Can You Have Two FHA Loans? Find Out the Rules & Exceptions

November 19, 2025

Wondering can you have two FHA loans? Learn the rules, exceptions for relocation or expanding your family, and how to qualify today.

It might come as a surprise, but yes, you can actually have two FHA loans at the same time. It’s not an everyday occurrence, but it’s definitely possible under the right circumstances.

The Federal Housing Administration generally prefers that borrowers only have one FHA-insured mortgage at a time. However, life happens. Big changes like a job relocation or a family that’s outgrowing its home can open the door for a second FHA loan.

The Surprising Truth About Having Two FHA Loans

There's a persistent myth that FHA loans are only for first-time homebuyers, but that’s simply not true. The FHA’s main mission is to encourage homeownership where people actually live, not to lock you into a single home for the rest of your life.

Think of it like this: the FHA’s general policy is like having a "one-ticket-per-person" rule for a sold-out concert. Normally, you just get one. But for a few special cases, they’re willing to hand out a second ticket.

This guide will walk you through exactly when and how you can qualify for that second FHA loan. It helps to understand just how big the FHA's role is in the housing market. They’re a powerhouse, insuring over 7.81 million mortgages across the country. And while it’s true that a whopping 82.6% of their purchase loans in Fiscal Year 2024 went to first-time buyers, they have the flexibility to help repeat borrowers who find themselves in specific situations. You can dive deeper into the FHA's recent lending data to see its market impact firsthand.

