Can I Refinance a Home Equity Loan? Your Guide

November 19, 2025

Thinking 'can I refinance a home equity loan?' Learn how to lock in a better rate, adjust your terms, and improve your cash flow with our expert guide.

Of course. Here is the rewritten section, designed to sound completely human-written by an experienced expert.

Yes, you can absolutely refinance a home equity loan. It’s a move homeowners make all the time. Essentially, you're just swapping out your current home equity loan for a brand new one, usually to get a better deal.

Think of it like refinancing your primary mortgage or even trading in your car lease. If a better offer comes along that saves you money or fits your life better, you take it.

Why Would You Refinance a Home Equity Loan?

Refinancing your home equity loan isn't just about moving numbers around on a spreadsheet; it's a smart financial play. The goal is to put yourself in a better position than you were in with your original loan.

The home equity market is massive—we're talking $24.8 billion in new loans and lines of credit in 2024 alone. A good chunk of that activity comes from people refinancing to take advantage of new opportunities. You can discover more insights about home equity trends to see just how common this is.

When you refinance, you’re either replacing an existing home equity loan or a Home Equity Line of Credit (HELOC) with a new loan. You’re looking for a clear win that wasn't on the table when you first signed the dotted line.

Key Motivations for Refinancing

So, what pushes a homeowner to actually go through the process? It usually boils down to one of a few powerful reasons.

- To get a lower interest rate. This is the big one. If interest rates have dropped since you got your loan, refinancing could slash your monthly payment and save you a ton of money in the long run.

- To switch from a variable rate to a fixed rate. Many people with a variable-rate HELOC get nervous when they see rates creeping up. Refinancing into a fixed-rate home equity loan locks in your payment, giving you predictability and peace of mind.

- To pull out more cash. Has your home's value shot up? A cash-out refinance lets you tap into that new equity. It's a great way to fund a big home renovation, consolidate high-interest debt, or cover another major expense.

- To change your loan term. Maybe you want to pay the loan off faster and can handle a higher payment. Or perhaps you need to lower your monthly bills, and extending the term is the best way to free up cash flow.

The bottom line is this: your financial life from five years ago probably looks very different from your reality today. Refinancing gives you the flexibility to make your debt work for you now, not the other way around. It’s about aligning your loan with your current goals.

Let's break down the most common reasons people decide to refinance in a bit more detail. This table provides a quick look at the main drivers and who benefits most from each scenario.

Key Reasons to Refinance Your Home Equity Loan

Ultimately, whether you're chasing a lower rate, more stability, or extra cash, refinancing is a tool to help you get there. It’s about taking control and making sure your home equity is truly working for you.

When Does it Actually Make Sense to Refinance Your Home Equity Loan?

Timing is everything when it comes to refinancing a home equity loan. Just because you can do it doesn't always mean you should. The smart move is to wait for a clear financial signal that shows you’ll come out ahead.

One of the biggest green lights is a drop in market interest rates. When rates fall, you have a golden opportunity to trade in your old, more expensive loan for a new one with a better deal. This is especially true if you have a variable-rate HELOC and you're watching the prime rate creep up, taking your monthly payments along with it.

To put it in perspective, as of August 2025, the national average rates for home equity loans hovered around 8.23%, with HELOCs close behind at 8.12%. If you can lock in a rate that’s significantly lower than what you’re paying now, you could slash your monthly payment or even pay off your loan faster without feeling the pinch.

Don't Forget the Break-Even Point

Before you jump in, you need to do a little math and figure out your break-even point. This is the moment when the money you've saved from your new, lower interest rate completely covers the closing costs you paid for the refinance.

Closing costs aren't trivial; they typically run between 2% to 5% of your new loan amount. You need to make sure the long-term savings are worth that upfront cost.

Here’s a quick way to calculate it:

- Step 1: Get a solid estimate of the total closing costs from your lender.

- Step 2: Figure out your monthly savings by subtracting the new payment from your old one.

- Step 3: Divide the total closing costs by your monthly savings. That number is how many months it'll take to recoup your expenses.

If you plan on staying in your home long after you’ve hit that break-even point, then refinancing is probably a fantastic financial decision.

