Do Student Loans Affect Buying a House? Tips & Insights

November 19, 2025

Wondering do student loans affect buying a house? Learn how they influence your mortgage chances and get expert tips to navigate student debt and homeownership.

Of course. Here is the rewritten section, crafted to sound like it was written by an experienced human expert.

So, can you actually buy a house with student loans? The short answer is absolutely yes. But it’s not quite that simple.

Think of your student debt less as a roadblock and more as a major intersection on your road to homeownership. Lenders need to see exactly how you're navigating it, and how it fits into your larger financial picture. It's a solvable problem, but one you have to face head-on.

How Student Loans Really Affect Buying a House

Let’s be honest, trying to get a mortgage while carrying student debt can feel daunting. I’ve seen countless aspiring homeowners walk in worried their education debt automatically disqualifies them. The good news? It doesn't.

Your student loans influence a lender’s decision in two main ways: through your credit history and, most critically, through your debt-to-income (DTI) ratio.

A long history of paying your student loans on time is a huge plus. It shows lenders you’re reliable and know how to manage your obligations—a green flag for any mortgage underwriter. But if you've missed payments or, worse, defaulted, that’s a red flag that will need to be addressed.

Still, the real make-or-break factor is almost always the DTI ratio.

Before we get into the weeds, here's a quick look at the main pressure points your student loans put on your mortgage application.

Key Ways Student Loans Impact Your Mortgage Application

This table gives you the 30,000-foot view. Now, let’s zoom in on the one that matters most.

The Debt-To-Income Connection

At the end of the day, a lender’s biggest question is: "Can you realistically afford this mortgage payment on top of everything else you owe?" Your DTI ratio is how they answer that question. It’s a simple formula, but its impact is massive.

A hefty student loan payment can inflate your DTI, sometimes to the point where lenders get nervous. This isn't just an individual challenge; it's a well-documented trend we've seen play out on a national scale.

Since 2005, there’s been a direct link between soaring student debt and a dip in homeownership for younger generations. For every $1,000 increase in student loan debt, the homeownership rate has dropped by about 1.8%. You can explore the data behind student loan debt's effect on homeownership on EducationData.org.

This statistic isn't meant to scare you. It's meant to show you that you're not alone in this and that a smart strategy is essential. The key is understanding exactly how lenders will calculate your specific student loan payments and building your homebuying plan around that number. Your debt isn't a dead end—it's just a variable you need to learn how to manage.

Understanding Your Debt-To-Income Ratio

If you walk into a lender's office and ask how your student loans will affect your chances of buying a house, the first thing that pops into their head is your debt-to-income (DTI) ratio. It’s the single most important number they’ll look at.

Think of it as a financial stress test. It tells a lender, in one simple percentage, how much of your monthly paycheck is already spoken for before you even think about a mortgage.

Picture your gross monthly income as a freshly baked pie. Every existing debt payment—your car loan, credit card minimums, and yes, your student loans—is a slice that’s already been claimed. The more pie you have left, the more confident a lender feels about you being able to handle a mortgage payment. That's why a lower DTI makes you a much more attractive borrower.

Ultimately, this ratio is what determines how much house you can realistically afford. Your student loan payment, whether it's a few hundred dollars or much more, is a major ingredient in that recipe and can seriously limit your borrowing power.

How Lenders Calculate Your DTI

The math itself is surprisingly simple. Lenders just add up all your monthly debt payments and divide that number by your gross (pre-tax) monthly income. If you want to get into the nitty-gritty, we've got a full breakdown in our guide on how to calculate your debt-to-income ratio.

Let's walk through a quick example.

- Gross Monthly Income: $6,000

- Student Loan Payment: $350

- Car Payment: $400

- Credit Card Minimums: $150

In this case, you’d divide $900 by $6,000, which gives you 0.15, or a DTI of 15%. From a lender’s perspective, that’s fantastic. It means you have plenty of income left to comfortably take on a mortgage.

The Magic Number Lenders Look For

So what’s the target DTI? While there's some wiggle room depending on the loan type and lender, the gold standard is 43% or lower. And that’s including your potential new mortgage payment.

