Your Guide to Bank Statement Loans

November 19, 2025

Unlock your mortgage with bank statement loans. Our guide explains how self-employed borrowers can secure financing by proving real cash flow. Learn more.

Bank statement loans are a game-changer for entrepreneurs and self-employed professionals. Instead of relying on traditional tax returns and W-2s, these loans let you prove your income using your actual cash flow, typically verified through 12 to 24 months of bank statements.

The Key to Homeownership for Entrepreneurs

Think of it this way: a conventional mortgage is like trying to open a high-tech lock that only accepts one specific key—the W-2 form. If you're a successful freelancer, gig worker, or small business owner, your financial "key" looks different. It just won't fit.

This is where bank statement loans come in. They are the master key. Lenders who offer these loans understand that an entrepreneur's tax return, with all its smart deductions, doesn't tell the whole story. So, they look at what really matters: the actual, consistent cash flowing into your bank account month after month.

A Focus on Cash Flow, Not Tax Deductions

I've seen it happen time and again. Take a successful freelance graphic designer, for instance. She pulls in a healthy six-figure income, but after writing off legitimate business expenses like software, marketing, and her home office, her taxable income on paper looks surprisingly low. Despite a great credit score and a solid down payment, she was turned down for a conventional loan.

The traditional system simply couldn't see past her deductions to the thriving business she had built.

Frustrated but determined, she discovered bank statement loans. Her new lender reviewed 24 months of her business bank statements, saw the consistent, high-volume deposits, and quickly approved her for the home she had been dreaming of. This is precisely why this financing tool is so powerful.

Bank statement loans shift the focus from what you report to the IRS to what you actually earn. They are built for borrowers whose true financial picture isn't captured by a W-2.

This approach recognizes a fundamental truth: for an entrepreneur, maximizing tax deductions is just smart business. It shouldn't lock you out of homeownership. If you're ready to see how your business's real financial strength can get you into a home, you can learn more about specialized bank statement loans and find out if they’re the right move for you.

Bank Statement Loans vs. Conventional Loans at a Glance

To really understand the distinction, it helps to see these two loan types side-by-side. The table below breaks down the core differences, which always circle back to how income is proven and who the loan is designed for.

FeatureConventional LoanBank Statement LoanIncome VerificationW-2s, pay stubs, tax returns12-24 months of bank statementsIdeal BorrowerSalaried employees with stable incomeSelf-employed, freelancers, business ownersFocusAdjusted gross income after deductionsGross deposits and consistent cash flowFlexibilityRigid, standardized requirementsMore flexible, cash-flow based underwriting

As you can see, the path to approval is fundamentally different. While conventional loans follow a strict, standardized checklist, bank statement loans offer a more holistic and realistic assessment of a business owner's ability to afford a home.

Why Alternative Lending Is on the Rise

Bank statement loans aren't just some fringe product anymore. They represent a powerful, necessary answer to a huge shift in how Americans earn a living. The old-school lending model, which was really built for the 9-to-5, W-2 employee, just isn't keeping up with the way people work today.

We're seeing an explosion of entrepreneurship and a booming gig economy. This has created a whole new class of successful professionals—think consultants, freelancers, small business owners, and online creators. These folks are building incredible businesses, but their financial picture doesn't fit neatly into the rigid boxes on a standard mortgage application.

The Limits of Traditional Lending

If you've ever applied for a traditional mortgage, you know it's all about one thing: your tax returns. For anyone self-employed, this immediately creates a conflict. As a smart business owner, you work with your accountant to take every legal deduction you can. It's just good business sense.

The problem? That same savvy strategy shrinks your "on-paper" income, making it look much smaller than the actual cash flowing through your business. It's a frustrating catch-22 where your financial success can actually stand in the way of buying a home. The system is set up to judge you on your post-deduction income, completely missing the real story of your company's health and earning power.

This isn't about finding some loophole. It's about financial innovation finally catching up to how millions of Americans actually work. Bank statement loans are what happen when lenders start treating real cash flow as the true measure of your ability to pay.