A Quick Refresher on FHA Loans

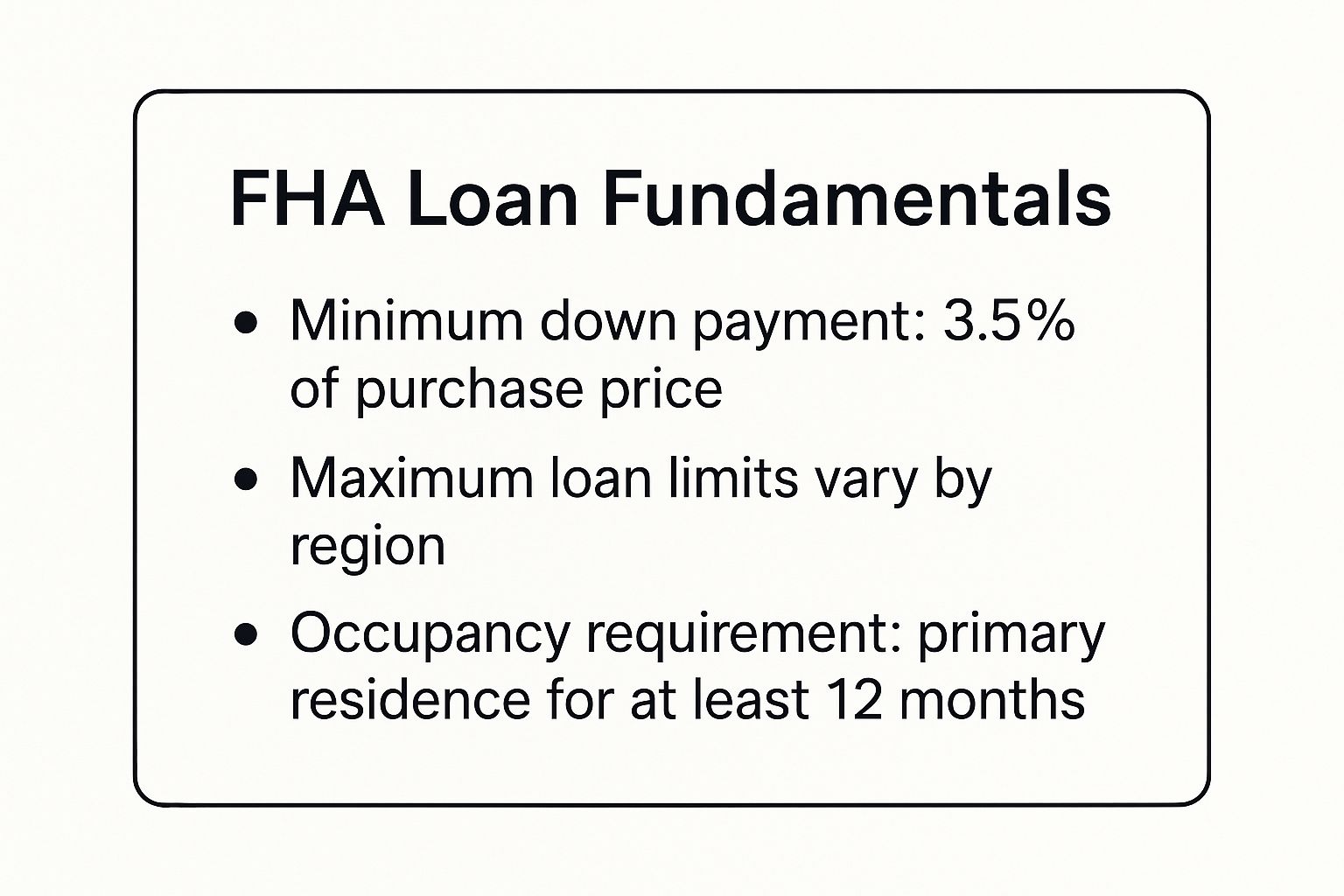

Before we get into the exceptions, let's quickly touch on what makes an FHA loan tick. This infographic lays out the core requirements that every borrower has to meet, whether it's their first loan or they're aiming for a second.

As you can see, the FHA program is built around low down payments, specific loan limits for each area, and a strict rule that the home must be your primary residence. It’s this "primary residence" rule that forms the backbone of the "one loan" policy.

The exceptions we're about to cover are designed for times when life changes make it impossible for your current FHA-financed house to continue being your primary home. So, let’s explore the exact scenarios that could get you approved.

Why FHA Loans Focus on Primary Residences

Before we even get into the nitty-gritty of getting a second FHA loan, you have to understand the program’s entire reason for being. The Federal Housing Administration isn't here to help people build real estate empires. Its core mission has always been about helping families plant roots in a community by buying a home they will actually live in.

This focus on a primary residence is the foundation for the FHA's general "one loan at a time" rule. The program was built from the ground up to make homeownership a reality for everyday people, especially those who might not have a huge down payment or a perfect credit score. It’s all about strengthening neighborhoods, one homeowner at a time. This is why the question "can you have two FHA loans?" usually gets a quick "no" before the conversation can even get started.

You can think of an FHA loan like a specific kind of grant—say, a scholarship for a specific university. It’s given to a student so they can attend that school and live on campus. The money is for that one purpose, not so they can start a side hustle or play the stock market. The FHA loan is designed for you to buy and live in a home.

The Real Reason for the Occupancy Rule

The FHA’s requirement that you live in the home isn’t just some random rule they came up with. It's the key to making the whole program work as intended. By making sure borrowers are living in the homes they finance, the FHA lowers its risk and achieves its main goals.

- Building Stronger Communities: When you live in your home, you care about it. You maintain the property, get to know your neighbors, and contribute to the local area. This creates stable, healthy neighborhoods.

- Lowering the Risk: It's a simple fact: people are far less likely to walk away from a mortgage on the home they live in compared to a rental property. This keeps default rates down and protects the FHA's insurance fund, which is what makes these loans possible in the first place.

This core principle is exactly why the exceptions to the one-loan rule exist. They aren't loopholes to be exploited; they are common-sense solutions for real-life situations where a family genuinely needs to move and establish a new primary residence.

The FHA’s occupancy requirement is its most powerful tool for ensuring the program serves its intended purpose: building homeowner equity and stabilizing communities, rather than fueling speculative investment.

Laying the Groundwork for Your Second Loan

Getting a solid grasp on this philosophy is the first and most important step in building your case for a second FHA loan. When you go to a lender, you’re not just filling out forms. You need to show them that your situation fits squarely within the FHA’s mission.