It's Not Always Just About the Rate

While snagging a lower rate is the most common reason to refinance, it's not the only one. Sometimes, life just changes, and your loan needs to change with it. Thinking about how a refinance fits into your bigger picture is one of the essential financial planning steps everyone should take.

Refinancing isn't just a numbers game about interest rates. It's about aligning your debt with your life's current needs, whether that means improving cash flow, accessing new equity, or gaining payment stability.

Here are a few other powerful reasons why refinancing might be the right move for you:

- You Need to Lower Your Monthly Payments: If things are a little tight financially, refinancing to a longer loan term can drop your monthly payment and give your budget some much-needed breathing room.

- You Want to Access More Equity: Has your home's value shot up since you took out your original loan? A cash-out refinance lets you tap into that newfound equity, giving you the funds for a major home renovation, college tuition, or another big expense.

- You're Craving Stability: If you’re tired of the unpredictable payments of a variable-rate HELOC, refinancing into a fixed-rate home equity loan can be a game-changer. You'll get a predictable payment that never changes, protecting you from any future rate hikes.

Weighing The Benefits And Potential Drawbacks

Deciding to refinance your home equity loan is a big financial move. Just like any major decision, it’s not all sunshine; there are compelling reasons to do it and a few risks you need to understand.

Getting a clear picture of both sides of the coin is the only way to make sure you’re strengthening your financial footing, not complicating it. Let's walk through what you stand to gain and what you need to watch out for.

The biggest driver for most homeowners is simple: saving money. If interest rates have taken a nosedive since you first got your loan, refinancing could lock in a much lower rate. That one change can slash your monthly payment, free up cash for other goals, and save you thousands over the life of the loan.

Another huge win is swapping uncertainty for stability. If you have a home equity line of credit (HELOC) with a variable rate, you’ve probably felt that anxiety creep in as interest rates climb. Refinancing into a fixed-rate loan stops that rollercoaster, giving you a predictable payment you can count on every single month.

The Upside: What You Stand To Gain

The benefits of a smart refinance are often felt immediately, bringing both financial relief and some much-needed peace of mind. Here are the key advantages on the table:

- Secure a Lower Interest Rate: This is the headliner. A lower rate directly leads to smaller monthly payments and less interest paid over time. It’s the clearest path to savings.

- Get Payment Stability: Switching from a variable-rate HELOC to a fixed-rate loan is a game-changer. It shields your budget from the whims of the market, which is a huge relief.

- Improve Your Monthly Cash Flow: You can do this in a couple of ways—either by snagging that lower rate or by extending your repayment term. Both result in a smaller monthly bill.

For many people, the chance to transform their second mortgage into a more manageable, predictable expense is incredibly appealing. It’s all about making your home’s equity work for you, not against you. To dig deeper, check out our guide on choosing between a home equity loan vs. a refinance to see which strategy truly fits your situation.

The Downside: What To Watch Out For

Refinancing isn't a magic wand, and it’s definitely not a guaranteed win. There are real costs and trade-offs you have to bake into your calculations before jumping in.

The most immediate hurdle? Closing costs.

Closing costs on a refinance typically run between 2% to 5% of the new loan amount. So, on a $50,000 refinance, you could be looking at $1,000 to $2,500 in upfront fees for appraisals, title searches, and loan origination.

These fees can quickly eat up your potential savings if you’re not paying attention. It’s essential to calculate your "break-even point"—the month when your savings finally outweigh the upfront costs.

You also need to be mindful of resetting your loan's clock. If you refinance into a new loan with a longer term, your monthly payment might look great, but you could easily end up paying more in total interest over the long run. And don't forget to check for prepayment penalties on your current loan. Some lenders will hit you with a fee if you pay off your loan ahead of schedule, which can be an unwelcome surprise.

Refinancing Benefits vs Potential Drawbacks

To make things even clearer, let's put the pros and cons side-by-side. This quick comparison can help you see which column carries more weight for your personal financial situation.

Ultimately, the right choice comes down to running the numbers and being honest about your long-term goals. If the math works and the benefits align with your financial plan, refinancing can be a brilliant move.

