VA Home Loan Closing Costs and Hidden Fees: What Veterans Need to Know.

September 6, 2025

VA home loan closing costs differ significantly from conventional mortgages, with specific fee limitations and prohibited charges that protect veteran borrowers. While the VA loan program offers substantial benefits like no down payment and no private mortgage insurance, understanding the complete cost structure is essential for financial planning. This guide examines allowable closing costs, funding fee calculations, and seller concessions available to veterans navigating the homebuying process with their earned benefits.

.png)

Are you prepared for the actual costs associated with using your VA loan eligibility, beyond just the purchase price of your home? Many veterans are surprised by closing costs and fees that can impact their homebuying budget, even with the significant advantages of veterans home loans. Today we'll break down the complete cost structure of VA loans, including which fees are prohibited, how funding fees are calculated, and strategies for minimizing your out-of-pocket expenses. Understanding these costs upfront can help you budget effectively and avoid surprises at the closing table.

VA-Prohibited and Allowable Closing Costs

VA mortgage regulations include strict limitations on fees that lenders can charge veteran borrowers, providing significant cost protections compared to conventional loans. Prohibited fees include attorney fees for loan preparation, application fees, broker commissions paid by the borrower, and loan processing fees. The VA also prohibits charges for notary fees, administrative fees, and document preparation fees that some lenders attempt to impose on conventional borrowers.

Allowable closing costs include standard items such as appraisal fees, credit report charges, title insurance, and recording fees. Veterans can expect to pay for hazard insurance, property taxes, survey costs if required, and pest inspection fees in certain regions. These legitimate costs typically range from 1% to 3% of the loan amount, significantly lower than many conventional loan scenarios.

The 1% origination fee represents the maximum amount lenders can charge for loan origination services, though many competitive lenders offer lower rates or waive this fee entirely. Veterans should shop around and negotiate these costs, as the VA's fee limitations create a more borrower-friendly environment compared to conventional lending scenarios.

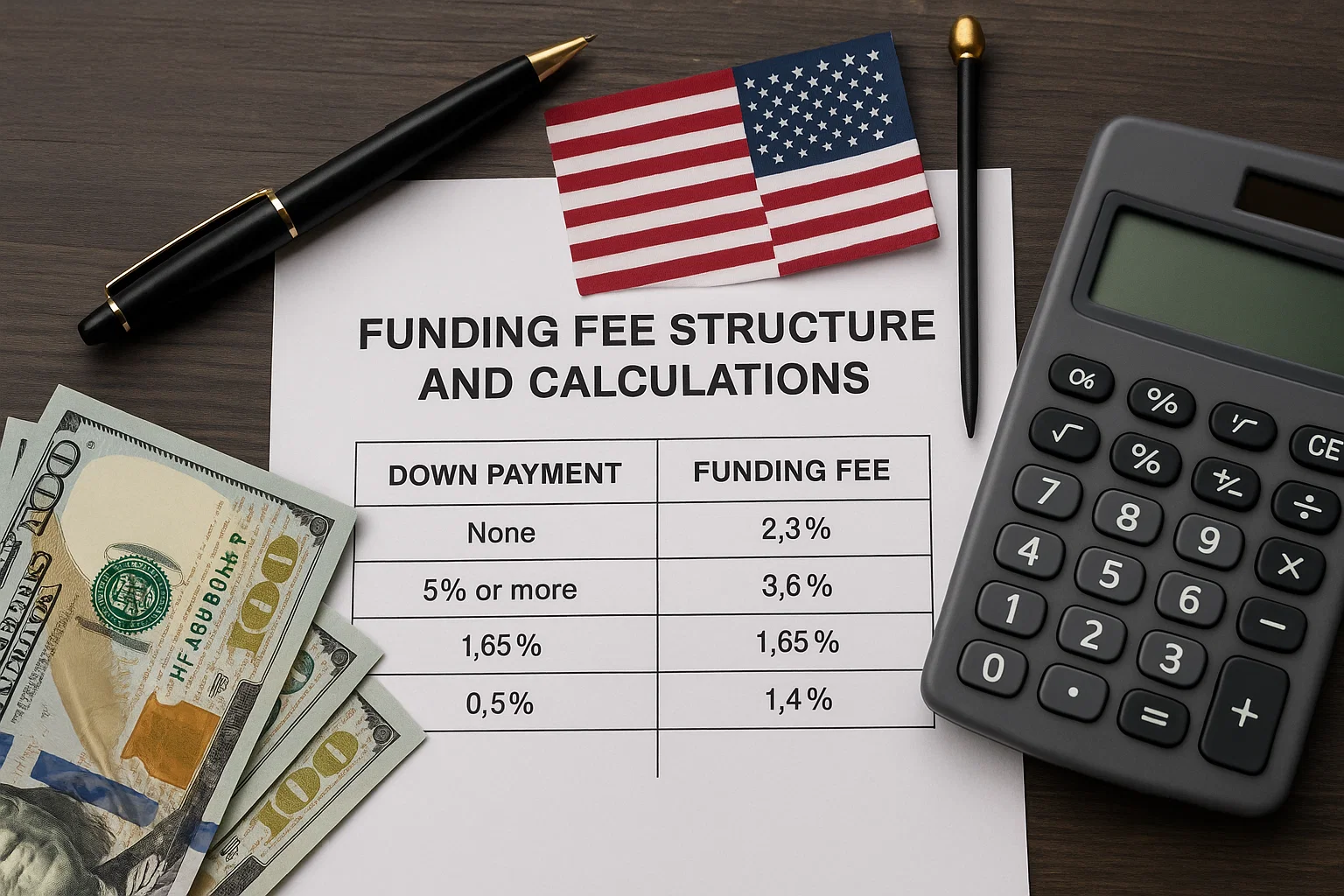

VA Funding Fee Structure and Calculations

The VA funding fee serves as a one-time payment that helps sustain the loan program for future generations of veterans. First-time users typically pay 2.3% of the loan amount for purchase loans with no down payment, while subsequent users face 3.6% funding fees. Making a down payment of 5% or more reduces the funding fee to 1.65% for first-time users and 1.40% for subsequent users.

