.avif)

Refinancing your existing loan can be one of the smartest financial moves you make, potentially saving thousands of dollars and providing greater control over your financial future. When done strategically, refinancing allows you to take advantage of lower interest rates, adjust your loan terms to match changing life circumstances, or access your home's equity for important expenses. Many borrowers continue paying their original loan terms without realizing that market conditions, improved credit scores, or better lending options could significantly reduce their monthly obligations and overall interest burden.

The refinancing landscape has evolved dramatically, with competitive lenders offering attractive rates and flexible terms to capture market share. Understanding when to refinance, how to navigate the process efficiently, and which refinancing option best suits your needs can transform your financial outlook. Whether you're struggling with high monthly payments, looking to consolidate debt, or simply want to pay off your loan faster, refinancing provides multiple pathways to achieve your goals. This comprehensive guide explores the strategic aspects of refinancing, helping you make confident decisions that maximize savings and align with your long-term financial objectives.

Key Benefits and Strategic Timing for Refinancing

Lower interest rates and monthly savingsrepresent the most compelling reason to consider refinancing your existing loan. Even a seemingly small reduction in interest rates can translate to substantial savings over your loan's lifetime. When market rates drop 0.75% to 1% below your current rate, refinancing becomes financially attractive:

- Lower monthly EMIs free up cash flow for other financial goals like investments, emergency funds, or children's education

- Reduced interest burden accelerates equity building in your property, strengthening your overall net worth

- Competitive lending environments often bring additional benefits like waived processing fees or reduced prepayment penalties

- A 1% rate reduction on a ₹30 lakh loan can save you several lakhs in interest payments over a 15-20 year period

Improved credit profiles open doors to better refinancing terms that weren't available when you originally secured your loan. If your credit score has improved by 50-100 points since your initial loan approval, you likely qualify for significantly better interest rates. Lenders reward responsible financial behavior—consistent on-time payments, reduced debt-to-income ratios, and longer credit history all contribute to preferential treatment. Additionally, if your property value has appreciated substantially, your improved loan-to-value ratio positions you for more favourable terms, as lenders perceive lower risk when you have greater equity in your property.

Debt consolidation through refinancing offers a strategic approach to managing multiple high-interest obligations. Cash-out refinancing allows you to tap into your home's equity and consolidate credit card debt, personal loans, or other expensive borrowing into your mortgage:

- Credit cards charging 36-42% annual interest can be replaced with home loan rates of 8-12%, resulting in massive interest savings

- Single monthly payment simplifies financial management and reduces the risk of missed payments across multiple accounts

- Extended repayment timelines lower monthly obligations, improving your debt-to-income ratio and overall financial flexibility

- Tax deductibility on home loan interest (subject to applicable limits) provides additional savings not available with other debt types

Loan term adjustments provide flexibility to match your repayment schedule with changing life circumstances and financial goals. Shortening your loan term from 30 years to 15 or 20 years increases monthly payments but dramatically reduces total interest paid and accelerates complete loan payoff. This strategy works particularly well for borrowers who have experienced salary increases, received inheritances, or simply want to eliminate debt before retirement. Conversely, extending your loan term reduces monthly EMI burdens during financially challenging periods like career transitions, medical emergencies, or major family expenses, though this approach increases lifetime interest costs.