This gap in the market created a massive need. Bank statement loans really started gaining steam after the 2008 financial crisis as lending standards got tighter and more flexible solutions were needed. Lenders offering these loans typically want to see at least 12 months of statements. To offset what they see as added risk, the interest rates are often 0.5% to 1.0% higher than a conventional loan. You can dig deeper into these lending trends by checking out the Federal Reserve's Senior Loan Officer Opinion Surveys.

Empowering a New Generation of Homeowners

By shifting the focus to bank statements, lenders get a much clearer, more honest picture of a business's success. They're looking at the consistency and volume of your deposits over 12 or 24 months to figure out what you can genuinely afford for a mortgage payment. This approach simply sidesteps the limitations of a tax return and judges you on your real-world performance.

This is a game-changer for entrepreneurs. It validates their hard work by valuing actual success over standardized paperwork. It’s a recognition that a business owner with strong, reliable cash flow is an excellent candidate for a home loan, no matter what their adjusted gross income says.

The growth in this type of lending also helps a wider range of people. The need for flexible financing isn't limited to just entrepreneurs. For example, it extends to people who might have other documentation hurdles, which is why there's a growing market for things like loans without SSN, as financial products evolve to serve a more diverse population.

Ultimately, the rising popularity of bank statement loans signals a long-overdue evolution in the mortgage industry. They are a vital tool for economic empowerment, opening a realistic path to homeownership for the self-employed people who are driving so much of our economy. They make sure the dream of owning a home is within reach for anyone who can prove their financial success, not just those with a traditional paycheck.

How to Qualify for a Bank Statement Loan

So, how do you actually get one of these loans? Forget about jumping through the typical hoops of a conventional mortgage. Qualifying for a bank statement loan is all about proving your business's real-world financial health. Lenders in this space are like financial detectives; they’re looking for a clear story of stability and success told directly through your cash flow.

Think of your bank statements as your financial resume. They need to show a consistent, reliable income stream that can comfortably handle a new mortgage payment. This is where the underwriting for bank statement loans takes a sharp turn away from traditional lending.

Your entire application really boils down to three key pillars: your bank statements, your credit history, and your down payment. Each one gives the lender a crucial piece of the puzzle, helping them build a complete picture of you as a borrower.

The Power of Your Credit Score

Even though your cash flow is the star of the show, your credit score still plays a vital supporting role. It’s the lender’s shortcut to understanding your history with debt. Most lenders who offer bank statement loans are looking for a credit score of 620 or higher, though some programs have a bit more wiggle room.

A better credit score will almost always unlock better interest rates and terms. If your score is hovering on the lower end, a lender might ask for other strengths to balance things out—like a larger down payment or significant cash reserves. Even with alternative loans, knowing where you stand is crucial. It's easy to how to get your credit reports for free and see what lenders will see.

If you know your credit needs some work, it’s smart to tackle that before you apply. Check out our guide on how to build and maintain good credit for some practical steps. A few months of focused effort can make a huge difference in your loan options and how much you pay over time.

Down Payment Expectations

Because bank statement loans are considered non-qualified mortgages (non-QM), they aren’t backed by the same government guarantees. That means they almost always require a more significant down payment than an FHA or conventional loan. This "skin in the game" reduces the lender's risk and shows them you're serious.

You should be prepared to put down at least 10-20% of the home's purchase price. If you have a lower credit score or some inconsistencies in your bank statements, that requirement could easily climb to 30% or more. Frankly, a larger down payment is one of the most powerful tools you have to strengthen your application.

Scrutinizing Your Bank Statements

This is it—the heart of the entire process. Lenders will dig into 12 to 24 months of your personal or business bank statements to figure out your qualifying income. They’re not just glancing at the deposit totals; they are analyzing the health, rhythm, and consistency of your business.

Lenders aren't just counting your deposits; they're assessing the stability of your income over time. Consistency is more important than a few high-income months.

Here’s exactly what underwriters are looking for:

- Consistent Deposits: They want to see a steady, predictable flow of income. Wild swings from one month to the next can be a red flag that requires a good explanation.

- No Excessive Overdrafts: Frequent non-sufficient funds (NSF) charges are a major warning sign of poor cash management and can quickly derail an application.

- Clear Income Sources: Lenders need to confirm the money is coming from your actual business activities, not from random cash infusions or personal loans from family.

