum benefit.

What Is Mortgage Refinancing?

At its essence, refinancing means replacing your existing mortgage with a completely new loan. The new mortgage pays off your current one entirely, and you begin making payments on the new loan under different terms—potentially with a new interest rate, different loan duration, changed monthly payment amount, and possibly even a new lender.

Think of refinancing as hitting the reset button on your mortgage. Everything about your original loan disappears, replaced by this new agreement that reflects current market conditions, your improved financial profile, or your evolved priorities. You're not modifying your existing loan; you're obtaining an entirely new one that happens to pay off the old one as its first order of business.

The process resembles your original home purchase in many ways. You'll submit a formal application, provide extensive financial documentation, undergo credit checks, have your property appraised, satisfy underwriting requirements, and eventually close on the new loan. The main difference is that you already own the home—refinancing simply changes the financing structure rather than changing ownership.

Why Homeowners Choose to Refinance

Homeowners pursue refinancing for various strategic reasons, each tied to specific financial objectives:

Capturing Lower Interest Rates: When market interest rates decline below what you're currently paying, refinancing locks in those improved rates. Even reductions of 0.5-1% translate to substantial monthly savings and dramatically reduced total interest paid over the loan's lifetime. On a $300,000 mortgage, a 1% rate reduction saves approximately $175 monthly—$2,100 annually—and tens of thousands over the loan's full term.

Shortening Loan Terms for Faster Payoff: Homeowners whose incomes have increased often refinance from 30-year to 15-year or 20-year mortgages. While monthly payments increase, you own your home much faster, build equity dramatically more quickly, and save enormous amounts on total interest charges by compressing the repayment timeline.

Converting Adjustable to Fixed-Rate Mortgages: Adjustable-rate mortgages (ARMs) offer attractive initial rates but carry uncertainty about future payments when adjustment periods arrive. Refinancing into fixed-rate mortgages provides payment stability and predictability, eliminating anxiety about potential rate increases that could strain your budget.

Accessing Home Equity Through Cash-Out Refinancing: Your home's equity represents accumulated wealth that can be accessed through cash-out refinancing—borrowing more than your current balance and receiving the difference as cash. This provides funds for major renovations, high-interest debt consolidation, education expenses, or other significant needs, typically at interest rates far below credit cards or personal loans.

Eliminating Private Mortgage Insurance: Borrowers who made down payments below 20% typically pay PMI monthly. Once home values appreciate and equity reaches 20% or more, refinancing eliminates this requirement, freeing up $100-300 monthly that provides zero borrower benefit.

The Refinancing Process: What to Expect

Understanding the refinancing journey helps you prepare properly and navigate each phase confidently. The typical timeline spans 30-50 days from application to closing, though streamlined programs for government-backed loans sometimes process faster.

Preparation Phase: Before applying, clarify your refinancing objectives. Are you seeking lower payments, shorter terms, payment stability, or cash access? Your goal shapes every subsequent decision. Check your credit score and review reports for errors. Research current interest rates across multiple lenders. Calculate your home's current value and equity position. Gather required documentation including pay stubs, tax returns, bank statements, and current mortgage details.

Application and Rate Lock: Submit your formal application providing all financial information. Within days, you'll receive a Loan Estimate detailing proposed terms, rates, and costs. Decide whether to lock your interest rate for a specific period (typically 30-60 days) or float your rate hoping for further decreases—though floating carries risk if rates increase instead.

Processing and Underwriting: A loan processor reviews your application for completeness and accuracy, requesting additional documentation as needed. Your lender orders a professional appraisal to confirm property value and verify sufficient equity. An underwriter then conducts deep analysis of your financial profile—credit history, income, assets, debts—to assess risk and make the final approval decision. This phase typically consumes one to three weeks and represents the longest part of the timeline.

Closing and Funding: Once approved, you receive a Closing Disclosure at least three business days before your closing appointment, listing all final terms and costs. At closing, you sign documents and pay any closing costs not rolled into the loan. For primary residence refinances, you have a three-day right of rescission allowing you to cancel without penalty. After this period expires, your new lender pays off the old mortgage and your new loan officially begins.

Calculating True Costs and Benefits

Refinancing involves substantial closing costs—typically 2-6% of your loan amount, or $6,000-$18,000 on a $300,000 mortgage. These expenses include appraisal fees, origination charges, title insurance, credit report fees, and various administrative costs.

The critical calculation is your break-even point: how long it takes monthly savings to recover these upfront costs. Divide total closing costs by your expected monthly savings. If costs are $9,000 and you'll save $225 monthly, you break even after 40 months—just over three years. If you plan to remain in your home substantially beyond this point, refinancing makes financial sense. If you might move before break-even, refinancing costs exceed benefits.

However, don't stop at monthly payment comparisons. Calculate total interest paid over your current mortgage's remaining life versus total interest under proposed refinancing over the new loan's complete term. Sometimes lower monthly payments mask higher lifetime costs due to extended loan terms. Model complete scenarios to understand true long-term financial implications rather than just surface-level monthly changes.