You’re not just asking for another loan; you’re proving that your life circumstances have changed in a way that makes it impossible to keep living in your current home. When you understand the why behind the rules, you can explain the how of your situation much more effectively.

Learning more about the specifics of FHA loans and their requirements will give you a much clearer picture of what lenders are looking for. That knowledge is a huge advantage when you need to make the case that you qualify for one of these rare exceptions.

How You Can Qualify For A Second FHA Loan

The FHA typically has a strict "one loan per borrower" policy, but they're not unreasonable. They know that life happens. Major life events can turn your dream home into one that no longer fits your needs, and for those specific situations, the FHA has carved out a few key exceptions.

Think of these exceptions less as loopholes and more as official detours on your homeownership path. They’re designed for borrowers who have a legitimate, well-documented reason for needing a new primary residence while still holding their first FHA-backed property.

The two most common reasons people qualify are relocating for a new job and needing more space for a growing family. Let's break down exactly what it takes to get approved under these scenarios.

The Job Relocation Exception

This is probably the most clear-cut path to a second FHA loan. If your employer is moving you to a new location that’s too far to commute, the FHA will often approve a new loan. The entire case hinges on proving the move is a career necessity, not just a personal choice.

So, what’s considered “too far”? While the FHA doesn't have a hard-and-fast rule, the widely accepted benchmark among lenders is that your new home must be at least 100 miles away from your old one.

The Bottom Line: Your lender needs to see undeniable proof that the job relocation is out of your hands and that the distance makes it impossible to continue living in your current home. Your paperwork is everything here.

To build a rock-solid case, you’ll need to hand over some concrete evidence to your lender, including:

- An official transfer letter from your employer on company letterhead.

- A new employment contract that clearly states your new job's location.

- Recent pay stubs that list the new work address.

The Growing Family Exception

Life changes, and families expand. That two-bedroom starter home that felt so spacious for a couple can quickly feel cramped when a new child arrives. The FHA gets it, which is why this exception exists for homeowners who have genuinely outgrown their current living space.

To qualify, you need to show a documented increase in your number of legal dependents—think a birth, an adoption, or another event that makes your home's size inadequate by local occupancy standards.

But there’s another critical piece to this puzzle: equity. Your loan-to-value (LTV) ratio on your existing FHA loan must be 75% or less. In simple terms, this means you need to own at least 25% of your home, either by paying down your mortgage or through an increase in your home’s market value.

It's also worth understanding how this differs from other financing tools. For a deeper dive, check out our guide on second mortgage vs. home equity loan options to see if those might be a better fit for your situation.

FHA Second Loan Documentation Checklist

When you're applying for a second FHA loan, your lender will need a specific set of documents to verify your eligibility under one of the approved exceptions. Having these papers in order from the start can make the process much smoother.

This checklist covers the essentials, but keep in mind that your lender might ask for additional information depending on your specific circumstances.

Navigating Today's Market

Getting approved for an exception is a huge step, but you still have to navigate the realities of the housing market. In a competitive environment, sellers sometimes view offers backed by conventional loans as safer or faster to close. In fact, 2023 mortgage lending data from the Consumer Finance Protection Bureau highlights these market dynamics.

This doesn't mean your FHA-backed offer won't be accepted, but it does mean your application needs to be as strong as possible to stand out. Working with an experienced lender who understands the ins and outs of FHA guidelines is absolutely critical to successfully landing that second home.

When Life Throws You a Curveball

While moving for a job or making room for a growing family are the most common reasons people need a second FHA loan, life doesn't always stick to the script. The FHA gets this. They've built in flexibility for other complex situations that create a genuine need for a new primary home.

These aren't everyday cases, and they demand solid paperwork and a clear story. But knowing these exceptions exist might just open a door you thought was permanently closed.

Leaving a Jointly Owned Home

Divorce is a tough, messy process, and it almost always forces a change in who lives where. If you're on an FHA loan with a spouse but have to move out as part of a legal separation, you can often qualify for a new FHA loan on your own.