The best thing you can do is get organized ahead of time. Make sure your statements are clean and easy to follow. If you have any large, out-of-the-ordinary deposits, be ready with a letter of explanation and any supporting documents to prove the source. When you present a clear, professional financial story, you make the entire qualification journey smoother and much more likely to succeed.

Weighing the Pros and Cons

So, are bank statement loans the perfect solution? For some people, absolutely. For others, not so much.

Think of it this way: a bank statement loan is a specialized key. It’s not meant for every lock, but for the self-employed borrower who can’t get a traditional mortgage, it can be the only key that opens the door to homeownership.

Making the right choice means getting brutally honest about the good, the bad, and whether it truly aligns with your financial reality. For many entrepreneurs, these loans are a game-changer, offering a path to a home they thought was years away. But that path comes with a few tolls. Let's break them down.

The Clear Advantages of Bank Statement Loans

The biggest win here is simple: access. These loans were created specifically for the millions of successful self-employed individuals, freelancers, and small business owners who are otherwise shut out by the rigid rules of conventional lending.

Beyond just getting your foot in the door, there are some powerful benefits:

- You're Judged on Real Cash Flow: This is the heart of it all. Lenders look at the actual money coming into your business accounts, not the adjusted gross income on your tax returns. It’s a system that understands that smart, legal tax write-offs shouldn't stop you from buying a house.

- A More Accurate Financial Picture: A single tax return can be misleading, especially if your business had a weird year. By looking at 12 to 24 months of statements, lenders see a much more stable and realistic picture of what you actually earn over time.

- A Faster Track to Owning a Home: Why spend years changing how you run your business just to satisfy a bank's narrow criteria? This lets you leverage your success now and start building personal equity sooner rather than later.

For the right person, these advantages make all the difference, turning what would have been a frustrating "no" into a confident "yes."

Bank statement loans don’t just offer a mortgage; they offer validation. They recognize your business's success based on its most honest metric—cash flow—and build a financing solution around that truth.

The Important Drawbacks to Consider

Of course, this kind of flexibility doesn't come for free. When lenders step outside the government-backed, one-size-fits-all mortgage guidelines, they take on more risk. They balance that risk by charging you, the borrower, more. It's crucial to walk into this with your eyes wide open.

The main trade-offs are higher interest rates and bigger down payment requirements. You also won't find these loans at just any bank on the corner. You'll need to seek out a specialized lender who deals in these non-qualified mortgages (non-QM).

To make it crystal clear, here’s a straightforward comparison to help you weigh your options.

Benefits and Drawbacks of Bank Statement Loans

Here's a balanced view of the advantages and potential disadvantages to help you decide if this loan type fits your financial situation.

AdvantagesDisadvantagesDesigned for the Self-Employed: Creates a real path to homeownership for those with non-traditional income.Higher Interest Rates: Expect rates to be 0.5% to 2.0% higher than a comparable conventional loan.Focuses on True Cash Flow: Your business's actual revenue is the basis for qualification, not your post-deduction tax income.Larger Down Payments Required: A minimum of 10-20% is standard, and it can be 30% or more for weaker files.Faster Route to Ownership: Lets you tap into your current business success without waiting years to fit a conventional mold.Fewer Lender Options: Not all banks offer these loans; you need a non-QM specialist.Holistic Financial Review: Lenders get a long-term view of your income stability (12-24 months), not just one year.Deeper Financial Scrutiny: Every deposit will be analyzed to ensure it's legitimate, consistent business income.

Ultimately, choosing a bank statement loan is a strategic business decision. You are trading a higher cost of borrowing for immediate access and flexibility. For many successful entrepreneurs, paying a little more in interest is a small price for the opportunity to lock in their dream home and start building personal wealth for their family.

Your Step-by-Step Application Guide

So, you're ready to make a move on a bank statement loan. It might feel like a daunting path, but I promise, when you break it down into a few key stages, it's a completely manageable process. This is your roadmap—from gathering your documents to finally getting those keys.

At the end of the day, this entire journey boils down to one simple thing: proving your business makes consistent, reliable money. Let's walk through exactly how to do that.

