Difference Between Mortgage Broker and Lender: Key Insights You Need

November 19, 2025

Learn the difference between mortgage broker and lender. Discover pros and cons to choose the best option for your home loan needs.

So, you're ready to buy a home. One of the very first, and most important, decisions you'll make is how you'll get your mortgage. This choice boils down to a fundamental question: should you work with a mortgage broker or go straight to a direct lender?

At its core, the difference is pretty straightforward. A broker is a personal loan shopper who does the legwork for you, connecting with a network of lenders to find the best fit. A lender, on the other hand, is the financial institution—like a bank or credit union—that actually provides the money. This single choice sets the stage for your entire home-buying journey, influencing everything from your loan options to how the process feels.

The First Big Decision in Your Home Purchase

Picking your financing partner is a major fork in the road on your path to homeownership. It's not just a box to check; it’s a strategic financial move that directly affects your interest rate, the fees you'll pay, and your overall stress level.

When you understand what makes these two paths different, you can confidently choose the right professional for your situation. Are you the type of person who wants the widest possible selection of loans laid out in front of you? Or do you find comfort in dealing directly with the institution that's actually funding your dream home?

To make it even clearer, here’s a quick breakdown of how they stack up.

Broker vs Direct Lender A Quick Comparison

Key FactorMortgage BrokerDirect LenderPrimary RoleActs as an intermediary or "loan shopper"Directly funds and underwrites the loanProduct AccessOffers loans from multiple different lendersOnly offers its own in-house loan productsRelationshipWorks for you, the borrower, to find a loanWorks for the bank or lending institutionCompensationPaid a fee, often by the lender (LPC)Earns money through loan origination fees and interest

Getting your loan approved is a huge moment in the [https://www.tigerloans.com/post/home-buying-process-timeline]. Once you've locked in your financing and have the keys in hand, a whole new set of tasks begins. For a great guide on what to tackle first, from utilities to maintenance, this ultimate new homeowner checklist is an invaluable resource.

Choosing the right path—broker or lender—isn't about finding a universally "better" option. It's about finding the best option for your specific financial profile, communication style, and home buying goals.

Understanding Your Relationship With Each Professional

When you're deciding between a mortgage broker and a direct lender, you’re doing more than just picking a service. You’re choosing the kind of relationship you want to have during one of the biggest financial decisions of your life. The real difference comes down to a simple question: who do they work for?

That one detail changes everything—the advice you get, the loans you see, and the support you receive along the way.

The Broker as Your Advocate

Think of a mortgage broker as your personal shopper for a home loan. They are licensed professionals who don't work for any single bank. Instead, they act as the middleman between you and a whole network of wholesale lenders.

Their job is to take your financial situation and shop it around to find the best possible fit. Because they have access to dozens of lenders—from big-name banks to smaller, specialized institutions you've probably never heard of—they see a much wider slice of the market. This puts them in a unique position to find a loan that works for you.

A good broker's loyalty is to you, not a specific bank. Their success is tied directly to getting your loan approved on the best possible terms.

Brokers are experts at packaging your story. They know how to present your income, credit, and assets in a way that appeals to the right lenders. For instance, they'll know exactly which lender is friendly to self-employed individuals or who has the most competitive rates on jumbo loans right now.

The Lender as the Source

A direct lender, on the other hand, is the bank, credit union, or online company that actually provides the money. When you work with a direct lender, you're talking to one of their employees, typically a loan officer.

A loan officer knows their company’s products inside and out. They are experts on their institution's specific guidelines, rates, and approval processes. But here's the catch: their toolkit is limited to only what their employer offers.

They can't tell you if the bank across the street has a better deal. It's a direct-to-consumer relationship where they represent one brand. This is a critical distinction, as it shapes the choices you'll have. For a deeper dive into how these roles shape your home financing journey, Experian.com has a great article.

Ultimately, getting this dynamic right—your advocate versus a direct provider—is the first step. It sets your expectations and helps you understand the motivations behind the advice you're given on your path to owning a home.

Unpacking the True Cost: Broker vs. Lender Fees

When you’re trying to choose between a mortgage broker and a direct lender, the conversation almost always turns to cost. But looking at just the interest rate is a rookie mistake—it doesn't give you the full story. The real financial picture emerges when you dig into how each professional gets paid, because their fee structures are worlds apart.