The lynchpin here is the legal side of things. Your lender will need to see official court documents proving you're vacating the property and that your ex-spouse is taking over the responsibility.

The Bottom Line: A divorce decree that hands over the house—and the mortgage payment—to your former spouse is your golden ticket. It's the proof that you're no longer legally tied to living there.

This is just a practical rule for a difficult time. It ensures you can get back on your feet and establish a new household without being held back by a mortgage that’s no longer part of your life.

The Co-Signer Situation

But what if you never even lived in the first house? This happens all the time when a parent or family member acts as a non-occupying co-borrower—basically, a co-signer—to help a loved one get their first FHA loan.

Good news. Since you never occupied that property as your primary residence, the FHA doesn’t count it against you. You're still eligible to get an FHA loan for a home you actually plan to live in.

To get the green light, you’ll just need to show your lender:

- Proof You Never Lived There: Utility bills or other documents showing you maintained a separate residence.

- You Can Afford It: The lender will still include the co-signed mortgage in your debt-to-income ratio, so you'll have to prove you can handle both payments.

- Clear Intent: Your application must make it obvious that this new home will be your primary residence.

Think of it this way: the FHA sees you as having helped someone else on their homeownership journey, not as having completed your own. It's a smart distinction that allows families to support each other without anyone losing out on their own chance to buy a home.

Your Step-By-Step Application Guide

So, you’ve read the rules and think your situation fits one of the FHA's rare exceptions. That’s a huge first step. But knowing the rules and actually getting approved are two different things. Now it’s time to build a rock-solid application.

Let's walk through exactly what you need to do. Think of this as your roadmap to getting that second FHA loan across the finish line.

Step 1: Prove Your Exception Without a Doubt

Before you even dream of talking to a lender, you need to be 100% certain you qualify. Don't just think you do—prove it to yourself first.

Relocating for Work? Is the new job at least 100 miles away? Do you have an official, signed offer letter or transfer notice from your employer that clearly states the move is a condition of employment?

Family Getting Bigger? Can you document the increase in your family size (like birth certificates)? And here’s the big one: is your current home's loan-to-value (LTV) ratio at 75% or lower? In simple terms, you need to have at least 25% equity built up.

If you can’t say a firm "yes" to these, your application will be a non-starter. Getting this right from the beginning will save you a world of time and frustration.

Step 2: Gather Your Paper Trail

An underwriter won't take your word for it. Your story is only as convincing as the documents you use to back it up. They need cold, hard proof.

An underwriter's job is to see the facts, not just hear the story. A complete, organized file makes their job easy, which makes saying "yes" to your loan much, much easier.

Start a folder—digital or physical—and get everything in one place. We're talking about that employer relocation letter, the new birth certificates, your current mortgage statements, and maybe even a recent appraisal to prove your equity. Walking into a lender's office with all this ready shows you're serious and prepared.

Step 3: Find a Lender Who Gets It

Listen, not all FHA-approved lenders are the same. Many can handle a standard FHA loan with their eyes closed, but the two-loan exception is a different beast. You need to find someone who's been down this road before.

When you're talking to loan officers, ask them this point-blank: "How many second FHA loans have you closed for clients under the relocation or growing family exceptions?" Their answer will tell you everything. An experienced lender will know exactly what underwriters are looking for. They can help you package your story in the most compelling way.

And if your plans involve building from the ground up, you'll want to ask about specialized products like an FHA construction loan as well.

Step 4: Brace for Underwriting

This is the final boss. An underwriter is going to dig into every corner of your financial life, looking at both properties. They’ll want to know why you need to keep the first home and, more importantly, if you can truly afford two mortgage payments.

They will calculate your debt-to-income ratio with both housing payments included, so your finances need to be squeaky clean. Be ready for tough questions. The more prepared you are with clear answers and solid documentation, the smoother this final, critical step will be.

Is a Second FHA Loan the Right Move?