Stage 1: Assemble Your Financial Package

Before you even think about talking to a lender, your first job is to become a financial archivist for your own business. You need to pull together a clean, organized package of documents that tells the story of your success. Trust me, getting this right upfront will make everything that follows go infinitely faster.

Your goal here is to think like an underwriter. Anticipate what they'll ask for and have it ready to go. It shows you're a serious, professional borrower, and that goes a long way.

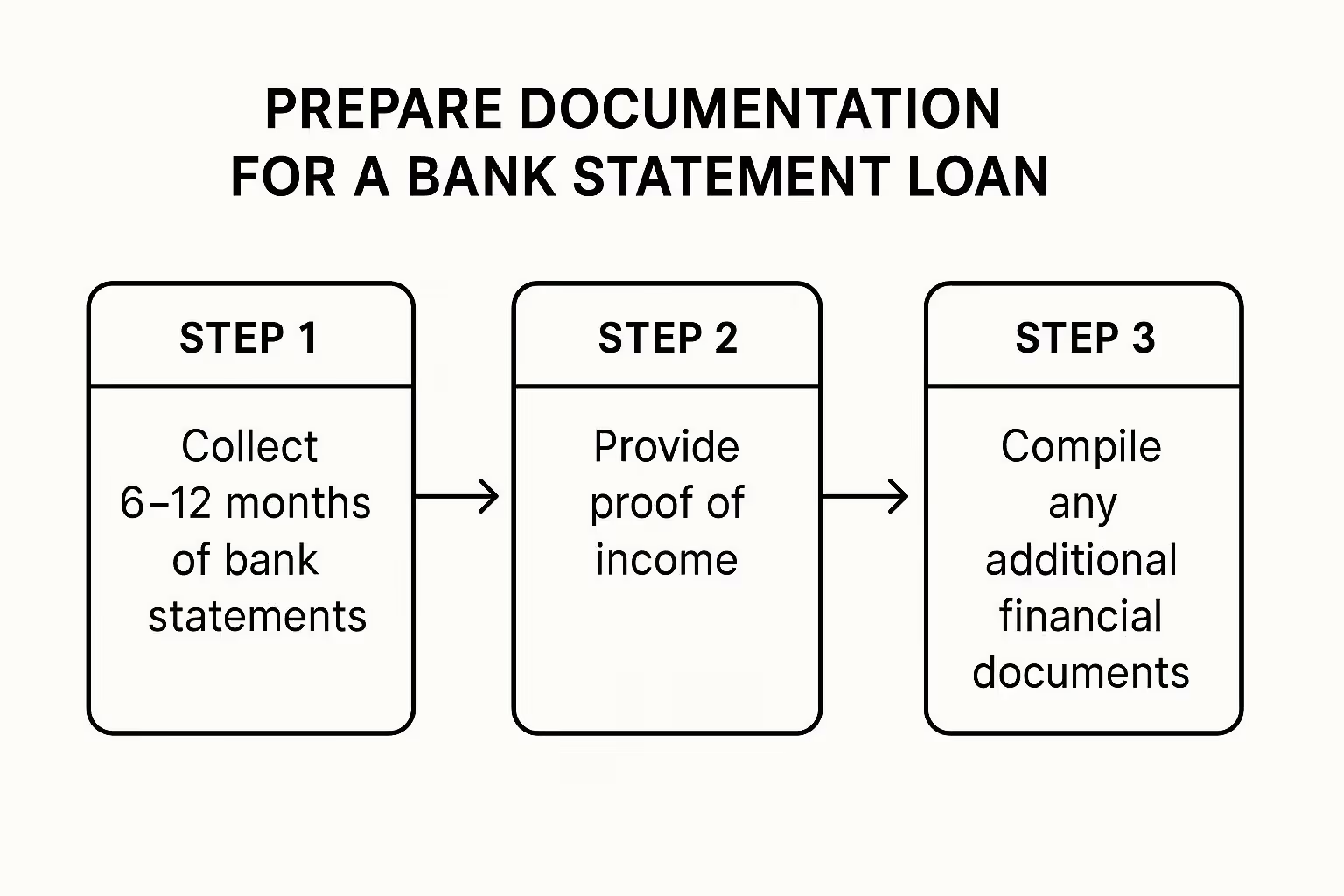

Here’s your essential checklist:

- Bank Statements: You'll need 12 to 24 months of back-to-back statements from your main business account. Some lenders might want to see your personal ones, too. Don't skip a single page.

