Conventional Loan vs FHA Which Is Best for You

November 19, 2025

Struggling with the conventional loan vs FHA decision? We compare credit scores, down payments, and mortgage insurance to help you choose the right mortgage.

When you’re weighing a conventional loan against an FHA loan, it really boils down to your specific financial picture. FHA loans are built to open the door for buyers who might have a few credit blemishes or less cash saved up. On the other hand, if you've worked hard to build a strong credit history and have a decent down payment, a conventional loan will almost always reward you with better long-term costs and fewer strings attached.

Your At-a-Glance Guide to Conventional vs FHA Loans

Choosing a mortgage can feel overwhelming, but it gets a lot simpler when you understand what each loan is designed to do. Think of FHA and conventional loans as the two main highways to homeownership—they'll both get you there, but they're built for different kinds of drivers.

FHA loans are insured by the government, which makes lenders more comfortable loaning money to someone with a less-than-perfect profile. Conventional loans are the private market's answer, catering to borrowers who meet stricter financial standards. The trick is to honestly assess your own situation—your credit, your savings, your debt—and pick the path that makes the most sense for you right now.

Core Differences You Need to Know

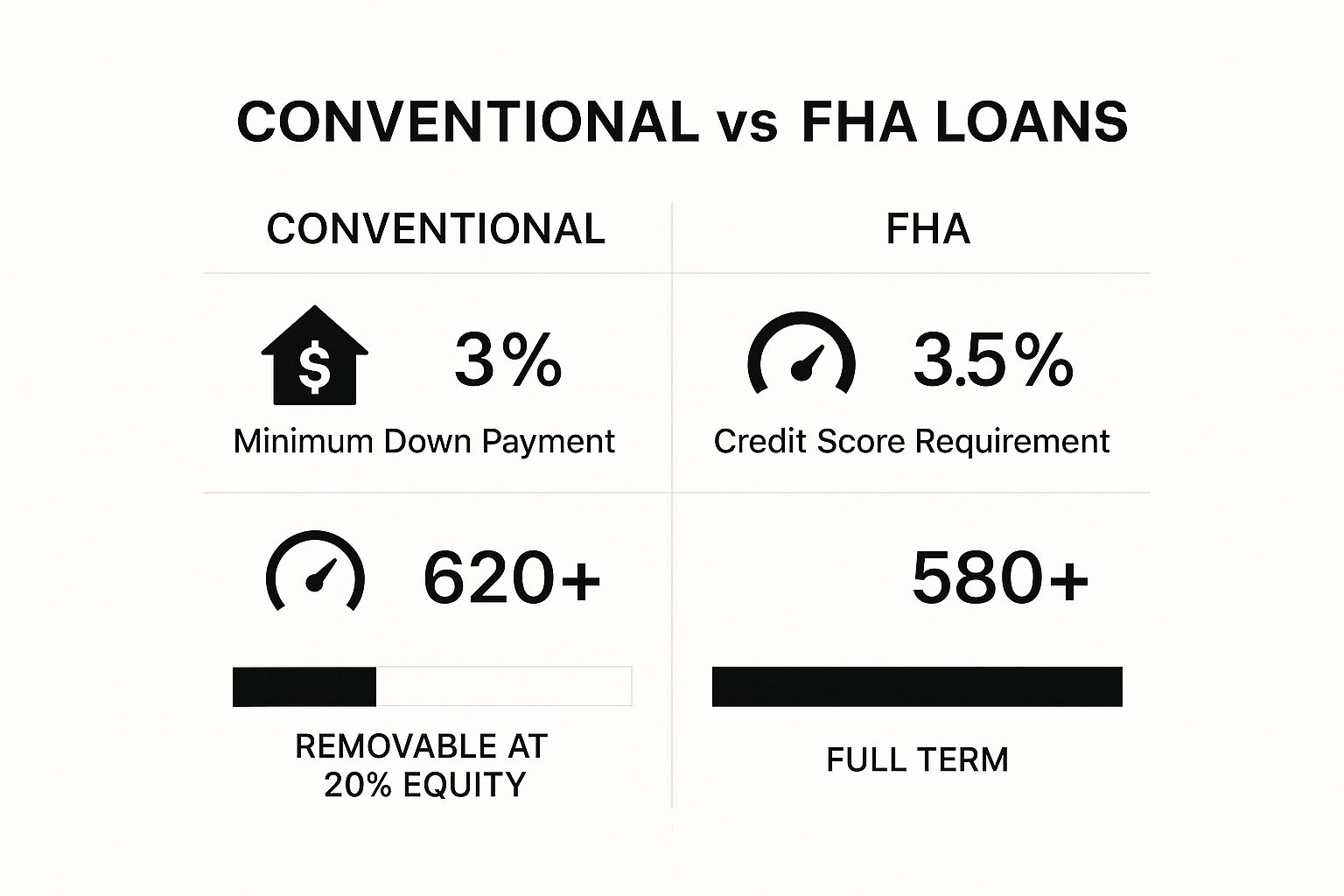

In 2025, the fundamental things that set these loans apart are still credit scores, down payment minimums, and mortgage insurance. For a conventional loan, most lenders are looking for a credit score of at least 620. FHA loans, however, are much more forgiving; you can often get approved with a score as low as 580 while still only putting down 3.5%.

If your credit score is in the 500 to 579 range, an FHA loan might still be on the table, but you'll need to bring a 10% down payment. It’s a common misconception that conventional loans always require 20% down. In reality, some programs let you get in the door with as little as 3% down.

This quick visual breaks down the most important numbers you need to know.

As you can see, the FHA loan is your foot in the door. But the conventional loan is where you start to see serious long-term savings, especially when it comes to ditching mortgage insurance.

Key Takeaway: Don't just focus on qualifying for the loan today. Think about the total cost over the next 10, 20, or 30 years. Getting rid of Private Mortgage Insurance (PMI) on a conventional loan can literally save you thousands of dollars.

To help you see the differences side-by-side, I've put together a simple comparison table. If you've got solid credit and a bit of cash in the bank, exploring your conventional loan options is a fantastic place to start.

At-a-Glance Comparison: FHA vs. Conventional Loans