Executing Your Refinance Strategy Successfully

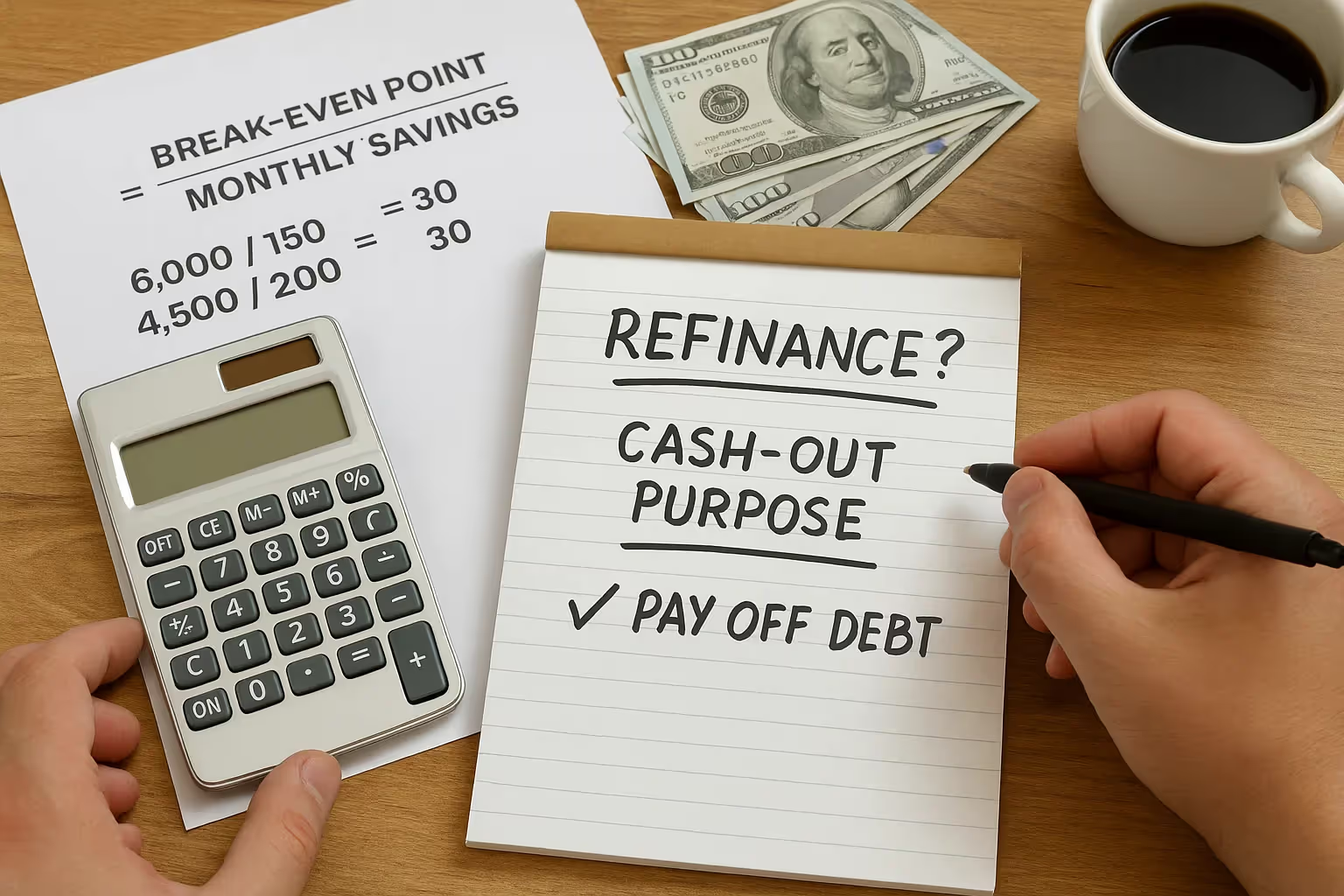

Comprehensive cost-benefit analysis should precede any refinancing decision to ensure the move genuinely improves your financial position. Calculate your breakeven point by dividing total closing costs by monthly savings—if you plan to stay in your property beyond this timeframe, refinancing makes sense:

- Closing costs typically range from 2-5% of your loan amount, including processing fees, valuation charges, legal expenses, and stamp duty where applicable

- Compare all-in costs across multiple lenders rather than focusing solely on advertised interest rates, as hidden fees can erode apparent savings

- Factor in prepayment penalties on your existing loan, which some lenders charge when you close accounts before maturity

- Consider opportunity costs—funds used for closing costs could alternatively be invested elsewhere for potential returns

Documentation preparation and lender comparison streamline the refinancing process and position you for the best possible terms. Start by gathering essential documents including recent salary slips or business financial statements, tax returns, existing loan statements, property documents, and updated credit reports:

- Request loan estimates from at least 3-5 lenders to create competitive pressure and identify the most favorable terms

- Negotiate aggressively on interest rates, processing fees, and prepayment clauses, as lenders often have flexibility beyond published rates

- Check for special programs or promotions targeting refinance customers, which can include cashback offers or waived fees

- Read all terms and conditions carefully, paying particular attention to reset clauses, rate adjustment frequencies for floating loans, and prepayment restrictions

Timing considerations significantly impact refinancing outcomes, making strategic timing essential for maximizing benefits. Monitor interest rate trends and economic indicators that influence lending rates—refinancing during rate-cutting cycles by central banks often yields better terms. Consider your personal timeline as well: refinancing makes more sense earlier in your loan tenure when you're paying predominantly interest rather than principal, as rate reductions have greater impact. Avoid refinancing if you plan to sell your property within 2-3 years, as closing costs may not be recovered through monthly savings. Additionally, ensure your credit score is at its peak before applying—even waiting 3-6 months to improve your score by 20-30 points can result in significantly better rate offers.

Post-refinance financial discipline determines whether you truly capitalize on the benefits refinancing provides. If refinancing reduces your monthly EMI, resist lifestyle inflation and instead redirect those savings toward investments or additional principal prepayments to accelerate loan closure:

- Set up automatic transfers of your monthly savings to investment accounts or emergency funds before you're tempted to spend them

- Make annual or quarterly prepayments using bonuses, tax refunds, or other windfalls to further reduce your outstanding principal

- Monitor your refinanced loan regularly and stay alert for future refinancing opportunities if rates continue declining

- Maintain the financial discipline that improved your credit profile, ensuring continued access to favorable terms for future financial needs

Understanding refinancing mechanics, conducting thorough due diligence, and executing with clear strategic objectives transforms refinancing from a simple transaction into a powerful wealth-building tool. The key lies in recognizing the right timing, comparing comprehensive costs rather than isolated rates, and maintaining disciplined financial habits that compound the benefits of your refinancing decision over time.

Alex Chen

Alex Chen

Get in touch with a loan officer

Our dedicated loan officers are here to guide you through every step of the home buying process, ensuring you find the perfect mortgage solution tailored to your needs.

Options

Exercising Options

Selling

Quarterly estimates

Loans

New home

Manténgase siempre actualizado sobre artículos y guías interesantes.

Todos los lunes, recibirás un artículo o una guía que te ayudará a estar más presente, concentrado y productivo en tu vida laboral y personal.

.png)

.png)

.png)

.avif)

.avif)

.avif)

.png)

.png)

.png)

.avif)

.png)

.png)

.avif)

.png)

.avif)

.png)

.avif)

.avif)

.avif)

.avif)

.avif)

.avif)