Getting the green light for a second FHA loan feels like a huge win, but hitting that milestone isn't the finish line. Just because you can get another FHA-backed mortgage doesn't automatically mean you should. This is a major decision that will shape your financial future for years to come, so it’s critical to step back and think strategically.

After all, two mortgages mean double the financial load. You’re now on the hook for two sets of property taxes, two insurance bills, and the upkeep on two different homes. That’s a heavy lift, and it demands a rock-solid income and a well-managed budget to pull it off without sleepless nights.

Weighing Your Financial Game Plan

Before jumping in with both feet, let's look at the other paths you could take. Each one has its own set of pros and cons, and one might fit your long-term goals way better than the others. The goal here isn't just to solve an immediate housing problem—it's to make the smartest move for building wealth and stability.

A second FHA loan can be a fantastic solution for navigating major life changes, but true financial success comes from choosing the right tool for the job, not just the one that’s easiest to grab.

Let's break down the most common strategies you should consider.

Your Three Main Options

Keeping Both FHA Loans: This makes sense if you’re planning to move back into the first house eventually or need to keep it for a family member. The big downside? It ties up a massive amount of your money and borrowing capacity, leaving you with less flexibility.

Selling Your First Home: This is usually the cleanest path forward. Selling frees up all the equity you've built, which you can then roll into a bigger down payment on your new place. A larger down payment can mean a smaller monthly payment and a much simpler financial life without the headaches of being a landlord.

Refinancing into a Conventional Loan: Have your credit score and income improved since you bought your first home? If so, refinancing it into a conventional loan could be a brilliant move. This frees up your FHA eligibility entirely for the new purchase and might even let you drop the pesky mortgage insurance, saving you a chunk of cash every month.

At the end of the day, there's no single "right" answer. The best choice is the one that aligns with your personal situation, your financial stability, and where you see yourself in the next five to ten years.

Digging into the Details: Your FHA Questions Answered

Even when you've got a good handle on the basics, the idea of getting a second FHA loan can bring up some very specific questions. Let's walk through a few of the most common ones that pop up, so you can move forward with confidence.

Can I Use a Second FHA Loan to Buy an Investment Property?

That’s going to be a hard no. The FHA loan program is designed from the ground up to help people buy homes they actually live in.

It’s all about owner-occupancy. This means the home you buy with an FHA loan has to be your primary residence. This rule is a cornerstone of the FHA's mission, so there's no wiggle room here.

How Far Do I Need to Move for the Relocation Exception?

The FHA doesn’t actually have a specific mileage requirement written into its official guidelines. However, in the real world, lenders have created a solid rule of thumb: 100 miles.

If your new job is at least 100 miles away from your current home, it’s pretty clear that a daily commute is out of the question. This makes it much easier to justify the need for a new primary residence closer to work.

Is There an Equity Requirement for My First Home?

Yes, for some scenarios, the equity in your current home is a make-or-break factor. This is especially true if you're trying to get a second FHA loan because your family has outgrown your current space.

To qualify under the "growing family" exception, you'll need to have at least 25% equity in your first home. This translates to a loan-to-value (LTV) ratio of 75% or less. Lenders see this as a sign of financial responsibility, showing you're in a stable position to handle a second mortgage.

Ready to explore your options and see if you qualify? The experts at Tiger Loans Inc can provide the personalized guidance you need to navigate the complexities of FHA loans and make your next move with confidence. Find out more at Tiger Loans Inc.

Alex Chen

Alex Chen

Get in touch with a loan officer

Our dedicated loan officers are here to guide you through every step of the home buying process, ensuring you find the perfect mortgage solution tailored to your needs.

Options

Exercising Options

Selling

Quarterly estimates

Loans

New home

Stay always updated on insightful articles and guides.

Every Monday, you'll get an article or a guide that will help you be more present, focused and productive in your work and personal life.

.png)

.png)

.png)

.avif)

.avif)

.avif)

.png)

.png)

.png)

.avif)

.png)

.png)

.avif)

.png)

.avif)

.png)

.avif)

.avif)