This table gives you a high-level snapshot of the core differences, helping you quickly see where you might fit.

Ultimately, the best loan is the one that aligns with both your current financial reality and your future goals.

Understanding the Core Purpose of Each Loan

To really get a handle on the FHA vs. conventional loan debate, you have to look beyond the surface-level numbers. It’s about understanding why each loan exists in the first place. These two paths to homeownership were designed with completely different homebuyers in mind, and their rules and costs directly reflect those distinct missions.

Think of an FHA loan as a mission-driven tool. At its heart, it’s a government-insured program designed to open the door to homeownership for more people, especially those who might struggle to get approved for a traditional mortgage. This core goal shapes every aspect of the loan.

On the other hand, a conventional loan is a pure product of the private market. Banks, credit unions, and mortgage companies fund these loans without any government guarantee. They follow the rules set by Fannie Mae and Freddie Mac, the major players that keep the mortgage market flowing. Because they’re privately funded, these loans naturally favor borrowers who look like a safer bet on paper.

The Mission-Driven FHA Loan

The FHA loan has a fascinating backstory rooted in the Great Depression. The government introduced it back in 1934 to get the housing market moving again. By insuring loans, the FHA reduced the risk for lenders, which in turn made them willing to accept buyers with smaller down payments.

That historical context is still the driving force today. The Federal Housing Administration isn't handing you the money directly; it's promising your lender that they'll be covered if you default. This government backing is a game-changer, giving lenders the confidence to work with borrowers who have:

- Less-than-perfect credit scores

- Minimal savings for a down payment

- A higher debt-to-income ratio

The FHA essentially acts as a lender's safety net. This is precisely why it's such a powerful option for many first-time buyers or anyone rebuilding their finances.

Key Insight: The best way to think about an FHA loan is as an accessibility tool. Its entire purpose is to give more qualified people a shot at owning a home, even if their financial picture isn't flawless.

Given its mission of accessibility, it’s worth seeing if this option fits your situation. Our team can walk you through the specifics, and you can get an in-depth look in our guide to FHA loans in your area.

The Market-Driven Conventional Loan

Conventional loans play by a different set of rules, guided by a simple principle: risk-based pricing. There’s no government insurance here to protect the lender if things go south. The decision to approve your loan comes down entirely to your financial track record.