If your DTI is already pushing that limit before a house payment is even factored in, you’re going to have a tough time getting approved. This is exactly where student loans can throw a wrench in your homeownership plans—by taking up too much of that precious 43% allowance.

A high student loan payment can be the single biggest obstacle in your DTI calculation. It's not the total debt that spooks lenders, but the size of the monthly payment that reduces your capacity to handle a new mortgage.

How Different Repayment Plans Affect Your DTI

Now, here’s where things get really interesting. The type of student loan repayment plan you're on can completely change how a mortgage lender sees your finances.

- Standard Repayment Plan: This one's easy. Lenders see a fixed, predictable payment and will simply use the actual monthly amount listed on your statement.

- Income-Driven Repayment (IDR) Plans: Plans like PAYE or REPAYE can lower your payment drastically, sometimes even to $0 per month. This is where lender rules can get tricky. For conventional loans, some lenders will happily accept that $0 payment and move on.

- FHA Loan Rules: The FHA, on the other hand, plays by a different set of rules. They won't use a $0 payment. Instead, they’ll calculate a "phantom" payment, typically using 0.5% of your total loan balance. On a $60,000 student loan, that means they’ll add a $300 monthly payment to your DTI, even if your actual bill is zero.

Getting familiar with these details is crucial. Your student loan repayment strategy isn’t just about managing debt; it’s about strategically positioning yourself to get a "yes" from a mortgage lender.

How Student Loans Shape Your Credit Score

While your Debt-to-Income (DTI) ratio gets a lot of the attention, your credit score is the other major piece of the homebuying puzzle—and your student loans have a direct say in it. Think of your credit score as your financial report card. Your student loans are like a long-term class that mortgage lenders will be grading you on. How you've managed this debt can either build a powerful case for your reliability or raise some serious red flags.

Your student loan history is essentially a story you’re telling lenders about your financial habits. Every on-time payment is a chapter that says, “I’m responsible and can be trusted with a large loan.” It’s a powerful narrative because payment history is the single most important factor in your credit score. A long record of consistent student loan payments is one of the best ways to prove you're a good bet.

The Power of Positive Payments

When managed well, your student loan account is a huge asset. It positively influences several key areas that the major credit scoring models, like FICO and VantageScore, look at when calculating your score.

- Payment History (35% of your score): This is the heavyweight champion. Making your payments on time, every time, shows you can handle your financial obligations.

- Length of Credit History (15% of your score): For many people, student loans are one of their very first credit accounts. Keeping this long-standing account in good health demonstrates financial stability over time.

- Credit Mix (10% of your score): Lenders like to see that you can successfully manage different kinds of credit. A student loan is an installment loan (where you pay a fixed amount over a set period), which adds healthy diversity to your credit profile, especially when you also have revolving credit like a credit card.

So, your student debt isn't just a liability. It's actually a fantastic opportunity to build a strong credit foundation that will support you when it's time to apply for a mortgage.

The Damage of Missed Payments

On the other hand, letting your student loans slide can cause significant damage and make buying a house much harder. Just one late payment can cause your score to drop, and a default is even worse—it can haunt your credit report for years.

This became a harsh reality for many when the pandemic-era freeze on federal loan payments ended. That shift led to a spike in loan delinquencies, with nearly 8% of borrowers falling behind in early 2024. Those missed payments directly harm credit scores, which in turn hurts their chances of qualifying for a home loan.

To a lender, a recent history of missed student loan payments screams risk. It suggests you might struggle to handle the new, much larger responsibility of a mortgage, making them think twice about approving your application.

If your score has taken a hit from a few late payments, don't panic. Building it back up is completely achievable with the right strategy. For some concrete, actionable steps, check out our guide on how to improve your credit score quickly to get approved for a home loan.

Finding The Right Mortgage Program For You

Trying to find a mortgage when you have student loans can feel like searching for a hidden key. The great news? There isn't just one key that fits. Different mortgage programs look at student loan debt in surprisingly different ways, and picking the right one is often the secret to getting your application across the finish line.

It helps to think of it like this: not every lender plays by the same rulebook. Some are incredibly strict, but others build in flexibility that can be a real lifesaver for anyone carrying a hefty student debt load. Getting a handle on these differences is your first step. It equips you to have a smart, strategic conversation with your lender and find a program that actually works with your financial picture, not against it.