How to Qualify for a Home Equity Refinance

Before you even start looking at rates, it’s a good idea to know where you stand. What are lenders really looking for? Getting approved to refinance your home equity loan feels a lot like it did the first time around—lenders will want a good, hard look at your overall financial picture to see if you're a safe bet.

Think of it as a financial health screening. Lenders are primarily focused on three big things: your credit history, how much equity you actually have in your home, and whether your income is stable. If you can get these three areas in great shape, you’re setting yourself up not just for approval, but for the best possible deal.

The Power of a Strong Credit Score

The very first thing a lender will pull up is your credit score. It’s their quick-glance summary of how you’ve handled debt in the past. While you might find a lender willing to work with a score in the low 600s, you’ll want to aim higher.

A FICO score of 680 or higher is usually the magic number that unlocks the best interest rates and more flexible loan terms. A strong score tells lenders you’re a reliable borrower, which makes them much more comfortable offering you their best products.

Has your score gone up since you first took out your home equity loan? If so, you're in a fantastic spot. That improvement can directly lead to a lower annual percentage rate (APR), saving you a bundle over the long haul.

Calculating Your Home Equity and LTV

Next up, lenders need to know you have enough skin in the game. Your home's equity is what secures the loan, so they want to see a healthy cushion. The main tool they use to measure this is your loan-to-value (LTV) ratio.

This metric simply compares all the money you owe against your home—your main mortgage plus the home equity loan you’re refinancing—to what your home is currently worth on the market.

Most lenders get comfortable when they see a combined LTV of 85% or less. A lower LTV means less risk for them and a much higher chance of approval for you.

Here’s a quick and easy way to figure out your combined LTV:

- Add up your primary mortgage balance and your current home equity loan balance.

- Divide that total by your home’s most recent appraised value.

- Multiply by 100 to get your percentage.

Let’s say your mortgage is $200,000, your home equity loan is $40,000, and your house is valued at $300,000. Your total debt is $240,000. Divide that by $300,000, and you get an LTV of 80%—right in the sweet spot.

Your Income and Debt-to-Income Ratio

Finally, lenders need to feel confident you can actually afford the new monthly payment without stretching yourself too thin. For this, they’ll calculate your debt-to-income (DTI) ratio. This number compares your total monthly debt payments (think mortgage, car loans, credit cards) to your gross monthly income. The standards for this often mirror general refinance mortgage requirements.

Typically, lenders like to see a DTI ratio below 43% to 45%. A lower DTI proves you have plenty of cash flow to cover all your existing bills plus the new refinanced loan. Be prepared to show consistent, reliable income with pay stubs, W-2s, and tax returns to seal the deal.

Your Step-by-Step Refinancing Roadmap

So, you’re thinking about refinancing your home equity loan? It might sound intimidating, but it’s really just a series of straightforward steps. Think of it less like a mountain to climb and more like a clear path forward.

With the right map, you can navigate the process without any major headaches. Let’s walk through it together, from the initial number-crunching to the day you sign on the dotted line.

Step 1: Assess Your Financial Standing

Before you even start looking at lenders, the first move is a quick financial self-audit. This is your chance to see if refinancing actually makes sense for you and to make sure you’re in a strong position to get a great deal.

Lenders have a pretty standard checklist. Hitting these marks puts you in the driver's seat.

- Your Credit Score: First, pull your credit report. Lenders love to see a score of 680 or higher, as it usually unlocks the best interest rates.

- Your Home Equity (LTV): Next, do a quick calculation of your loan-to-value (LTV) ratio. You’ll want your combined mortgages (your first mortgage plus the new home equity loan) to be 85% or less of your home's value.

- Your Income (DTI): Finally, check your debt-to-income ratio. Keeping your DTI below 43% signals to lenders that you can comfortably manage your monthly payments.

Step 2: Shop for Lenders and Gather Documents

Once you know your numbers are solid, it’s time to find a lender. My best advice? Don't settle for the first offer you get. Rates, fees, and terms can be surprisingly different from one lender to the next.

Make it a goal to get quotes from at least three different places—think banks, credit unions, and even online lenders. While you’re comparing offers, start pulling together your paperwork. Lenders need to verify everything, and having your documents ready to go will seriously speed things up.