This is exactly why the standards are tougher. Lenders need solid proof that you’re a low-risk borrower. A strong credit score, manageable debt, and a healthy down payment all send a clear signal that you’re financially responsible and likely to pay back the loan.

The good news? This model heavily rewards borrowers with strong financial habits. Lenders are competing for your business, so they offer their best deals to those who qualify:

- Lower interest rates

- More favorable loan terms

- The ability to completely avoid mortgage insurance with a 20% down payment

Ultimately, the goal of a conventional loan is to offer a sustainable, market-driven financing option. It’s designed to empower financially stable borrowers, giving them a path to secure a home with the best possible long-term costs.

Comparing Your Eligibility for Each Mortgage

So, how do you actually qualify? Getting a mortgage isn’t magic; it’s about the numbers on your application. To make a smart choice between a conventional and an FHA loan, you need to get real about your financial situation and see how it stacks up against each program's rules.

This is where the rubber meets the road. We're moving past the big-picture ideas and digging into the three core pillars of mortgage eligibility: your credit score, your down payment, and your debt-to-income (DTI) ratio. Each loan program has its own take on these numbers, creating different paths to getting the keys to your new home.

The Decisive Role of Your Credit Score

Your credit score is the first hurdle. For lenders, it’s a quick snapshot of how you’ve handled debt in the past, and it has a massive impact on which loans you can even apply for.

With a conventional loan, most lenders draw a line in the sand at a 620 credit score. If your score is higher, you're not just more likely to get approved—you’ll probably be offered better interest rates and lower private mortgage insurance (PMI) costs. It's their way of rewarding you for a solid financial track record.

An FHA loan, on the other hand, is built for flexibility. You can often get your foot in the door with a credit score as low as 580. In some situations, lenders might even consider scores down to 500, though with some extra conditions. This makes it a lifeline for people who are still working on building or repairing their credit.

A Real-World Scenario: Imagine you have a 630 credit score. You might qualify for both loans. The FHA loan is a sure bet, but the conventional loan could let you ditch your mortgage insurance in a few years. This is why you have to look at the long-term cost, not just the initial approval.

Analyzing Down Payment Requirements

After credit, the next big question is how much cash you can bring to closing. The down payment is a major sticking point for many buyers, but the rules are more straightforward than you might think.

- FHA Loan Down Payment: The most common requirement is 3.5% of the home's purchase price. This is available to anyone with a credit score of 580 or higher. If your score is between 500 and 579, you'll need to put down 10%.

- Conventional Loan Down Payment: There's a persistent myth that you need 20% down for a conventional loan. The truth is, many borrowers can qualify with as little as 3% down, thanks to programs like Fannie Mae’s HomeReady or Freddie Mac’s Home Possible.

The best move here really depends on your savings account. A 3% conventional down payment is technically less cash upfront than the 3.5% FHA minimum. But if your credit score is hovering below 620, the FHA loan is your most realistic shot at homeownership without spending years saving up.

Understanding Debt-to-Income Ratio Flexibility

The final piece of the puzzle is your debt-to-income (DTI) ratio—the percentage of your gross monthly income that goes toward paying your monthly debts. This number shows lenders how much financial breathing room you have.

Conventional loans are usually stricter here. Lenders typically want to see a DTI ratio of 43% or less. For borrowers with otherwise stellar applications (like a high credit score and significant savings), some automated systems might stretch this up to 50%.

FHA guidelines, however, are much more forgiving. While the official target DTI is also 43%, lenders frequently approve applicants with ratios up to 50% or even 57%. They’ll just want to see other strengths, like good credit or cash reserves, to balance the risk. This flexibility is at the very heart of the FHA program's goal to make homeownership more accessible.

While this guide focuses on buying a home to live in, it never hurts to get a broader perspective on the lending world. For anyone curious, you can find great tips on getting approved for various property loans. Understanding what lenders look for in general can make you a much more confident borrower.

The True Cost of Your Mortgage Insurance

When you’re weighing a conventional loan against an FHA loan, one factor stands out above all others in shaping your long-term costs: mortgage insurance. It might seem like a small detail, but the way each loan handles this requirement can mean a difference of tens of thousands of dollars.