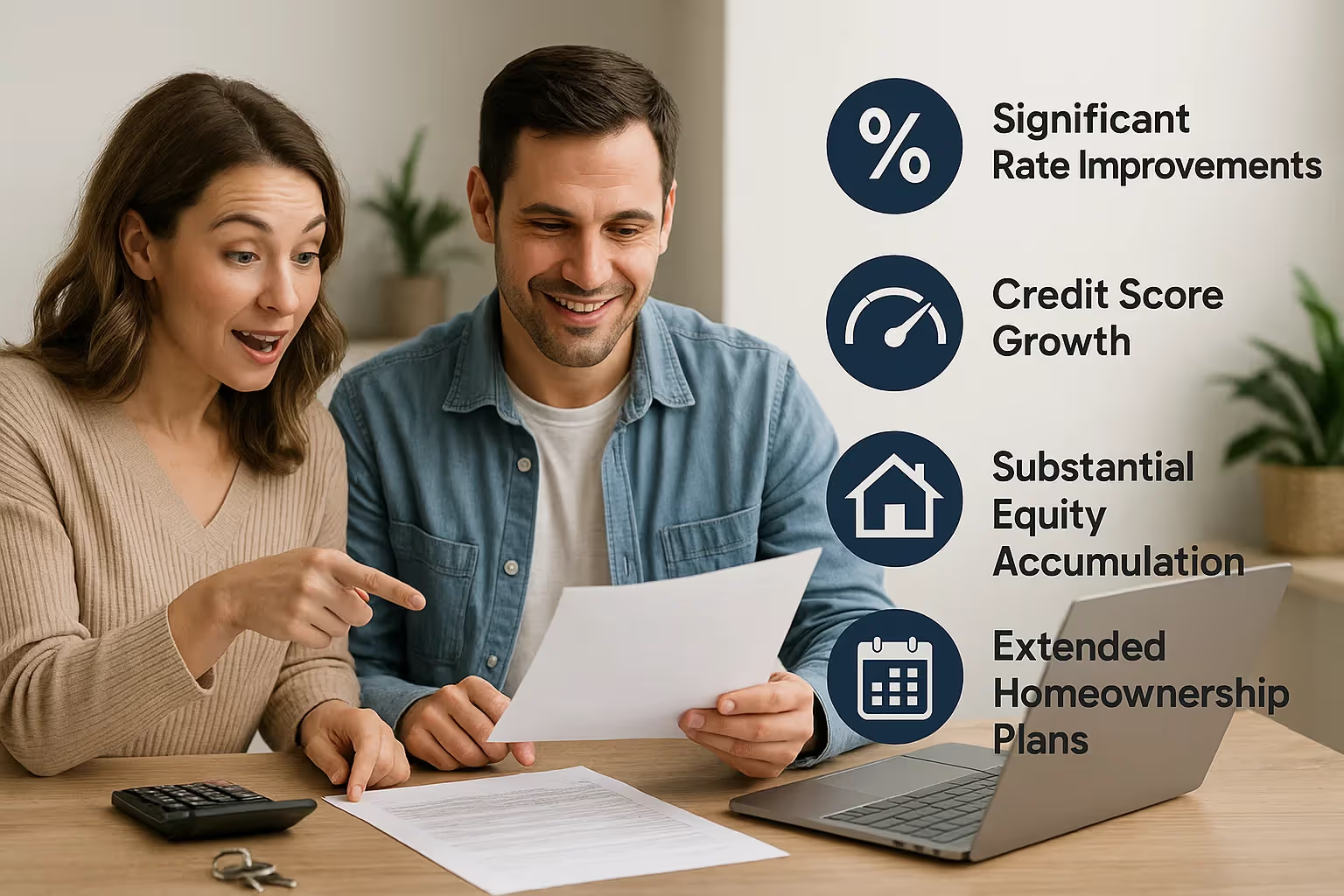

When Refinancing Makes Strategic Sense

Certain circumstances create particularly compelling refinancing opportunities:

Significant Rate Improvements: Market rates at least 0.75-1% below your current rate typically justify refinancing, especially with larger loan balances where even modest rate reductions generate substantial monthly savings that quickly recover closing costs.

Credit Score Growth: If your score has increased 50+ points since you originally financed—perhaps from 670 to 730—you now qualify for better rate tiers previously unavailable. This credit improvement alone might justify refinancing even if market rates haven't changed dramatically.

Substantial Equity Accumulation: Building equity to 20% or more through appreciation and principal payments allows refinancing to eliminate PMI, potentially saving hundreds monthly. Additional equity also improves loan-to-value ratios, unlocking better refinancing terms.

Extended Homeownership Plans: Homeowners confident about remaining in their properties for five or more years have ample time to recover closing costs through monthly savings, making refinancing attractive when other factors align favorably.