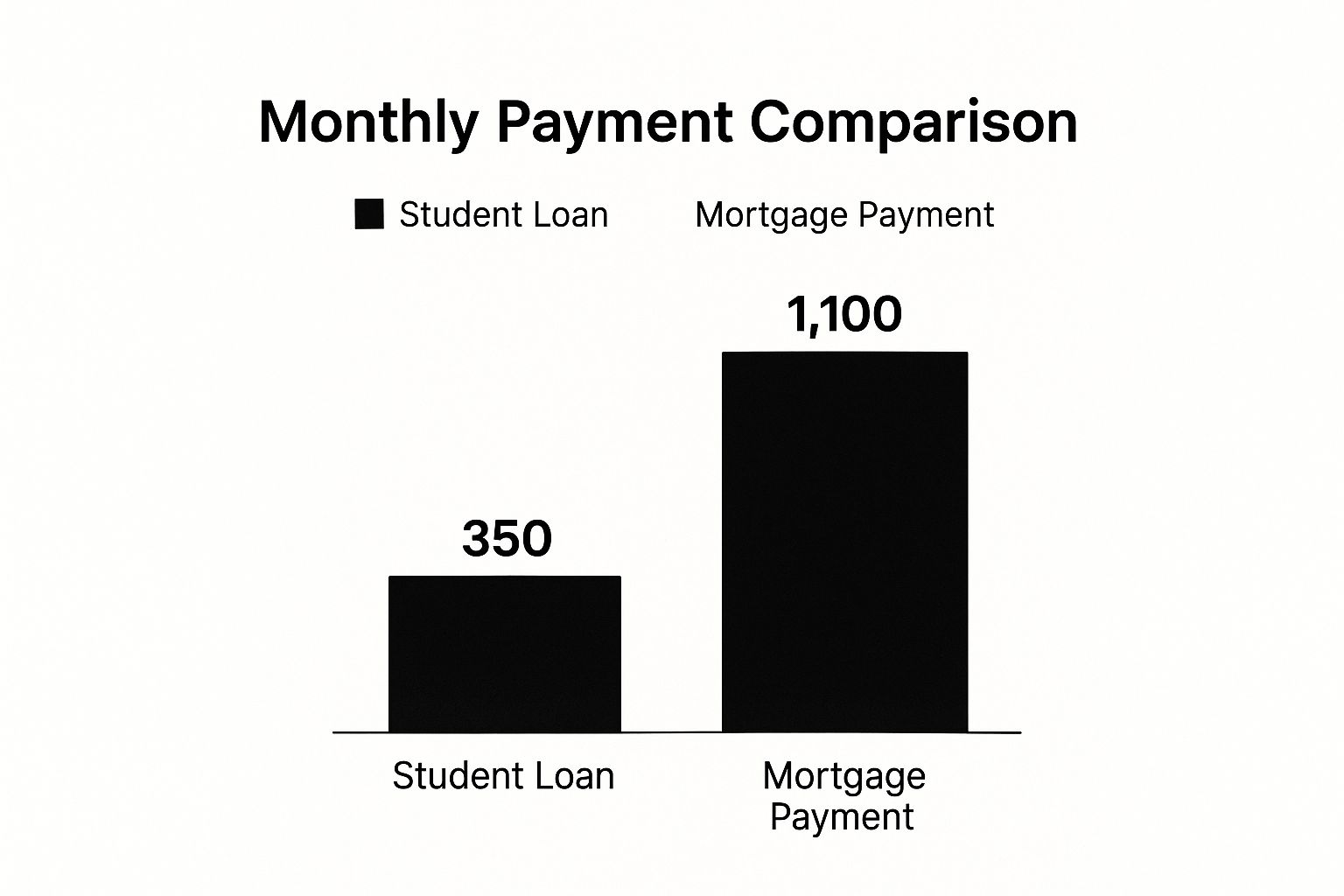

To really see how these two major monthly expenses stack up, take a look at the average payments for student loans versus mortgages.

This visual really drives the point home. It shows why lenders pay such close attention to the balance between your existing student debt and the new, much larger commitment of a mortgage.