Both loans require mortgage insurance if your down payment is less than 20%, but that's where the similarities end. FHA loans have their own system, called Mortgage Insurance Premium (MIP), which is the price you pay for its flexible approval standards. On the other hand, conventional loans use Private Mortgage Insurance (PMI), a far more borrower-friendly option. Getting this one distinction right is your key to a much healthier financial future.

The Unavoidable Costs of FHA MIP

Let's be direct: FHA mortgage insurance is expensive and relentless by design. It’s the very thing that gives lenders the confidence to back loans for borrowers who might not otherwise qualify. This safety net, however, comes with a hefty price tag, broken into two non-negotiable parts.

First, you’re hit with an Upfront Mortgage Insurance Premium (UFMIP). This is a one-time fee of 1.75% of your loan amount, due at closing. On a $300,000 loan, that’s an immediate $5,250 cost. Most people finance this by rolling it into the loan, but that just means you’re paying interest on it for years to come.

Then comes the real long-term pain: the annual MIP. This premium is bundled into your monthly mortgage payment. For the vast majority of FHA borrowers putting down the minimum 3.5%, this insurance payment is for life. It doesn't matter how much your home value appreciates or how much equity you build—it stays with you for the entire 30-year term.

Crucial Distinction: This is the point that trips up so many homebuyers. With an FHA loan, you can't just call your lender and cancel MIP once you hit 20% equity. The only ways out are to sell your house or refinance into a different loan program.

The Flexibility and Freedom of Conventional PMI

This is where a conventional loan pulls way ahead for well-prepared borrowers. Private Mortgage Insurance (PMI) is also required for down payments under 20%, but it was created with an end date in mind. It exists for one reason only: to protect the lender until you have a solid stake in your property.

Once your loan-to-value (LTV) ratio drops to 80% (meaning you own 20% of your home’s value), you can officially ask your lender to cancel PMI. Even better, federal law requires lenders to automatically terminate it when your LTV hits 78% based on your original payment schedule. This built-in escape hatch is the single biggest financial advantage a conventional loan has over an FHA loan.

A Real-World Cost Comparison

Let's ground this in reality. Say you're buying a $325,000 home with a 5% down payment, giving you a loan of $308,750.

FHA Loan Scenario: Right off the bat, you'd have a $5,403 UFMIP (1.75%), which you’d probably add to your loan. Then, your annual MIP (at a common rate of 0.55%) would add about $141 to your payment every single month, for 30 years.

Conventional Loan Scenario: Assuming you have a good credit score, your PMI rate might be lower, perhaps around 0.45%. That translates to a monthly cost of about $116. The critical difference? You’d likely only pay this for about 8-9 years before reaching 20% equity and eliminating it completely.

The long-term cost difference here is staggering.

Long-Term Cost Analysis: MIP vs. PMI

This table illustrates the total cost of mortgage insurance over the life of a hypothetical $300,000 loan for both FHA and conventional options, highlighting the potential savings with cancellable PMI.

The numbers don't lie. In this fairly typical situation, choosing the conventional loan saves you over $43,000 in mortgage insurance costs alone.

Don't just take my word for it. You can see how these costs impact your own potential budget by plugging your numbers into a good mortgage calculator to compare payment scenarios side-by-side. Sometimes, seeing the hard numbers makes the financial benefit of escaping lifetime MIP impossible to ignore.

It's not just about your personal financial picture; the house itself has a huge say in the conventional vs. FHA loan decision. The right mortgage needs to fit both the home's price tag and its physical condition. These two areas—loan limits and property standards—can often make the choice for you before you even get started.

How Much House Can You Actually Buy?

One of the first things you'll run into is how much you can actually borrow. With a conventional loan, this is dictated by the conforming loan limits. These are set every year by the Federal Housing Finance Agency (FHFA) and give you a pretty consistent target for most of the country, with some bumps for high-cost areas.

FHA loans play by a different set of rules. The Federal Housing Administration sets its own loan limits on a county-by-county basis, and these are often quite a bit lower than conventional limits. That means a home you could comfortably finance with a conventional loan might be completely out of reach for an FHA loan, depending on where you live.