- Business Licenses and Registration: This is your proof that your business is legitimate and has been up and running for at least two years.

- Profit & Loss (P&L) Statement: While not every lender demands it, a professionally prepared P&L adds a huge layer of credibility. It backs up the numbers you're presenting.

- Identification: A clear, simple copy of your driver’s license or another government-issued ID.

To get a clearer picture of where to start, this graphic lays out the first crucial steps.

As you can see, it all begins with meticulously collecting those bank statements. They're the foundation of your entire application.

Stage 2: Find a Specialist Lender

You’re not going to find bank statement loans advertised at your local big-name bank. These are specialized products, and you need a lender who lives and breathes the world of entrepreneurship. You're looking for a non-QM (non-qualified mortgage) lender or a mortgage broker who has a deep bench of these kinds of loans.

Don't be shy about interviewing potential lenders. This is a massive financial decision, and you need to feel confident they get your situation and have your back.

Pro Tip: When you're talking to lenders, ask them point-blank: "How many bank statement loans did you close last year?" An experienced pro will know that number off the top of their head and be proud to share it.

Arm yourself with a few key questions to really gauge their expertise:

- What's the standard expense factor you use for my industry?

- Do you require a P&L statement prepared by a CPA?

- What’s your typical timeline from application to closing?

How they answer will tell you everything you need to know about their experience and whether they're the right fit.

Stage 3: Navigate the Underwriting Review

Once you’ve submitted your package, it lands on an underwriter's desk. This is the person whose job is to comb through your financial life and give the final thumbs-up or thumbs-down. For bank statement loans, they are laser-focused on one thing: your cash flow. They'll add up your average monthly deposits and then apply an "expense factor" to figure out your qualifying income.

It’s pretty straightforward. For example, if your business deposits average $30,000 per month and the lender applies a 50% expense factor, they’ll qualify you with a monthly income of $15,000. That's the magic number they use to decide how much you can borrow.

Be ready for questions. If the underwriter spots large, one-off deposits—maybe from selling a piece of equipment or a gift from a relative—they're going to ask about it. Have a letter of explanation and any supporting documents ready. Full transparency is your best friend here. Of course, the loan process is just one piece of the puzzle; remember that different financing options come with their own unique hurdles, like the home inspection requirements for VA loan approval, which shows just how much the details can vary.

Stage 4: Reach the Closing Table

When the underwriter gives the "clear to close," you're in the home stretch! This is the final step where you sign all the official loan documents, usually with a notary or at a title company's office. You'll carefully review the Closing Disclosure, which breaks down every final number—your interest rate, monthly payment, and all closing costs.

Once the ink is dry and the funds have been wired, you get the keys. By following this guide, you can confidently turn the success you've built as an entrepreneur into the dream of owning your own home.

Global Lending Trends and Your Mortgage

To really get why bank statement loans are so important, you need to look at the bigger picture. These aren't just some quirky, niche product; they're a direct answer to massive shifts in the global economy. The reality is, the demand for more flexible ways to get a mortgage isn't just a U.S. thing—it's happening everywhere as the way people work and earn money continues to change.

Think of it like this: economic trends in other major countries often give us a sneak peek of what’s heading our way. When global financial institutions talk about lending rules or housing market confidence, they're painting a picture of what kind of financing people worldwide are hungry for. This global perspective shows that bank statement loans aren't just a fad; they’re a stable and essential part of the modern lending landscape.

A Worldwide Demand for Flexibility

All around the world, the classic 9-to-5 job is no longer the only way to build a successful career. This simple fact has pushed lenders everywhere to get creative and rethink how they decide who is a good candidate for a loan. The U.S. market has been ahead of the curve in creating products like bank statement loans, but the fundamental need for them is truly universal.

