.png)

If you’re a veteran or current service member with a VA home loan, now may be your best chance in years to cut your monthly mortgage costs. The VA IRRRL (Interest Rate Reduction Refinance Loan), also called the VA streamline refinance, is a program built from the ground up for simplicity and savings. In 2025—when every dollar counts—knowing how to use this tool can open the door to newfound breathing room in your budget and greater long-term security.

Have you stayed on top of payments but find your interest rate feels out of touch with the market? Are you wondering if you can skip the long, complicated refi paperwork you hear about from neighbors? The VA IRRRL puts veterans and military borrowers in the driver’s seat, helping you quickly swap your old VA loan for a new one at a better rate, usually with less paperwork than you’d expect with any refinance.

What is VA IRRRL and Who Should Use It?

The VA IRRRL isn’t your average refinance. It exists solely for those who already have a VA loan and want a lower rate, a more predictable payment, or a switch from an adjustable to a fixed rate. No cash-out is allowed—this loan is about streamlining your payment, not tapping home equity for big projects. With a funding fee of only 0.5% (fully waived for those with qualifying disabilities), the IRRRL usually beats the cost and speed of civilian loan options.

If you’ve made your last six VA loan payments on time and want to save on interest or get rid of rate uncertainty, you’re the perfect candidate. Unlike most mortgages, you’ll typically avoid income verification, asset checks, or even a new home appraisal.

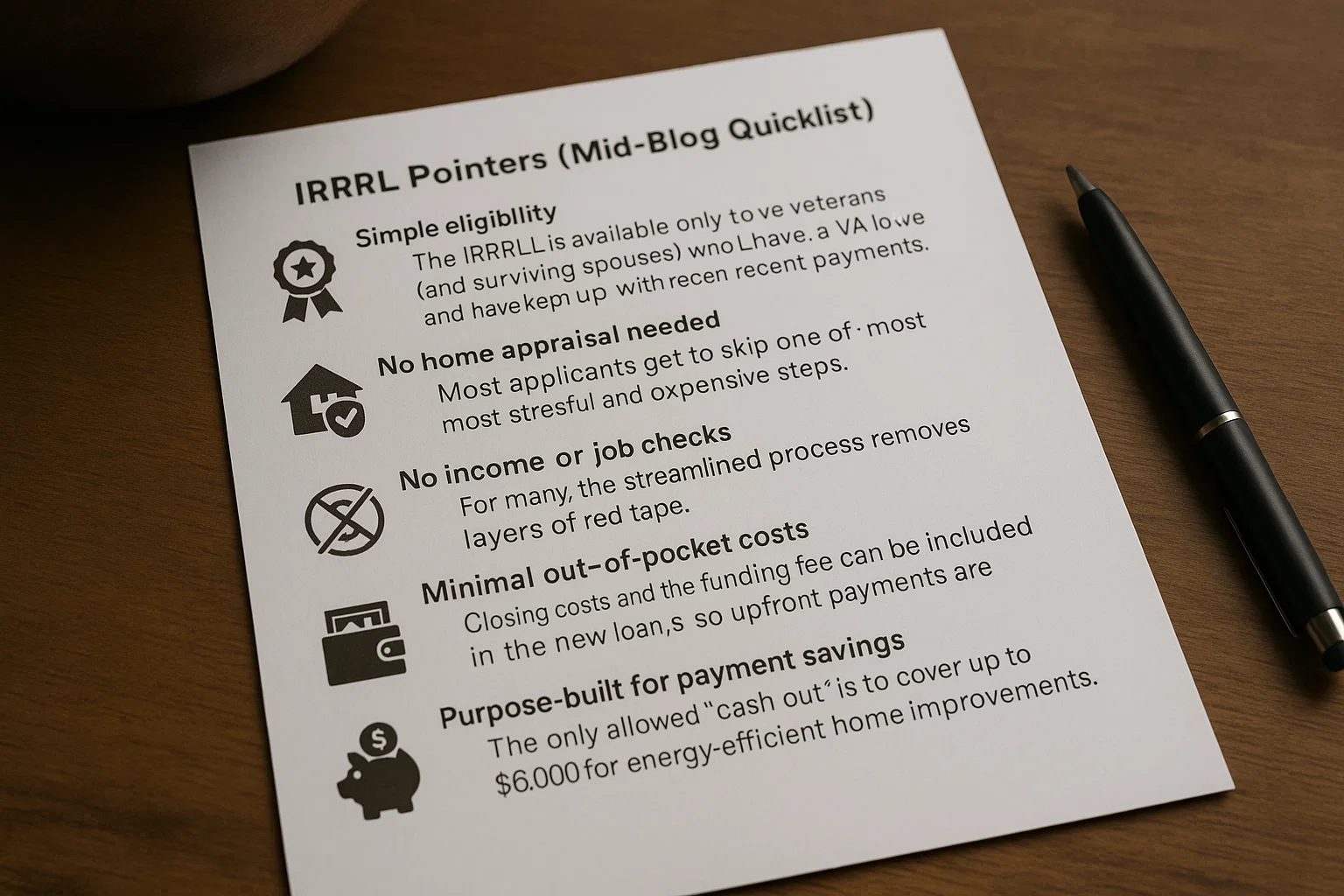

IRRRL Pointers (Mid-Blog Quicklist)