Imagine you're looking for a home in a nice suburban neighborhood. The conventional loan limit might be $766,550, which opens up a ton of possibilities. But in that same county, the FHA limit could be capped at just $550,000. If you find the perfect place listed at $600,000, the FHA loan is simply not an option. It's a non-starter.

Expert Tip: Before you even start scrolling through listings, do a quick search for your county's FHA and conforming loan limits. Knowing these numbers upfront will save you from the major letdown of falling for a home you can't finance with your chosen loan.

This becomes especially critical in hot markets where prices are constantly testing the upper limits of what's allowed.

The Make-or-Break Factor: Property Condition

The differences go way beyond the price. They extend right down to the home's foundation and roof, and this is where the FHA’s core mission of promoting safe housing really becomes clear.

An FHA appraisal is much more than a simple valuation. Think of it as a health and safety inspection. The appraiser has a strict checklist and is on the lookout for specific red flags that could put a homeowner at risk. This includes things like:

- Chipping or peeling paint in any home built before 1978 (a major lead-based paint concern).

- Any sign of termites or other wood-destroying pests.

- A roof that’s in bad shape or has less than two years of life left in it.

- Obvious safety hazards, like missing handrails on a staircase.

- Major systems—like electrical or plumbing—that are broken or dangerously outdated.

If the appraiser finds any of these problems, they have to be fixed before the loan can be approved. This strict "move-in ready" requirement is there to protect buyers from sinking their life savings into a property that needs immediate, costly repairs.

On the other hand, conventional loans are much more forgiving. The appraiser is still there to make sure the home is worth what you’re borrowing, but their standards are far less rigid. A conventional appraisal isn't going to kill a deal over some cosmetic flaws or minor repairs.

This flexibility makes a conventional loan the go-to option for anyone eyeing a fixer-upper. If you're excited by the idea of buying a place with "good bones" and putting in some sweat equity, a conventional loan is almost certainly what you'll need. A house that needs a lot of work from day one would likely never pass the FHA's strict appraisal standards in the first place.

Which Mortgage Is Right for You in the Real World?

The numbers and rules are one thing, but how do they play out when you're actually trying to buy a house? To really get a feel for the Conventional vs. FHA decision, let's step away from the charts and into the lives of three different homebuyers.

Forget generic pro/con lists. Seeing these loans in action is the best way to figure out which path makes sense for your own financial reality and homeownership dreams.

Scenario 1: The First-Time Buyer with Strong Credit but Low Savings

Let's meet Alex. As a recent grad with a steady job and a solid 710 credit score, Alex is financially responsible. But after tackling student loans, building a massive savings account hasn't been easy. Alex has managed to put away $10,000 and is looking at homes in the $250,000 range.

For Alex, an FHA loan is the clear winner here. The 3.5% minimum down payment works out to just $8,750, leaving a much-needed financial cushion. While a 3% down conventional loan is technically an option ($7,500 down), the FHA loan’s more forgiving debt-to-income rules provide critical flexibility that Alex will likely need.

Ultimately, the FHA loan offers a direct and secure path to homeownership without draining every last dollar. The lifelong mortgage insurance is a known drawback, but it’s a strategic trade-off. For now, it's about getting in the door. The plan is to build equity over the next few years and then refinance into a conventional loan once Alex is on even stronger financial footing.

Scenario 2: The Upgrader with Good Equity and Excellent Credit

Now, let's turn to Maya and Ben. They bought their starter home five years ago and, with a growing family, it's time to move up. They've built up a nice chunk of equity and both have excellent credit scores, averaging around 780. After selling their current place, they'll have enough for a 10% down payment on a $450,000 house.

For them, a conventional loan is really the only path that makes sense. With their stellar credit and a sizable down payment, they can lock in a great interest rate and—this is the key—avoid the permanent mortgage insurance that comes with an FHA loan.

Here’s why it's such a clear-cut decision:

- Down Payment: Their $45,000 (10%) is more than enough to qualify.

- Mortgage Insurance: They'll pay Private Mortgage Insurance (PMI), but only until they hit 20% equity. It has an expiration date.

- Long-Term Savings: Choosing a conventional loan sets them up to cancel their PMI payments in a few years, saving them thousands compared to the FHA's permanent MIP.

Key Takeaway: If you have strong credit and a down payment of 5% or more, a conventional loan will almost always offer a better long-term financial outcome. The ability to cancel mortgage insurance is a powerful wealth-building tool.

