Breaking Down the Numbers: The Financial Mathematics of Mortgage Refinancing

November 19, 2025

.png)

For most homeowners, the decision to refinance their mortgage feels more emotional than analytical. Marketing messages promise savings, friends share success stories, and rate announcements create urgency. Yet beneath these surface impressions lies a mathematical reality that determines whether refinancing genuinely serves your financial interests or merely shifts costs around without delivering meaningful value.

This guide strips away the emotions and marketing hype, focusing instead on the hard numbers, calculations, and financial analysis that should drive every refinancing decision. By understanding the mathematics behind mortgage refinancing, you'll be equipped to evaluate opportunities objectively, calculate true costs and benefits accurately, and make decisions based on facts rather than feelings or fear of missing out.

The Core Refinancing Equation

Every refinancing decision ultimately boils down to a simple question: do the long-term financial benefits exceed the upfront costs within my realistic ownership timeline? Answering this question requires understanding three critical numbers:

Your Monthly Savings: Calculate the difference between your current monthly principal and interest payment and what your new payment would be after refinancing. If you currently pay $2,100 monthly and refinancing reduces this to $1,850, your monthly savings equal $250. This number drives your break-even calculation and determines how quickly you recover closing costs.

Your Total Closing Costs: Refinancing involves substantial expenses typically ranging from 2-6% of your loan amount. On a $300,000 mortgage, expect $6,000-$18,000 in costs including appraisal fees ($400-600), origination charges (0.5-1% of loan amount), title insurance ($500-1,500), credit reports ($30-50), and various administrative fees. Get detailed estimates from lenders showing every fee rather than accepting vague ranges that might hide unexpected costs.

Your Break-Even Timeline: Divide total closing costs by monthly savings to determine how many months of payments are needed to recover upfront expenses. If closing costs total $9,000 and monthly savings are $250, you break even after 36 months—three years. This timeline must fall comfortably within your planned homeownership duration for refinancing to make financial sense.

Understanding Total Interest Calculations

Monthly payment comparisons tell only part of the refinancing story. The complete picture requires calculating total interest paid over your loan's entire life—both your current mortgage and the proposed refinance.

Current Mortgage Total Interest: Your remaining balance multiplied by your interest rate and remaining term reveals how much interest you'll pay if you maintain your current mortgage. Use online amortization calculators or spreadsheets to model this precisely. For example, a $280,000 balance at 7.25% interest with 23 years remaining will cost approximately $258,000 in total interest over the loan's remaining life.

Refinanced Mortgage Total Interest: Model the same calculation for your proposed refinance—new loan amount (including any rolled-in closing costs), new interest rate, and new loan term. If you refinance that $280,000 balance to 6.5% for 20 years with $8,000 in closing costs rolled into the loan ($288,000 total), you'll pay approximately $208,000 in total interest over the new loan's life.

The Real Savings: Subtract the refinanced total interest from the current total interest to reveal genuine long-term savings. In this example, $258,000 minus $208,000 equals $50,000 in interest savings over the loan's life—substantial value that justifies the refinancing decision despite $8,000 in upfront costs.

The Hidden Cost of Term Extensions

One of the most misunderstood aspects of refinancing involves loan term resets. Many homeowners focus exclusively on lower monthly payments without recognizing that extending their loan term dramatically increases total interest paid—sometimes exceeding any savings from rate reductions.

Consider a homeowner who purchased five years ago with a 30-year mortgage at 7% interest. They've paid diligently and now have 25 years remaining on a $320,000 balance. Current rates have dropped to 6.5%, creating an apparent refinancing opportunity.

Scenario 1: Maintaining 25-Year Term: Refinancing to a 25-year mortgage at 6.5% reduces their monthly payment from approximately $2,130 to $2,150—essentially no change because they're maintaining their current remaining term. However, the 0.5% rate reduction saves approximately $40,000 in total interest over 25 years. After $8,000 in closing costs, net savings equal $32,000—genuine value despite minimal monthly payment change.

Scenario 2: Resetting to 30-Year Term: Refinancing to a new 30-year mortgage at 6.5% drops monthly payments dramatically—from $2,130 to $2,020, saving $110 monthly. This looks attractive on the surface and creates immediate cash flow relief. However, the extended term adds five years of payments (60 additional months at $2,020 equals $121,200 in extra payments) that obliterate interest savings from the rate reduction. Total interest paid actually increases by approximately $15,000 compared to maintaining the current mortgage, making this refinancing financially detrimental despite lower monthly payments.