This isn’t just about finding the "cheaper" option. It's about knowing where your money is going and understanding two completely different compensation models. This is where the difference between a mortgage broker and a lender hits your wallet.

How Your Mortgage Broker Gets Paid

Brokers typically get paid in one of two ways, and understanding the distinction is key. The most common route by far is Lender-Paid Compensation (LPC). With LPC, the lender whose loan you choose pays your broker a commission after the deal is done. This means you don't have a separate, out-of-pocket "broker fee" to worry about at the closing table.

Less frequently, you might encounter Borrower-Paid Compensation. Here, you pay the broker's fee directly, usually as a line item in your closing costs. While it feels more direct, the LPC model is far more prevalent in today's market.

Broker fees generally hover between 1% and 2% of the total loan amount. On a $400,000 mortgage, that's a fee of around $4,000 to $8,000. But with the popular LPC model, this cost is essentially baked into the loan terms by the lender, not paid upfront by you. You can discover more insights about these broker fee structures on HomeLight.com.

How a Direct Lender Makes Its Money

When you go straight to a bank or credit union, you're working with the source of the money. So, you won't see a "broker fee" on your paperwork. Instead, a direct lender's profit is built right into the loan's structure through various standard charges.

Here’s how a lender typically earns its keep:

- Origination Fees: This is the lender’s fee for the work of putting your loan together—the application, processing, and underwriting. It's almost always a percentage of the loan amount.

- Application & Processing Fees: Think of these as covering the administrative legwork and paperwork required to get your loan to the finish line.

- The Interest Rate: This is the long-term profit driver. Lenders make their money over the life of your loan from the interest you pay each month.

The only way to see all these costs laid out is on your official Loan Estimate. This document is your best friend in the process. If you're not sure how to read one, you're not alone. You can get up to speed by decoding loan terms with our essential tips for navigating lender requirements.

A Key Insight: Don't get fixated on just one number. A broker might find you a loan with a slightly higher interest rate because their commission is built into it. Meanwhile, a direct lender might offer a lower rate but hit you with higher upfront origination fees. The only way to make a true apples-to-apples comparison is to look at the Annual Percentage Rate (APR), which rolls fees and interest into a single, powerful number.

How the Loan Process Actually Feels Day to Day

Beyond the numbers on a spreadsheet, what truly sets a mortgage broker apart from a direct lender is the feel of the journey. The day-to-day experience—from that first application to finally getting the keys—is completely different depending on who you partner with. It comes down to communication, how documents are handled, and most importantly, how problems get solved.

When you work with a mortgage broker, it’s like hiring a personal project manager for your home loan. You’ll complete one universal application, and that's your main lift. From there, the broker does the heavy lifting, shopping your profile to various lenders and managing the constant back-and-forth.

Your broker is your single point of contact. This is a game-changer if you’re juggling a job, family, and life. Instead of fielding calls and emails from different people in a bank's underwriting or processing department, you have one dedicated person to call who knows your file inside and out.

Navigating the Lender Process Directly

Choosing a direct lender, on the other hand, gives you a much more straightforward, in-house experience. You'll work directly with the loan officer and their team—the processor, underwriter, and closer—all operating under the same roof. For borrowers with a simple, clean financial history, this can feel incredibly streamlined and efficient.

If you’re already a customer with that bank or credit union, they have a head start with your financial data, which can sometimes speed things up. Communication is direct, but it can also feel a bit segmented. You might talk to a processor about your pay stubs one day and then hear from an underwriter’s assistant about a specific loan condition the next.

The Bottom Line: A broker acts as your buffer and strategist, managing all the moving parts for you. A direct lender offers a direct, and often faster, path to the finish line, but you're locked into their system and their rules.

When Problems Arise During Underwriting

Here's where the rubber really meets the road. This is the moment the difference between a broker and a lender becomes crystal clear. Imagine an underwriter flags a large, unusual deposit in your bank account.

- With a Lender: Your loan officer will ask you for an explanation. If your story and documentation don't neatly fit into their strict, internal guidelines, your loan can stall or even get denied. You're stuck playing by that one lender's rulebook, with no other options.