You can see this playing out in recent numbers from Europe. A survey of banks in the Euro area for the second quarter of 2025 showed that demand for home loans jumped by a net 37%. That's a huge increase, and it was directly linked to a better outlook on the housing market and growing consumer confidence. This tells us there's a powerful, ongoing need for mortgage options that work for all kinds of borrowers, especially those with non-traditional income. You can dig into the data yourself in the European Central Bank's survey report.

This data from overseas makes one thing crystal clear: as economies change, lending has to change with them. Strong demand for housing isn't just coming from people with a W-2.

The global rise in entrepreneurship and freelance work is creating a powerful, worldwide demand for loans that look beyond traditional paperwork and focus on provable, real-world cash flow.

Looking at it from this high-level view, it's obvious that bank statement loans aren't a temporary workaround. They represent a necessary evolution in how people buy homes. They are a resilient and relevant tool in a modern, global economy where the very definition of a "qualified borrower" is getting broader every day.

To get the full picture of how global trends might affect your home-buying journey, it’s helpful to continue understanding various mortgage options, including reverse mortgages. By looking at the entire financial landscape, you can move forward with confidence, knowing that flexible solutions like these are here to stay.

Common Questions About Bank Statement Loans

Even with a solid understanding of how these loans work, you probably still have a few specific questions. It's only natural. After all, this isn't your everyday mortgage path.

Let's clear up some of the most common questions I hear from entrepreneurs and self-employed professionals. Think of this as the final check-in before you move forward, making sure you’re totally comfortable with the details.

Can I Get a Bank Statement Loan with a Low Credit Score?

You can, but it's not a free pass. While these loans are definitely more forgiving than a conventional mortgage, a lower credit score—say, in the mid-600s—means the lender will need to see strength elsewhere in your file.

What does that look like? Usually, it means putting more skin in the game with a substantial down payment, often 20-30% or more. Lenders also love to see healthy cash reserves left over after closing. Your cash flow is the star of the show here, but a lower score will mean a higher interest rate. There’s no getting around that.

Are Interest Rates for Bank Statement Loans Much Higher?

They are higher, yes. You should plan for an interest rate that's anywhere from 0.5% to 2.0% above what you'd see on a standard, W-2 based loan. The exact rate depends on your credit, how much you're putting down, and the lender's specific programs.

This isn't a penalty; it's simply the lender's way of balancing the risk of not using traditional income documents like tax returns. For most business owners I work with, paying a slightly higher rate is a small price for the opportunity to buy a home based on their actual, real-world income.

You're essentially paying a premium for flexibility. It’s a trade-off that allows your business's true cash flow, not just what's on your tax returns, to get you the keys to your home.

Is a P&L Statement from an Accountant Required?

It's not always mandatory, but I strongly advise it. Submitting a profit and loss (P&L) statement prepared and signed by your CPA adds a huge amount of credibility to your application. It gives the underwriter a professionally vetted snapshot of your business's health.

Frankly, a CPA-prepared P&L just looks better. It shows you're serious and organized, and it can sometimes even help you secure better terms. Think of it as a small investment to make your application as strong as possible.

Can I Use Business Bank Statements for a Personal Mortgage?

Absolutely! That’s precisely what these loans are designed for. Lenders who specialize in this niche are skilled at reviewing 12 or 24 months of your business deposits to determine a stable, qualifying income.

They'll apply an "expense factor" to your gross deposits—often around 50%, though it varies—to arrive at an estimated net income figure they can use for your personal mortgage. This calculation proves you can handle the new house payment, creating a direct bridge from your business's success to your dream of homeownership.

Ready to turn your business's cash flow into your new home? The team at Tiger Loans Inc specializes in finding the right financing for entrepreneurs. Explore your options and start your journey today.

Alex Chen

Alex Chen

Get in touch with a loan officer

Our dedicated loan officers are here to guide you through every step of the home buying process, ensuring you find the perfect mortgage solution tailored to your needs.

Options

Exercising Options

Selling

Quarterly estimates

Loans

New home

Stay always updated on insightful articles and guides.

Every Monday, you'll get an article or a guide that will help you be more present, focused and productive in your work and personal life.

.png)

.png)

.png)

.avif)

.avif)

.avif)

.png)

.png)

.png)

.avif)

.png)

.png)

.avif)

.png)

.avif)

.png)

.avif)

.avif)