Scenario 3: The Investor Eyeing a Fixer-Upper

Finally, there's David, a contractor who wants to buy a property to renovate and live in. He found a diamond in the rough—a house in a great neighborhood that needs a lot of love. We're talking peeling paint, an ancient electrical system, and a roof on its last legs.

In this situation, the house itself makes the decision for him. A conventional loan is the only practical option.

Why? The property David wants would never pass the FHA's strict appraisal standards, which mandate that a home be safe, secure, and essentially move-in ready. An FHA appraiser would immediately flag the peeling paint and faulty systems, killing the deal right there.

A conventional loan, on the other hand, provides the necessary flexibility. While an appraiser still has to confirm the property's value, the standards for repairs are far less rigid. This gives David the green light to buy the house as-is, use his own skills to bring it up to code, and build instant equity in the process.

As you can see, there’s no single “best” mortgage—only the one that’s best for you.

Got Questions? We've Got Answers: FHA vs. Conventional Loans

Okay, so we've covered the fundamentals. But let's be real—the nitty-gritty details are where the real decisions are made. Here are some of the most common questions I hear from homebuyers trying to choose between these two loans.

Can I Refinance My FHA Loan into a Conventional One?

Absolutely. In fact, this is a brilliant financial move that many savvy homeowners make. Think of it as a stepping-stone strategy: you use an FHA loan to get your foot in the door of homeownership, and once you've built some equity and polished your credit, you switch to a conventional loan.

Why bother? The biggest driver is ditching the FHA Mortgage Insurance Premium (MIP), which can stick around for the entire life of your loan. To make the switch and drop mortgage insurance entirely, you'll generally need two things:

- A credit score that qualifies for a conventional loan, usually 620 or better.

- At least 20% equity in your home. Hitting that magic number means you won't have to pay any mortgage insurance at all.

Even if you're not quite at 20% equity, refinancing can still be a game-changer. You’d simply swap the lifelong FHA MIP for Private Mortgage Insurance (PMI) on your new conventional loan, which automatically cancels once you have enough equity. That move alone can save you thousands over time.

Which Loan Is Best for Buying a Multi-Family Property?

This really comes down to your game plan. Both loans can finance a multi-family home (2-4 units), but they're built for different types of investors.

FHA loans are the go-to for "house hacking"—where you live in one unit and let your tenants' rent pay your mortgage. It’s an incredibly accessible path, letting you buy a multi-unit property with a rock-bottom 3.5% down payment.

Conventional loans, on the other hand, give you more freedom. If you want to buy an investment property and rent out all the units without living there yourself, conventional is your only option. FHA loans strictly require you to occupy one of the units.

Key Insight: For first-time investors looking to house-hack, the FHA loan is a powerful tool to get started with minimal cash. For seasoned investors or those buying a pure rental property, a conventional loan is the right fit.

Do Seller Contributions Work Differently?

They sure do, and this can be a huge deal if you’re tight on cash for closing costs.

- With an FHA loan, the seller can contribute up to 6% of the home's purchase price toward your closing costs.

- With a conventional loan, the seller's contribution is capped based on how much you put down. It's typically limited to 3% if your down payment is less than 10%.

If you're negotiating with a motivated seller and need help covering those upfront expenses, the FHA loan gives you a lot more wiggle room.

Figuring out the nuances between conventional and FHA loans is much easier when you have an expert in your corner. At Tiger Loans Inc, our team lives and breathes this stuff. We're here to match you with the perfect mortgage for your financial story. Get your personalized rate quote today and take the first real step toward owning your home with confidence.

Alex Chen

Alex Chen

Get in touch with a loan officer

Our dedicated loan officers are here to guide you through every step of the home buying process, ensuring you find the perfect mortgage solution tailored to your needs.

Options

Exercising Options

Selling

Quarterly estimates

Loans

New home

Stay always updated on insightful articles and guides.

Every Monday, you'll get an article or a guide that will help you be more present, focused and productive in your work and personal life.

.png)

.png)

.png)

.avif)

.avif)

.avif)

.png)

.png)

.png)

.avif)

.png)

.png)

.avif)

.png)

.avif)

.png)

.avif)

.avif)