Comparing Mortgage Loan Options

Each type of mortgage has its own set of guidelines for handling student debt, particularly when it comes to your DTI ratio. This is where things get interesting, and where you can find a real strategic advantage.

Let's break down how the major loan types see your student loans. It’s crucial to understand these differences because it directly impacts how much home you can afford.

How Different Mortgage Programs Calculate Student Loan Payments

As you can see, the program you choose can completely change the math. A borrower with a large student loan balance but a low IDR payment would have a much lower DTI under a conventional loan compared to an FHA loan.

This is a powerful piece of information to have in your back pocket.

Your choice of mortgage program is one of the most powerful strategic decisions you can make. A borrower who might be denied for an FHA loan due to a high DTI calculation could potentially qualify for a conventional loan with the exact same financial profile.

Knowing these rules before you apply allows you to guide your application toward the program that sees your finances in the best possible light. For an even more thorough breakdown of the financing process, this guide is an excellent a crash course in financing your first home.

In the end, it’s all about finding the right lender and the right loan. With a little bit of knowledge, you can turn what seems like a major roadblock into a clear path toward homeownership.

Proven Strategies to Improve Your Home Buying Odds

Feeling a little overwhelmed by all this? That’s perfectly normal. But now is when you shift from just understanding the hurdles to actively clearing them. Having student loans doesn’t lock you out of homeownership; it just means you need a smarter game plan. With the right moves, you can seriously strengthen your mortgage application and get the keys to your own place.

This isn’t just theory. We’re talking about concrete, actionable steps to put you in the strongest possible financial position. It’s no secret that student debt often pushes homeownership further down the road. In fact, surveys show about 29% of American adults have put off buying a house specifically because of student loans. You can dig into more of the data on how student loans impact homeownership readiness on FreedomMortgage.com. Let's build a strategy to make sure you're not part of that statistic.

Start with a Pre-Approval

Before you even think about scrolling through listings, get pre-approved for a mortgage. This is the single most important first step you can take. A pre-approval letter is a lender’s conditional promise to loan you a specific amount, and it’s your golden ticket to knowing what you can actually afford.

Think of it as a financial dress rehearsal. A lender will pull back the curtain on your income, assets, credit, and—crucially—your student loan situation. This process gives you a crystal-clear picture of your borrowing power from their perspective. It turns your house hunt from a wishful guessing game into a focused, realistic search.

Optimize Your DTI and Credit

When a lender looks at your file, two numbers will jump out: your Debt-to-Income (DTI) ratio and your credit score. Nudging these numbers in the right direction, even slightly, can make a world of difference.

- Tackle High-Interest Debt First: Before you throw extra cash at your student loans, go after any high-interest credit card debt. Wiping out a credit card or two can quickly lower your DTI and often gives your credit score a nice little boost.

- Check Your Repayment Plan: If you're on an Income-Driven Repayment (IDR) plan with a manageable monthly payment, a Conventional loan could be a great fit. Many lenders will use that smaller payment when calculating your DTI, which works in your favor.

- Pause on New Credit: In the months before you apply for a mortgage, avoid opening new credit cards or financing a new car. Every "hard inquiry" on your credit report can cause a temporary dip in your score.

Getting pre-approved is like getting the answers to the test ahead of time. It tells you exactly where you stand and what you need to work on before you start seriously looking at homes.

Explore Down Payment Assistance

For many aspiring homeowners with student loans, the biggest obstacle is scraping together a down payment. But here’s the good news: you probably don’t need to save as much as you think. The idea that you must have a 20% down payment is one of the most persistent myths in real estate.

Look into down payment assistance (DPA) programs in your area. Many state and local governments offer grants or forgivable loans to help first-time homebuyers get over the finish line. A quick search for "down payment assistance programs in [Your State]" can reveal options you never knew existed, potentially saving you thousands. These programs can also help with closing costs and other expenses, so it pays to understand the 5 hidden costs of buying a home that pop up along the way.

The Reality of Saving for a Down Payment

For so many of us trying to buy a home, the biggest question is brutally simple: how can you possibly save for a down payment when your student loans take a huge bite out of every single paycheck? It’s a frustrating reality, and if you feel like you're stuck, you're not alone. This is the number one reason many people have to put their homeownership dreams on hold.