Pro Tip: I always tell clients to create a digital "loan folder" on their computer. Scan and save your pay stubs, tax returns, and bank statements there. When a lender asks for something, you can send it over in minutes instead of digging through a file cabinet.

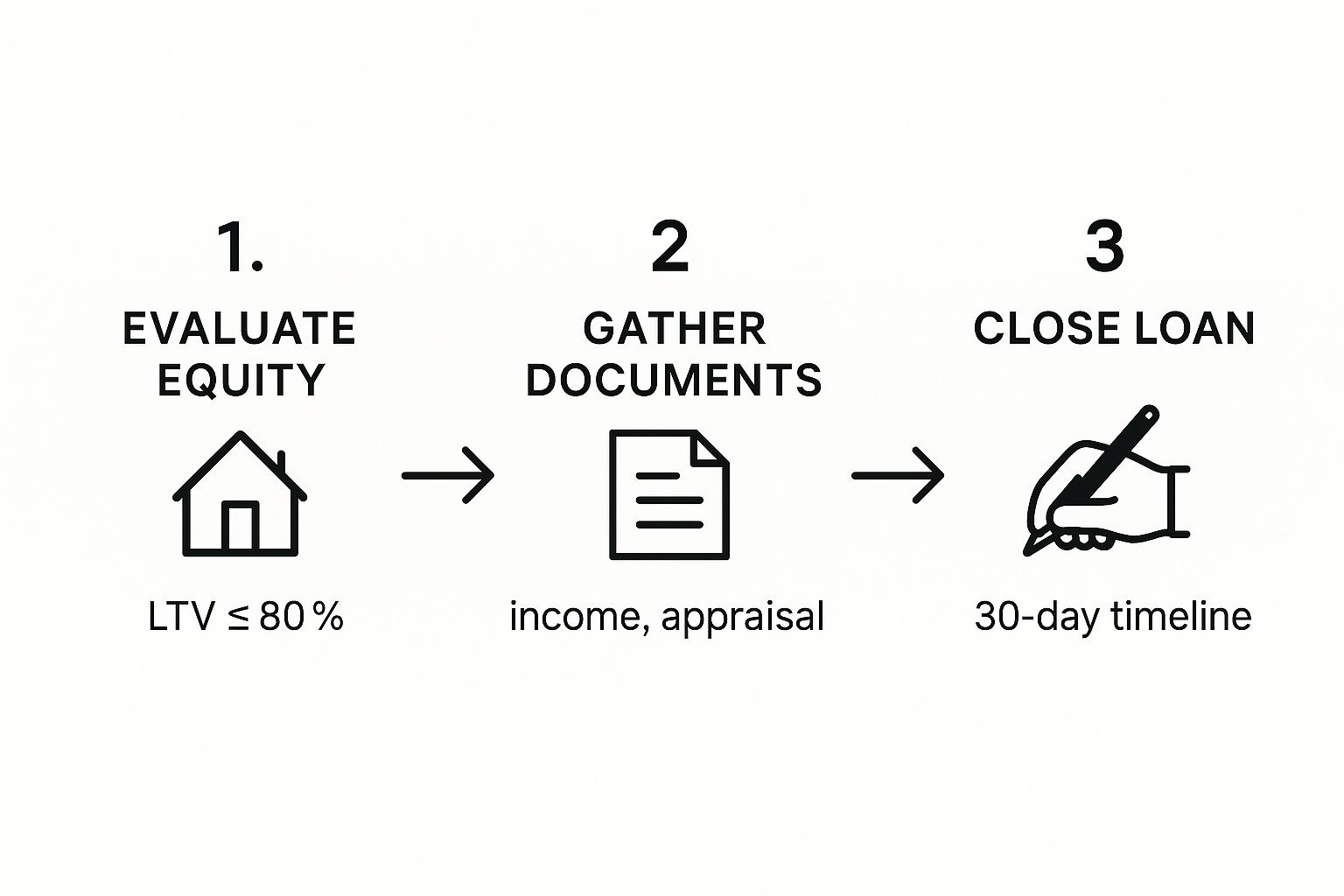

This visual breaks down the key milestones, from checking your equity to closing the deal.

