.avif)

When homeowners start thinking about ways to reduce their monthly payments or take advantage of lower interest rates, one of the first options that comes to mind is to refinance. However, not all Refinance loans are the same. There are several types designed for different goals - from lowering interest rates to cashing out home equity or changing loan structures.

Choosing the right type of refinance is essential to maximizing your financial benefits and minimizing unnecessary costs. In this article, we’ll break down the major types of Refinance loans, how each works, and when they might be the right choice for you.

What Is a Refinance Loan?

A Refinance loan is a new mortgage that replaces your current home loan. When you refinance, your old mortgage is paid off, and you begin paying under new terms. The goal is usually to secure a lower interest rate, reduce monthly payments, or modify the loan structure to better fit your financial situation.

Whether you’re looking to save money or unlock your home’s value, the right refinance type can make a big difference.

1. Rate-and-Term Refinance

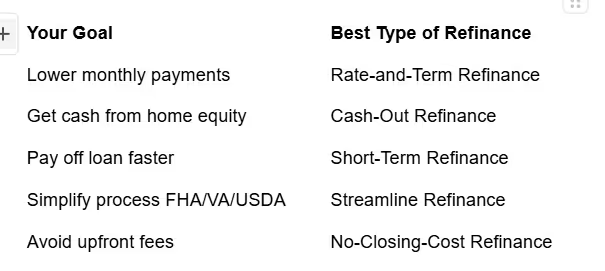

This is the most common type of refinance. A rate-and-term refinance focuses on improving your loan’s interest rate, repayment term, or both - without changing the total amount you owe significantly.

Why homeowners choose it:

- To lower monthly payments by securing a lower interest rate

- To shorten the loan term for example, from 30 years to 15 years

- To switch from an adjustable-rate to a fixed-rate mortgage

If you want to save money and gain stability without tapping into home equity, a rate-and-term Refinance loan is an excellent choice.

2. Cash-Out Refinance

A cash-out refinance allows homeowners to access the equity built up in their home. In this case, you take out a new, larger Refinance loan than what you currently owe, and you receive the difference in cash.

Example:

If your home is worth $400,000 and you owe $250,000 on your mortgage, you could refinance for $300,000. You’d receive $50,000 in cash minus closing costs, which you can use for home improvements, debt consolidation, or personal investments.

Why homeowners choose it:

- To fund major expenses like renovations, education, or medical bills

- To consolidate high-interest debt

- To invest in another property or business opportunity

A cash-out refinance gives you access to liquid cash but increases your loan balance, so it’s best for homeowners confident in their ability to manage slightly higher payments.

3. Cash-In Refinance

The opposite of cash-out, a cash-in refinance involves paying extra money toward your principal when you refinance. This reduces your loan balance and may help you qualify for a lower interest rate or eliminate the need for private mortgage insurance PMI.

Why homeowners choose it:

- To reduce their mortgage balance

- To qualify for a better Refinance loan rate

- To reach 20% equity faster and remove PMI

If you’ve recently received a bonus, inheritance, or other lump sum, a cash-in refinance can be a strategic way to strengthen your long-term financial position.

4. Streamline Refinance

A streamline refinance is designed to make the refinancing process faster and simpler, often requiring less paperwork and no appraisal. These loans are typically available for government-backed mortgages, such as FHA, VA, or USDA loans.

Why homeowners choose it:

- Faster approval process

- Minimal documentation and lower closing costs

- No need for a new appraisal in some cases

If you already have a government-backed mortgage and want to reduce your rate quickly, a streamline refinance may be ideal. However, it usually doesn’t allow cash-out options.

5. FHA Refinance

An FHA refinance is backed by the Federal Housing Administration. It’s suitable for homeowners who initially used an FHA loan or who may not have perfect credit but still want to refinance.

There are different FHA Refinance loan options:

- FHA Rate-and-Term Refinance – to lower interest rates or change terms

- FHA Streamline Refinance – fast approval for current FHA borrowers

- FHA Cash-Out Refinance – allows access to home equity

This type of refinance is especially beneficial for borrowers with limited credit history or lower credit scores.

6. VA Refinance

A VA refinance is available to eligible veterans, active-duty service members, and surviving spouses. It’s supported by the U.S. Department of Veterans Affairs.

Two major VA Refinance loan types exist:

- VA Streamline Refinance IRRRL – simplifies the process for those with an existing VA loan

- VA Cash-Out Refinance – allows veterans to tap into their home equity

Benefits:

- No private mortgage insurance

- Competitive interest rates

- Low or no down payment requirements

For qualified veterans, a VA refinance can be one of the most cost-effective ways to save money or access funds.

7. USDA Refinance

The USDA refinance is designed for rural homeowners with USDA-backed loans. Like FHA and VA programs, USDA Refinance loans often feature simplified requirements and lower costs.

Why homeowners choose it:

- Reduced interest rates for rural borrowers

- Streamlined documentation

- Affordable refinancing options for moderate-income families

If your home is in an eligible rural area, a USDA refinance could be the key to lowering your payments and improving your loan terms.

8. No-Closing-Cost Refinance

In a no-closing-cost refinance, the lender covers the upfront fees or rolls them into your loan. While this reduces immediate expenses, it may lead to slightly higher interest rates or a larger total balance over time.

Why homeowners choose it:

- To avoid paying thousands upfront

- To make refinancing accessible without saving for fees

It’s an excellent short-term solution if you need quick relief but plan to refinance again later or sell your home within a few years.

Choosing the Right Refinance Loan

Selecting the best Refinance loan depends on your goals:

Before deciding, review your credit score, income stability, and future plans. Compare lenders, calculate closing costs, and ensure that the benefits of refinancing outweigh the expenses.

Final Thoughts

A Refinance loan can be one of the smartest tools for improving your financial situation, but choosing the right type is key. Whether you’re looking to lower your rate, unlock cash, or simply update your loan structure, understanding your refinance options helps you make an informed decision.

Always take time to compare offers, read the fine print, and consult a trusted loan advisor before finalizing your decision. The right refinance at the right time can save you money, build equity, and bring you closer to true financial freedom.

Alex Chen

Alex Chen

Get in touch with a loan officer

Our dedicated loan officers are here to guide you through every step of the home buying process, ensuring you find the perfect mortgage solution tailored to your needs.

Options

Exercising Options

Selling

Quarterly estimates

Loans

New home

Manténgase siempre actualizado sobre artículos y guías interesantes.

Todos los lunes, recibirás un artículo o una guía que te ayudará a estar más presente, concentrado y productivo en tu vida laboral y personal.

.png)

.png)

.png)

.avif)

.avif)

.avif)

.png)

.png)

.png)

.avif)

.png)

.png)

.avif)

.png)

.avif)

.png)

.avif)

.avif)

.avif)

.avif)

.avif)

.avif)