First, let's get one huge misconception out of the way. You do not always need a 20% down payment. While putting more down is great—it lowers your monthly mortgage and helps you dodge Private Mortgage Insurance (PMI)—plenty of fantastic loan programs are designed to get you into a home for much less. FHA loans, for example, can get you through the door with as little as 3.5% down.

That’s a sigh of relief for anyone watching their savings account barely keep its head above water against their student debt.

It's a widespread struggle. A report from the National Association of REALTORS® found that student loans are the top obstacle for buyers trying to save. In fact, a massive 52% of buyers who had trouble saving pointed directly at their student loans, which delayed their home purchase by a median of four years. You can dig deeper into how student debt impacts saving for a house on PremierMtg.com.

The Big Trade-Off: Pay Down Debt or Save for a House?

This leads you to a major financial crossroads. Should you go scorched-earth on your student loans, or should you pour all your extra cash into saving for a house? Honestly, there’s no single right answer—it all comes down to what matters most to you.

Let's walk through two common approaches:

The Debt Avenger: You decide to throw every spare dollar at your student loans. It feels incredible to watch that balance drop, and it will absolutely help your DTI ratio in the long run. The downside? Your down payment fund grows at a crawl, and your dream of owning a home gets pushed further down the road.

The Homeowner Hopeful: You stick to making just the minimum payments on your student loans and instead funnel that extra cash into a high-yield savings account earmarked for your down payment. You'll hit your savings goal much faster this way, but that student loan balance will hang around, which could still affect your DTI when it's time to apply for a mortgage.

Neither path is inherently better than the other. The trick is to sit down and run the numbers for your own life. Do you crave the freedom of being debt-free more, or is the idea of holding the keys to your own home your top priority? Figuring that out is the first real step toward building a strategy that gets you to the future you actually want.

Still Have Questions About Student Debt and Homeownership?

It's completely normal to have a few lingering "what ifs" even after you've mapped out a plan. Let's walk through some of the most common questions I hear from aspiring homeowners who are also managing student loans. Getting these answers can give you the confidence you need to take the next step.

Can I Get a Mortgage if My Loans Are in Deferment or Forbearance?

Yes, you absolutely can, but there's a catch. Lenders won't simply pretend that debt doesn't exist just because you aren't making payments right now.

Instead, they have to account for a future payment. For government-backed loans like FHA and VA, they’ll typically estimate a monthly payment—often calculated as 0.5% to 1% of your total loan balance—and factor that number into your DTI. Every lender has slightly different rules, so make it a point to ask them directly how they handle deferred loans.

Should I Pay Off All My Student Loans Before Trying to Buy a House?

This is a big one, and the answer is usually no. It feels counterintuitive, I know. While wiping out your student loans sounds like the smartest move, it could completely drain the savings you’ve worked so hard to build for a down payment and closing costs.

Think of it as a strategic balancing act. It’s often much smarter to keep your student loans active with a manageable monthly payment and hold onto your cash for the actual home purchase.

When it comes to qualifying for a mortgage, lenders are almost always more concerned with your monthly payment than your total loan balance. That monthly payment is what directly impacts your debt-to-income ratio, which is the key metric for them.

Focusing on a reasonable payment allows you to manage your debt without sidelining your homeownership goals.

Ready to see how your specific situation fits into the homeownership puzzle? At Tiger Loans Inc, we specialize in finding the right mortgage solutions for borrowers with student debt. Get your free pre-approval today and see what's possible.

Alex Chen

Alex Chen

Get in touch with a loan officer

Our dedicated loan officers are here to guide you through every step of the home buying process, ensuring you find the perfect mortgage solution tailored to your needs.

Options

Exercising Options

Selling

Quarterly estimates

Loans

New home

Stay always updated on insightful articles and guides.

Every Monday, you'll get an article or a guide that will help you be more present, focused and productive in your work and personal life.

.png)

.png)

.png)

.avif)

.avif)

.avif)

.png)

.png)

.png)

.avif)

.png)

.png)

.avif)

.png)

.avif)

.png)

.avif)

.avif)