This example illustrates why monthly payment reductions don't automatically signal beneficial refinancing. Always calculate total interest over complete loan lives to understand whether apparent savings are real or illusory.

The Amortization Reality

Mortgage amortization—how payments split between interest and principal over time—profoundly affects refinancing value calculations that many homeowners overlook.

Early mortgage payments go predominantly toward interest, with minimal principal reduction. As loans age, this ratio gradually shifts until later payments reduce principal substantially while interest portions shrink. This creates an inflection point typically occurring 15-18 years into 30-year mortgages where you've finally crossed from interest-heavy to principal-heavy payments.

Homeowners who've paid mortgages for 10-15 years have made significant progress toward this inflection point. Refinancing resets the amortization schedule, putting them back at the beginning where interest dominates each payment. Even with lower rates, this reset means subsequent payments build equity more slowly than they would have under the original mortgage's remaining amortization.

Calculate the principal reduction in your next 12 months of payments under both your current mortgage and a proposed refinance. If your current mortgage would reduce principal by $18,000 over the next year while the refinance would only reduce it by $14,000 due to amortization reset, you're sacrificing $4,000 in equity building despite lower rates—a hidden cost that might not justify refinancing depending on your priorities.

Cash-Out Refinancing Mathematics

Cash-out refinancing introduces additional complexity because you're simultaneously changing loan terms and increasing your debt. The mathematics require evaluating whether the interest rate on extracted cash justifies using your home as collateral.

Suppose you owe $250,000 on your mortgage at 7% interest with 22 years remaining. Your home is worth $450,000, providing $200,000 in equity. You're considering cash-out refinancing to extract $50,000 for debt consolidation while securing a 6.75% rate.

Your New Loan: $300,000 at 6.75% for 20 years equals approximately $2,290 monthly—$150 more than your current $2,140 payment on the smaller balance despite the lower rate. You've received $50,000 cash (minus closing costs of $9,000, netting $41,000) but increased your monthly obligation and total mortgage debt.

The Justification Analysis: This makes financial sense only if the $50,000 eliminates debt costing more than 6.75% interest. If you're consolidating $50,000 in credit card debt at 22% average interest (costing approximately $11,000 annually in interest), converting it to mortgage debt at 6.75% (costing approximately $3,375 annually) saves $7,625 yearly in interest charges—substantial savings that justify the increased mortgage payment and reduced equity.

However, if you're extracting cash for discretionary spending or purposes that don't eliminate higher-cost debt or generate returns exceeding 6.75%, you're simply increasing your debt burden without corresponding financial benefit—mathematics that don't support cash-out refinancing regardless of improved rates.