- With a Broker: Your broker gets the same request. But if that lender proves too rigid, a good broker simply pivots. They can pull your application and quickly resubmit it to another lender in their network—one they know is more lenient with that exact issue. This move can single-handedly save the deal without forcing you to start the entire process over.

As you get closer to the finish line, you’ll interact with several professionals who help finalize the deal. To ensure everything goes smoothly, understanding what a closing agent does is incredibly helpful. The right partner, whether it's a broker or a lender, will make sure you get to that final step without any major hiccups.

When to Choose a Broker vs. a Lender

Deciding who to trust with your mortgage isn't just about chasing the lowest interest rate. It's a personal decision, one that hinges on your unique financial picture, how much hands-on work you want to do, and the level of guidance you need. The real difference between a mortgage broker and a lender pops into sharp focus when you look at specific, real-world situations. In some cases, one is the clear winner.

Think about a self-employed person with income that ebbs and flows from different projects. This is where a mortgage broker really shines. They work with a network of niche lenders, many of whom specialize in non-traditional income. A broker can find a home for that loan, dramatically boosting the odds of approval where a single bank might only see risk.

On the flip side, what about a borrower with a stellar 800+ credit score, a steady W-2 job, and a great relationship with their local credit union? They might find the absolute best deal by going direct. That existing relationship can often unlock loyalty discounts or fee waivers that a broker, as an outsider, simply can't access.