Refinancing transactions carry different fee structures, with IRRRLs assessed at 0.5% of the loan amount regardless of prior usage. Cash-out refinance loans follow the same structure as purchase loans, with fees varying based on down payment amounts and previous VA loan usage.

Funding fee exemptions apply to veterans receiving VA disability compensation, survivors of veterans who died in service or from service-connected disabilities, and veterans with individual unemployability ratings. These exemptions can save eligible borrowers thousands of dollars, making it crucial to obtain proper VA disability ratings before loan application.

Seller Concessions and Negotiation Strategies

VA loans allow sellers to contribute up to 4% of the home's sales price toward the buyer's closing costs, a more generous allowance than many loan programs offer. These seller concessions can cover allowable closing costs, prepaid items, and even discount points to reduce the interest rate, effectively enabling veterans to purchase homes with minimal out-of-pocket expenses.

Negotiation strategies should focus on maximizing seller contributions while maintaining competitive offer terms. In seller's markets, veterans may need to offer full asking prices or above to secure seller concession agreements, while buyer's markets provide more negotiation leverage for both price and closing cost assistance.

Veterans can also request that sellers pay for property improvements identified during the VA appraisal process, provided these items are required for loan approval. This includes repairs needed to meet VA Minimum Property Requirements, which can otherwise become unexpected buyer expenses.

Regional Variations in Closing Costs

Closing cost amounts vary significantly by geographic location due to differences in local taxes, title insurance rates, and attorney requirements. High-cost areas like California and New York typically have higher title insurance premiums and transfer taxes, while states like Texas may require additional inspections or have higher property tax prorations at closing.

State-specific requirements can impact total closing costs, with some states mandating attorney involvement in real estate transactions while others allow title companies to handle closings. Veterans should research local closing cost norms and obtain detailed Loan Estimates from multiple lenders to understand regional variations.

Property tax prorations and homeowner association fees also vary by location, with some areas requiring substantial upfront escrow deposits while others have minimal prepayment requirements. Understanding these regional differences helps veterans budget appropriately for their specific purchase locations.

Escrow Account Requirements and Prepaid Items

VA loans typically require escrow accounts for property taxes and hazard insurance, though veterans can request escrow waivers in certain circumstances. Initial escrow deposits usually require two to three months of property tax and insurance payments at closing, creating upfront costs that veterans should factor into their budgets.

Prepaid interest calculations depend on the closing date, with closings later in the month requiring more prepaid daily interest charges. Veterans can potentially save money by timing their closings strategically, though this must be balanced against other factors like rate lock expiration dates and move-in timing needs.

Hazard insurance premiums must be paid for the first year at closing, while flood insurance may be required in designated flood zones. These insurance costs can vary significantly based on property location, construction type, and coverage amounts, making insurance shopping an important cost-control strategy.

Cost Comparison with Other Loan Programs

Veterans home loans typically offer lower total closing costs compared to FHA loans and conventional mortgages due to prohibited fees and competitive interest rates. FHA loans require upfront mortgage insurance premiums of 1.75% of the loan amount, while VA funding fees are often lower and can be financed into the loan amount.

Conventional loans with low down payments require private mortgage insurance, adding ongoing monthly costs that VA loans avoid entirely. Over the life of a loan, this PMI savings can amount to tens of thousands of dollars, offsetting higher upfront VA funding fees in most scenarios.

Interest rate advantages on VA loans further enhance their cost-effectiveness, with veterans typically receiving rates 0.25% to 0.50% lower than comparable conventional loans. These rate advantages translate to substantial monthly payment savings and reduced total interest costs over the loan term.

Strategies for Minimizing Out-of-Pocket Costs

Veterans can employ several strategies to reduce closing costs and minimize cash requirements at closing. Shopping multiple lenders helps identify the most competitive origination fees and third-party service costs, while negotiating seller concessions can shift many expenses to the seller.

Timing strategies include applying for loans when interest rates are favorable and scheduling closings to minimize prepaid interest charges. Veterans should also ensure their Certificate of Eligibility is current and complete, avoiding delays that could jeopardize rate locks or purchase contracts.

Disability rating optimization represents a crucial cost-saving strategy, as veterans with service-connected disabilities receive funding fee exemptions worth thousands of dollars. Veterans should work with VA representatives to ensure proper disability ratings are documented before loan application.

VA home loans provide substantial financial advantages for eligible veterans, though understanding the complete cost structure ensures informed decision-making and optimal use of these valuable benefits earned through military service.

Alex Chen

Alex Chen

Get in touch with a loan officer

Our dedicated loan officers are here to guide you through every step of the home buying process, ensuring you find the perfect mortgage solution tailored to your needs.

Options

Exercising Options

Selling

Quarterly estimates

Loans

New home

随时了解有见地的文章和指南。

每周一,你将获得一篇文章或指南,这将帮助你在工作和个人生活中更具活力、更专注和更有成效。

.png)

.png)

.png)

.png)

.png)

.png)

.png)

.png)

.png)

.png)

.png)

.png)

.png)

.png)

.png)

.png)

.png)

.png)

.png)

.png)

.png)

.png)

.png)

.png)