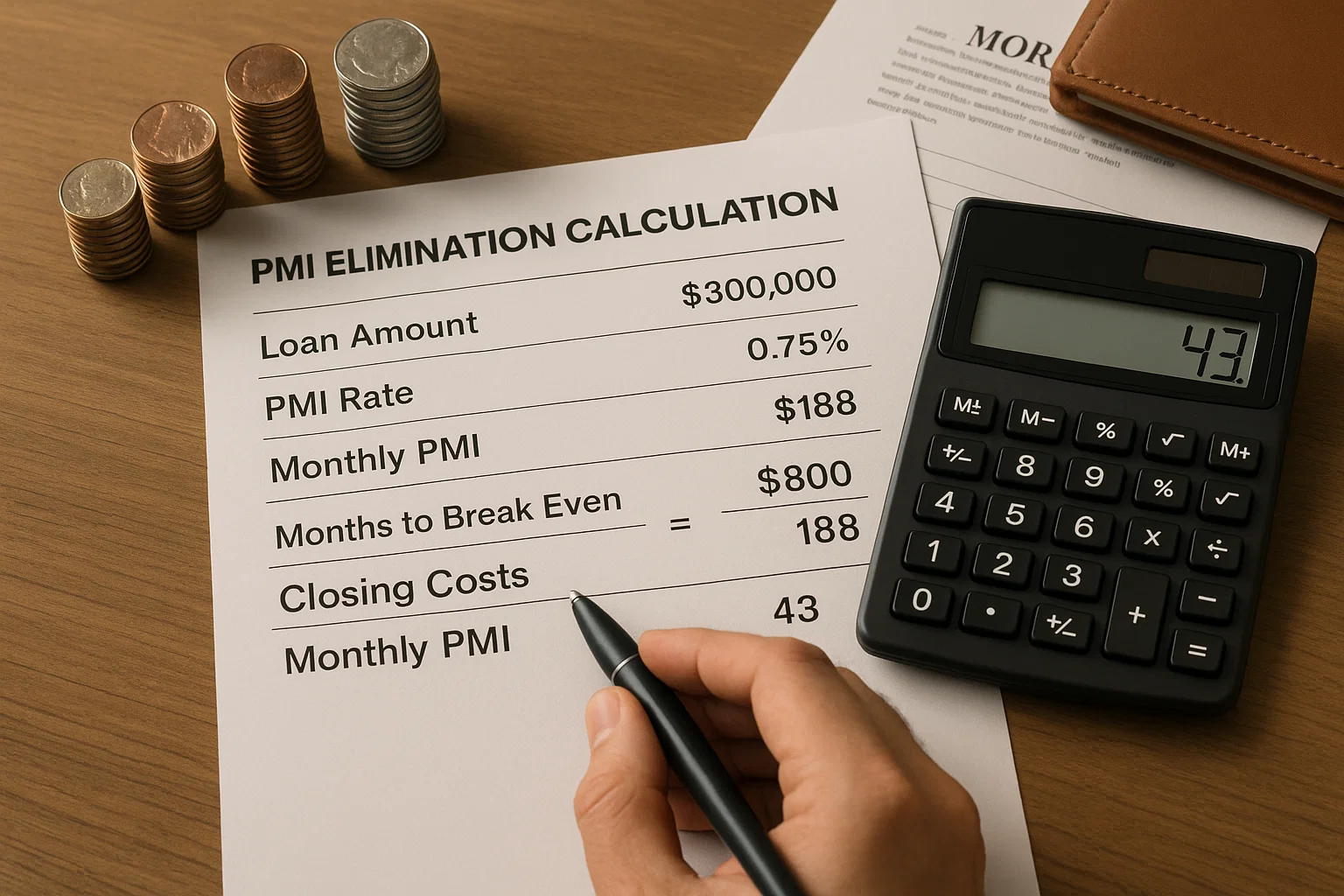

The PMI Elimination Calculation

For homeowners paying private mortgage insurance, elimination through refinancing creates immediate monthly savings that might justify refinancing even without rate improvements.

PMI typically costs 0.3-1.5% of the loan amount annually, translated into monthly premiums. On a $300,000 loan at 0.75% PMI, you're paying $2,250 annually or approximately $188 monthly for insurance that provides zero borrower benefit—it simply protects the lender against default risk.

Once equity reaches 20% through appreciation and principal payments, refinancing eliminates PMI requirements. Calculate whether PMI savings alone justify closing costs: if PMI costs $188 monthly and closing costs total $8,000, you recover these expenses through PMI elimination in approximately 43 months—less than four years. Any additional savings from rate reductions represent pure bonus benefits beyond PMI elimination.

Some lenders allow PMI removal without full refinancing once equity hits 20%, requiring only updated appraisals and administrative processes costing $500-1,000. Compare this option against full refinancing to determine which delivers better value. If you can eliminate PMI for $800 versus $8,000 in refinancing costs, the simpler approach makes more sense unless rate improvements or other benefits justify the additional expense.

Rate Improvement Thresholds

Financial experts traditionally suggested refinancing only when capturing rate reductions of 1-2% or more. Modern analysis reveals this rule oversimplifies refinancing mathematics and prevents beneficial refinancing in some situations while encouraging questionable refinancing in others.

The actual threshold depends on your loan balance, closing costs, and timeline. Large loan balances make smaller rate improvements worthwhile because even modest percentage reductions translate to substantial dollar savings:

Large Balance Example: A $500,000 mortgage at 7% interest costs approximately $3,326 monthly. Refinancing to 6.5% reduces this to $3,160—saving $166 monthly or nearly $2,000 annually. With $12,000 in closing costs, you break even in 72 months (six years). If you plan to remain in your home for 10+ years, this 0.5% improvement delivers roughly $20,000 in net savings after recovering closing costs—worthwhile refinancing despite failing the traditional 1% rule.