As you can see, the whole process really boils down to having enough equity and getting your documents in order. From there, you're usually looking at about a 30-day timeline to close.

Step 3: Underwriting and Closing

After you’ve applied, your file heads to underwriting. This is where the lender does their due diligence, double-checking all your information and making their final decision. They’ll likely order a new appraisal to get an up-to-date value for your home.

Once you get the green light, you’ll receive a Closing Disclosure. This is a critical document. Read it carefully at least three days before your closing appointment—it details all the final terms of your new loan.

Closing day is the final step. You'll sign the last of the paperwork, cover any closing costs, and just like that, your old loan is paid off. Congratulations, you've officially refinanced

Got Questions About Home Equity Refinancing? We've Got Answers.

Even with all the details laid out, you probably still have a few questions rolling around in your head. That's completely understandable. When you're talking about your home's equity, you want—and need—total clarity before you sign on the dotted line.

Let's dive into some of the most common things homeowners ask when they’re thinking about refinancing a home equity loan.

Can I Refinance a HELOC into a Fixed-Rate Loan?

You bet. In fact, this is one of the smartest and most common reasons people refinance in the first place. If you're over the fluctuating monthly payments that come with a variable-rate Home Equity Line of Credit (HELOC), you can absolutely refinance it into a traditional home equity loan.

Making this move locks you into a fixed interest rate, giving you the same predictable payment month after month. It's the perfect play if you're looking for more stability in your budget and want to sidestep the stress of interest rates creeping up.

How Soon Can I Refinance My Loan?

There's no single, universal rule, but you generally can't close on a loan one day and refinance it the next. Most lenders have what’s called a “seasoning” requirement. This just means they want to see that you’ve been making payments on the original loan for a bit, usually somewhere between six to twelve months.

The more important thing to check? Your original loan agreement for any mention of a prepayment penalty. Some lenders will charge you a fee for paying off the loan too early. You'll want to confirm this detail before you get too far into the process to avoid any nasty financial surprises.

Will Refinancing Hurt My Credit Score?

It will, but the hit is usually small and short-lived. Here’s what happens: when you apply to refinance, lenders will pull your credit report, which results in a hard inquiry. This can knock your score down by a few points.

The good news is that credit scoring models are savvy. They typically recognize when you're rate-shopping and will bundle multiple inquiries for the same type of loan within a short timeframe (like 14-45 days) as a single event.

Once the new loan is on your report, you might see another slight dip. But as you start making consistent, on-time payments, your score will bounce back and can even improve over time. It shows you're a responsible borrower.

Can I Get Cash Out When I Refinance My Home Equity Loan?

Yes, and this can be a fantastic way to tap into your home's increasing value. If your property is worth more now than when you took out the original loan, you've built up more equity you can access.

You can refinance for more than what you currently owe on your home equity loan and pocket the difference as a lump sum of cash. It’s a strategy homeowners use all the time to:

- Fund a major home renovation that boosts the property's value even further.

- Consolidate high-interest debt from credit cards or personal loans into one lower-rate payment.

- Cover big-ticket expenses like college tuition or unexpected medical bills.

Thinking through your "why" is key. For more help, be sure to look over these 10 essential questions to ask before refinancing to make sure you're setting yourself up for financial success.

At Tiger Loans Inc, our job is to give you the clarity and support you need to make smart decisions about your home's equity. Whether you want a lower rate, need to get cash out, or are ready for a fixed payment, our experts are here to walk you through it. Explore your refinancing options with us today!

Alex Chen

Alex Chen

Get in touch with a loan officer

Our dedicated loan officers are here to guide you through every step of the home buying process, ensuring you find the perfect mortgage solution tailored to your needs.

Options

Exercising Options

Selling

Quarterly estimates

Loans

New home

Stay always updated on insightful articles and guides.

Every Monday, you'll get an article or a guide that will help you be more present, focused and productive in your work and personal life.

.png)

.png)

.png)

.avif)

.avif)

.avif)

.png)

.png)

.png)

.avif)

.png)

.png)

.avif)

.png)

.avif)

.png)

.avif)

.avif)