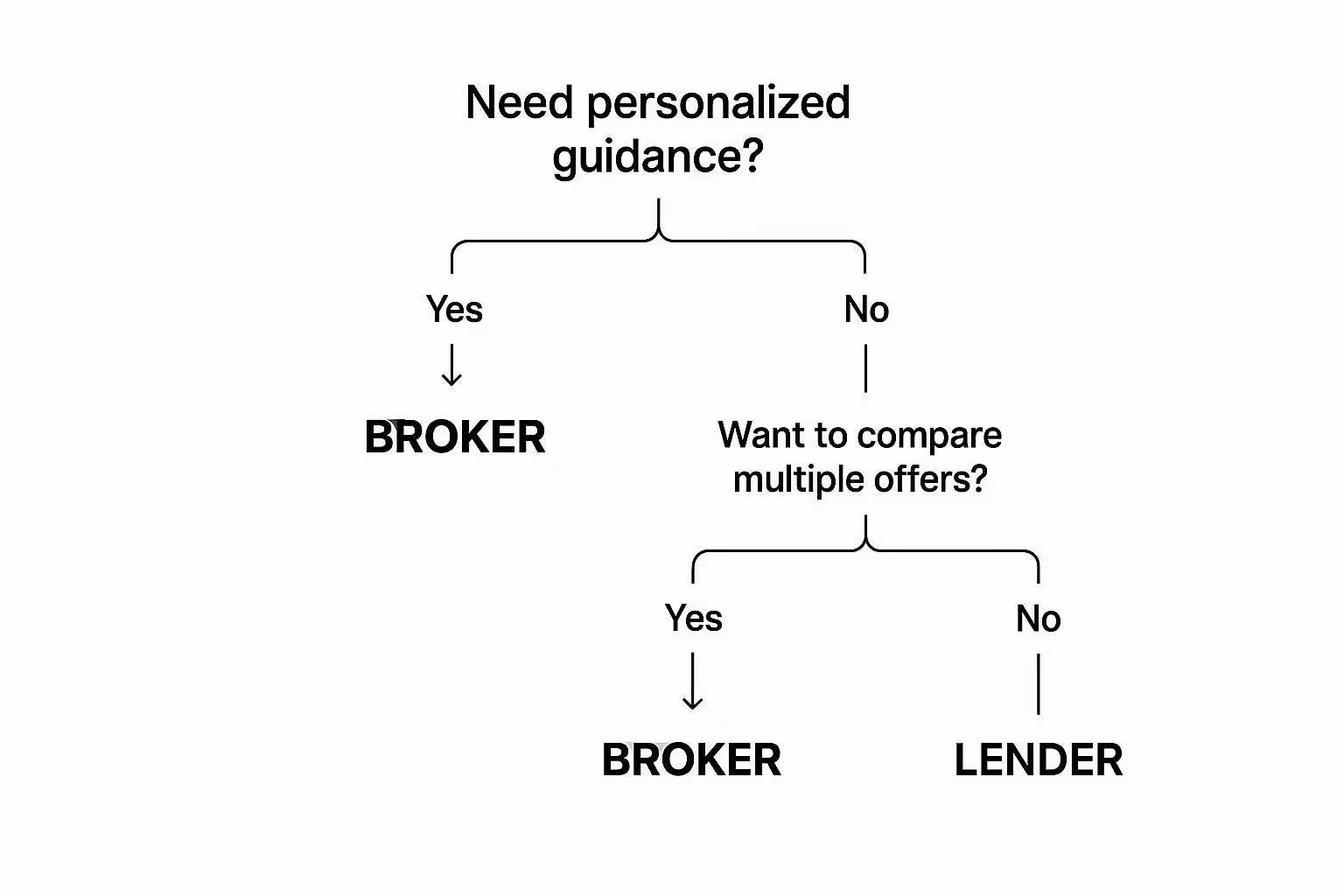

To get a quick sense of which path might be better for you, take a look at this decision tree. It helps frame the choice from the get-go.

As you can see, the decision often boils down to whether you prefer personalized guidance and a one-stop-shop for comparing offers—two of the biggest strengths a broker brings to the table.

Scenarios That Favor a Mortgage Broker

A good mortgage broker is more than just a middleman; they're a strategist. Their value becomes undeniable when your situation has a few extra layers of complexity.

Here are a few times when a broker is probably your best bet:

- You're a First-Time Homebuyer: Feeling lost in the jargon and paperwork? A broker acts as your personal guide, explaining every step and handling the back-and-forth with lenders so you can breathe easier.

- You Have a "Story" to Tell: This could mean a credit score that’s good but not perfect, some past financial hiccups, or a unique employment situation. Brokers are pros at framing your application to highlight its strengths and get it in front of the right people.

- You Value Convenience Above All: If the thought of filling out application after application and trying to compare a dozen different Loan Estimates makes your head spin, a broker is your hero. You fill out one application, and they do all the shopping for you.

The financial impact here is very real. A major study using Home Mortgage Disclosure Act (HMDA) data found that borrowers who worked with an independent mortgage broker saved an average of $10,662 over the life of their loan compared to those who went with a nonbank retail lender. You can read the full research about these borrower savings.

Scenarios That Favor a Direct Lender

Going straight to a bank or credit union can make a lot of sense when your priorities are speed, simplicity, and an established relationship. If your finances are straightforward, cutting out the intermediary is often the most efficient path.

You might lean toward a direct lender if:

- You Have a Simple Financial Profile: With a strong credit history and a stable W-2 income, you're the perfect candidate for a bank's streamlined, in-house approval process.

- You Prioritize an Existing Banking Relationship: Many big banks and credit unions reward their long-term customers with relationship-based discounts or preferred pricing on mortgages. It pays to ask.

- You Are Considering a Portfolio Loan: Some lenders offer special in-house loans with their own flexible rules. These portfolio loans aren't sold on the secondary market, so a broker wouldn't even have access to them.

The thought process is a lot like deciding whether to refinance. You have to carefully weigh your current situation against the potential benefits, and that means asking the right questions. Before you commit, it’s a good idea to review the 10 essential questions to ask before refinancing to save more, as many of the same core principles will apply.

So, How Do You Choose?

Alright, you've seen the side-by-side breakdown. You understand the core differences between a mortgage broker and a direct lender. Now comes the most important part: deciding which path makes the most sense for you.

This isn't about one being universally "better" than the other. It's about alignment. Think of it as matching a professional's specific skillset to your financial picture, your comfort level, and the kind of experience you want. Let’s cut through the noise and make this simple.

When to Go With a Mortgage Broker

A great mortgage broker is like a personal shopper for home loans. They thrive on complexity and variety, making them an incredible asset when your situation isn't a perfect, cookie-cutter scenario.

You should lean toward a broker if:

- You want someone to do the heavy lifting. If the thought of calling ten different banks gives you a headache, a broker is your champion. They shop the market for you, comparing rates and products from dozens of lenders to find a great fit. It's a huge time-saver.

- Your financial story is a little complicated. Are you self-employed? Have a unique income stream? Is your credit score a work in progress? A broker's real value shines here. They know which niche lenders welcome these profiles and can find a path to "yes" when a big bank might say "no."