- Simple eligibility: The IRRRL is available only to veterans (and surviving spouses) who currently have a VA loan and have kept up with recent payments.

- No home appraisal needed: Most applicants get to skip one of the most stressful and expensive steps.

- No income or job checks: For many, the streamlined process removes layers of red tape.

- Minimal out-of-pocket costs: Closing costs and the funding fee can be included in the new loan, so upfront payments are rarely needed.

- Purpose-built for payment savings: The only allowed “cash out” is to cover up to $6,000 for energy-efficient home improvements.

How the IRRRL Process Works

- Check Your Rate and Payment History: Compare your current interest rate to today’s VA refi offers and ensure you’ve had no late payments in the past six months.

- Select a VA-Approved Lender: Not all lenders are equal—shop around for lower rates, better service, and the ability to roll in fees where possible.

- Apply and Submit Basic Paperwork: Most borrowers don’t need to provide pay stubs or bank statements. Your lender will order the necessary paperwork and disclosures.

- Close Quickly: With fewer underwriting steps, closing may happen in 2-4 weeks. On closing day, review new payment terms and ensure closing costs are as expected.

- Move Forward with a Lower Bill: Your new monthly payment takes effect. If you chose to include costs in the loan, confirm final balances and new loan details.

With these few steps, many veterans find the IRRRL to be refreshingly efficient compared to their original home purchase or previous refinances.

Advantages—and What IRRRL Can’t Do

Beyond ease, the VA IRRRL is about smart savings. By refinancing into a lower rate or a more stable payment, you keep more money in your pocket, month after month. The funding fee is one of the lowest for any VA product, and for those with service-connected disabilities, it’s often waived entirely. If you’re looking to switch out of an ARM, the security of a fixed-rate IRRRL can be especially valuable in an unpredictable market.

But remember, not everything is on the table. You can’t withdraw extra cash for vacations, cars, or college bills (unless for approved energy improvements), and the IRRRL can’t convert a non-VA or delinquent loan to VA status. The focus is strictly on making your VA-backed mortgage safer and cheaper.

Final Decision Pointers (Pre-Conclusion)

- Break-even period matters: Calculate how many months your new savings will take to “pay back” any refi costs—if you plan to stay in your home at least that long, refinancing is financially sound.

- Compare at least three lenders: Not all lenders offer the same IRRRL rates or service. Shopping around ensures you avoid hidden fees and get the lowest possible payment.

- Check your VA eligibility status: Disabled veterans may qualify for a funding fee waiver—be sure to ask and provide current documentation if eligible.

- Keep your paperwork: After closing, keep all documents and new payment information handy—especially if you plan to sell, refinance, or transfer your home again in the future.

Conclusion: When Simplicity Equals Savings

For veterans, the VA IRRRL in 2025 is a rare chance to simplify your refinance—and finally enjoy the benefits you earned with your service. With lower payments, easier paperwork, and faster turnaround, it’s a refinance designed for real military lifestyles. Don’t let current rates pass you by or struggle with outdated terms: talk to a VA-approved lender, ask about your unique situation, and do the math so your next financial milestone reflects your hard work and future plans.

With just an hour or two of research and lender comparison, you could set yourself up for years of improved cash flow and peace of mind. That’s what the VA IRRRL was created to deliver

Alex Chen

Alex Chen

Get in touch with a loan officer

Our dedicated loan officers are here to guide you through every step of the home buying process, ensuring you find the perfect mortgage solution tailored to your needs.

Options

Exercising Options

Selling

Quarterly estimates

Loans

New home

随时了解有见地的文章和指南。

每周一,你将获得一篇文章或指南,这将帮助你在工作和个人生活中更具活力、更专注和更有成效。

我们的博客

.png)

―

September 27, 2025

.png)

.png)

.png)

.png)

.png)

.png)

.png)

.png)

.png)

.png)

.png)

.png)

.png)

.png)

.png)

―

September 17, 2025

.png)

.png)

.png)

.png)

.png)

.png)

.png)