Life Stage Transitions: Career advancement supporting higher payments might motivate refinancing to shorter terms. Approaching retirement could prompt refinancing to eliminate mortgage debt before income decreases. These life changes create refinancing motivations beyond simple rate improvements.

When Refinancing Doesn't Make Sense

Sometimes maintaining your current mortgage proves wiser than refinancing despite apparent opportunities:

Short Remaining Timeline: Planning to move or sell within 2-3 years rarely provides sufficient time to recover closing costs through monthly savings, making refinancing economically questionable.

Minimal Rate Improvements: Rate reductions below 0.5% typically don't generate enough savings to justify refinancing costs and effort unless you have exceptionally large loan balances.

Recent Refinancing: If you refinanced within the past 12-24 months, refinancing again means paying closing costs twice in short succession—expensive churning that rarely delivers net benefits.

Late-Stage Mortgages: Homeowners with only 5-8 years remaining have crossed the amortization inflection point where payments now substantially reduce principal rather than paying interest. Refinancing resets this progress and may cost more despite lower rates.

Financial Instability: During job transitions, income uncertainty, or financial stress, committing to new mortgage terms introduces risk precisely when flexibility matters most.

Maximizing Refinancing Success

To extract maximum value from refinancing:

Shop Multiple Lenders Aggressively: Obtain detailed quotes from at least three to five different institutions including traditional banks, credit unions, and online mortgage companies. Compare Annual Percentage Rates (APRs) that incorporate fees rather than just interest rates for accurate cost comparison.

Calculate Complete Financial Scenarios: Model total interest paid over complete loan terms, not just monthly payment changes. Understanding lifetime costs reveals whether apparent savings are genuine or illusory due to extended repayment periods.

Negotiate Terms and Fees: Use competing offers as leverage to negotiate better rates or reduced fees. Many lenders have flexibility on origination charges even if rates are fixed—don't accept first offers without attempting negotiation.

Time Your Application Strategically: While predicting rate bottoms proves impossible, refinancing when rates have dropped meaningfully below your current rate—even if they might decline slightly further—often proves wiser than waiting indefinitely for perfect timing that may never arrive.

Respond Promptly to Lender Requests: During processing, underwriters will likely request additional documentation or clarification. Quick responses keep refinancing on schedule while delays jeopardize rate locks or create complications.

Making Your Refinancing Decision

Determining whether refinancing serves your interests requires moving beyond generic rules toward comprehensive analysis of your unique situation. Calculate your specific break-even point honestly. Model complete cost scenarios over realistic timeframes. Assess your homeownership timeline realistically rather than optimistically. Evaluate your financial stability and income security.

When analysis reveals clear financial benefits—meaningful monthly savings, substantial lifetime interest reduction, strategic equity access, or important payment stability—that justify closing costs within your realistic timeline, proceed with confidence. When analysis reveals marginal benefits, extended break-even periods, or uncertain circumstances that complicate long-term commitments, maintaining your current mortgage often proves wiser than pursuing refinancing that might not deliver promised value.

Remember that refinancing is always optional. Unlike mortgage payments that arrive monthly regardless, refinancing happens only when you initiate it. This gives you control over timing and terms, allowing you to wait for truly compelling opportunities rather than accepting mediocre improvements simply because they're available.

Conclusion

Mortgage refinancing represents a powerful financial optimization tool that rewards strategic deployment and punishes careless use. The difference between successful refinancing that delivers substantial value and disappointing refinancing that costs more than it saves lies entirely in thorough preparation, comprehensive analysis, honest self-assessment, and disciplined execution focused on long-term value rather than short-term convenience.

By understanding how refinancing works, when it makes strategic sense, and how to execute it effectively while avoiding common pitfalls, you transform your mortgage from a static obligation into a dynamic financial tool supporting wealth building, cash flow optimization, and accelerated achievement of financial goals. Your home loan doesn't have to remain unchanged from purchase through payoff—strategic refinancing ensures it evolves with your financial growth and market opportunities, delivering maximum value throughout your homeownership journey.

Approach refinancing decisions with clear eyes, accurate information, and realistic expectations. Calculate comprehensively, shop competitively, and align decisions with genuine financial improvement rather than surface appeal. When circumstances truly favor refinancing and you execute it thoughtfully, the savings and benefits compound into significant financial advantages supporting the secure, prosperous future you're working to build.

Alex Chen

Alex Chen

Get in touch with a loan officer

Our dedicated loan officers are here to guide you through every step of the home buying process, ensuring you find the perfect mortgage solution tailored to your needs.

Options

Exercising Options

Selling

Quarterly estimates

Loans

New home

Manténgase siempre actualizado sobre artículos y guías interesantes.

Todos los lunes, recibirás un artículo o una guía que te ayudará a estar más presente, concentrado y productivo en tu vida laboral y personal.

.png)

.png)

.png)

.avif)

.avif)

.avif)

.png)

.png)

.png)

.avif)

.png)

.png)

.png)

.avif)

.png)

.avif)

.avif)

.avif)

.avif)

.avif)

.avif)