- You're a first-timer feeling a bit lost. The mortgage world is full of jargon and endless paperwork. A good broker is your personal translator and project manager, guiding you through every step and handling the back-and-forth communication. That support can be priceless.

When a Direct Lender Is the Right Call

Going straight to the source—your bank, a local credit union, or a major online lender—is often the cleanest and most efficient route, especially when your application is straightforward.

A direct lender is probably your best bet if:

- You have a clean, simple financial profile. If you've got a solid credit score, a low debt-to-income ratio, and a steady W-2 job, you're exactly the kind of applicant lenders love. Their in-house process is built for you, and it can be incredibly fast and smooth.

- You already have a banking relationship you trust. Many banks and credit unions reward loyalty. Before you do anything else, ask your current institution about relationship discounts or preferred rates on a mortgage. You might be surprised by what they can offer.

- You want to sit across the desk from someone. There's a lot to be said for face-to-face service. If you value being able to walk into a local branch and talk things over with your loan officer in person, a traditional bank or credit union is the way to go.

At the end of the day, there’s no wrong answer—only the right answer for you. Whether you choose a broker to scan the entire market or a direct lender you already know and trust, the goal remains the same: getting the right key to unlock your new front door.

Answering Your Key Mortgage Questions

Even after weighing the pros and cons, a few crucial questions always seem to surface. Let’s tackle them head-on, so you can move forward with total confidence in your decision.

Can a Mortgage Broker Truly Get Me a Better Interest Rate?

It’s not a guarantee, but they often have a real advantage here. Think of it like this: a broker submits your single application into a competitive arena, making dozens of wholesale lenders fight for your business. This is where their power lies. That competition is what can really nudge the rates down, especially if you have a tricky financial picture, like being self-employed or having a unique income structure.

That said, if you’ve been banking with the same institution for years, they might pull out a loyalty discount or special offer that a broker can’t touch. The bottom line is that a broker casts a much wider net, which improves your odds, but a long-standing relationship with a direct lender can sometimes pay off in unexpected ways.

Who Closes Faster: a Broker or a Direct Lender?

For a simple, straightforward loan, a direct lender usually wins the race. Their entire operation—from the person who takes your application to the underwriter who approves it—is under one roof. This internal system means fewer handoffs and a more streamlined, controlled process.

Working with a broker adds one more link to the communication chain. A great broker will manage this flawlessly, but the simple reality is that coordinating between you and a completely separate company can sometimes add a few days to the closing timeline.

Here’s what it all boils down to: There’s no single "best" answer. Your personal situation is what truly matters. If you have a standard W-2 job and a great credit score, you'll probably love the speed of a direct lender. But if you're a freelancer, the market access a broker provides is invaluable.

Are There Hidden Fees With Mortgage Brokers?

"Hidden" isn't quite the right word, but their fee structure is definitely different, and it's something you need to understand. Most brokers are paid through what's called Lender-Paid Compensation (LPC). Essentially, the lender they place your loan with pays their commission, which is typically 1-2% of the loan amount.

This fee is baked directly into the interest rate you get. So while you won't see a separate line item for the "broker fee" on your closing documents, it's part of the overall cost. This is a key difference between a mortgage broker and lender, as a lender’s charges will appear as clear origination and processing fees on your Loan Estimate. To get a true apples-to-apples comparison, always look at the Annual Percentage Rate (APR), not just the interest rate.

At Tiger Loans Inc, we operate as both a direct lender and a broker, which gives our clients the best of both worlds. Whether you need the streamlined speed of our in-house lending or the massive optionality of our broker network, our team is built to find the perfect financing for your home.

Ready to explore your options? Start your journey with Tiger Loans Inc today!

Alex Chen

Alex Chen

Get in touch with a loan officer

Our dedicated loan officers are here to guide you through every step of the home buying process, ensuring you find the perfect mortgage solution tailored to your needs.

Options

Exercising Options

Selling

Quarterly estimates

Loans

New home

Stay always updated on insightful articles and guides.

Every Monday, you'll get an article or a guide that will help you be more present, focused and productive in your work and personal life.

.png)

.png)

.png)

.avif)

.avif)

.avif)

.png)

.png)

.png)

.avif)

.png)

.png)

.avif)

.png)

.avif)

.png)

.avif)

.avif)