Small Balance Example: A $150,000 mortgage at 7% interest costs approximately $998 monthly. Refinancing to 6% reduces this to $899—saving $99 monthly or $1,188 annually. With $4,500 in closing costs, you break even in 45 months (less than four years). However, a full 1% rate improvement saves only $1,188 annually—modest absolute savings despite meeting the traditional percentage threshold.

The mathematics reveal that absolute dollar savings matter more than percentage improvements. Calculate your specific break-even timeline and ensure it falls comfortably within your planned homeownership duration rather than following generic percentage rules that might not apply to your situation.

Opportunity Cost Analysis

Every dollar spent on refinancing closing costs represents capital unavailable for alternative uses—an opportunity cost that sophisticated financial analysis must consider.

If closing costs total $10,000, compare refinancing returns against alternative uses for that capital:

Investment Alternative: $10,000 invested in a diversified portfolio averaging 8% annual returns grows to approximately $21,589 over 10 years. Compare this against cumulative refinancing savings over the same period. If refinancing saves $175 monthly, 10 years equals $21,000 in savings—similar to investment returns. Factor in risk differences: refinancing savings are guaranteed while investment returns fluctuate, potentially favoring refinancing's certainty.

Debt Elimination Alternative: $10,000 applied to credit card debt at 20% interest eliminates approximately $2,000 in annual interest charges—substantially more than typical refinancing monthly savings. If holding high-interest consumer debt, paying it off directly might deliver better financial outcomes than refinancing your mortgage, even with favorable rate improvements.

Emergency Fund Building: If lacking adequate emergency reserves, using $10,000 to build a six-month expense cushion provides financial security that prevents future debt accumulation—potentially more valuable than marginal refinancing savings that leave you vulnerable to unexpected expenses.

This opportunity cost analysis ensures you're deploying capital optimally rather than reflexively choosing refinancing simply because it's available without considering superior alternatives.

The Final Calculation: Net Present Value

Sophisticated refinancing analysis employs net present value (NPV) calculations that account for the time value of money—recognizing that savings received years from now are worth less than savings received today.

NPV refinancing analysis discounts all future cash flows (monthly savings over the loan's life) back to present value using an appropriate discount rate, then subtracts upfront costs. Positive NPV indicates beneficial refinancing; negative NPV suggests maintaining your current mortgage serves you better.

While NPV calculations require financial calculators or spreadsheet tools, the concept is straightforward: $200 saved monthly for 20 years equals $48,000 in nominal savings. However, discounted at 4% annually (a reasonable discount rate reflecting inflation and alternative investment returns), the present value of those savings equals approximately $32,800. Subtract $8,000 in closing costs for $24,800 in net present value—substantial positive NPV that supports refinancing.

This analysis provides the most sophisticated view of refinancing value, accounting for factors that simple break-even calculations ignore.

Conclusion: The Numbers Don't Lie

Mortgage refinancing mathematics provide objective truth in a landscape often dominated by emotions, marketing, and social pressure. By focusing on concrete calculations—break-even timelines, total interest comparisons, amortization impacts, opportunity costs, and net present values—you strip away uncertainty and make decisions grounded in financial reality.

The numbers don't guarantee perfect outcomes—unexpected life changes, market shifts, or personal circumstances can alter plans. However, thorough mathematical analysis ensures your refinancing decision makes sense based on what you know today and reasonable assumptions about tomorrow, dramatically increasing the likelihood of beneficial outcomes that deliver genuine value rather than disappointment masked by attractive marketing messages.

Before refinancing, do the math. Calculate comprehensively, model completely, and ensure the numbers support your decision rather than hoping they work out after you've already committed. When the mathematics genuinely favor refinancing and your circumstances align with beneficial execution, proceed with confidence knowing your decision rests on solid analytical foundation rather than wishful thinking or fear of missing out.

Alex Chen

Alex Chen

Get in touch with a loan officer

Our dedicated loan officers are here to guide you through every step of the home buying process, ensuring you find the perfect mortgage solution tailored to your needs.

Options

Exercising Options

Selling

Quarterly estimates

Loans

New home

Stay always updated on insightful articles and guides.

Every Monday, you'll get an article or a guide that will help you be more present, focused and productive in your work and personal life.

.png)

.png)

.png)

.avif)

.avif)

.avif)

.png)

.png)

.png)

.avif)

.png)

.avif)

.png)

.avif)

.png)

.avif)

.avif)