Ace Your Home Appraisal for Refinance

November 19, 2025

Unlock your home's true value. Our guide to the home appraisal for refinance process gives you the tools to prepare and maximize your outcome.

So, you’re thinking about refinancing your mortgage. At the heart of that process is one crucial step: the home appraisal. This isn't just some formality your lender makes you go through. It's a professional, in-depth assessment of your property's current market value, and it’s the bedrock of your entire refinance application. The number the appraiser comes back with will directly shape your new loan terms, your interest rate, and how much of your home's equity you can actually tap into.

Why Your Refinance Hinges on a Solid Home Appraisal

Think of the refinance appraisal as the moment of truth that determines your financial leverage. When you refinance, you’re asking a lender for a brand new loan. Before they hand over the money, they need to be absolutely sure it’s a sound investment on their end. Your home is the collateral that secures that loan, and the appraisal gives them an impartial, expert opinion on what that collateral is worth right now.

A strong appraisal can be your golden ticket. It can unlock a better interest rate, slash your monthly payments, or free up a significant chunk of cash if you’re doing a cash-out refinance. Simply put, a higher valuation puts you in the driver’s seat during negotiations.

The appraisal process boils down to a few key goals for both you and your lender. Here's a quick look at what it aims to achieve.

Key Goals of a Refinance Appraisal

ObjectiveWhy It Matters for Your RefinanceVerify Property ValueThe lender needs to confirm your home is worth enough to secure the new loan amount. A higher value means less risk for them.Calculate Your EquityThe appraisal is essential for determining your Loan-to-Value (LTV) ratio, which is a direct measure of your equity stake.Assess Property ConditionThe appraiser notes the overall condition and any significant issues, which can impact the home's final valuation and loan approval.Secure Favorable TermsA strong appraisal that shows you have significant equity can lead to lower interest rates and the avoidance of PMI.

Ultimately, a successful appraisal reassures the lender that their investment is safe, which in turn helps you secure the best possible deal.

Your Home's Financial Scorecard

The whole game really comes down to one critical metric: the Loan-to-Value (LTV) ratio. Don't get tripped up by the jargon; it’s just your home's financial scorecard. LTV is a simple percentage that compares how much you want to borrow against the home's appraised value.

LTV is calculated with a simple formula: (Loan Amount / Appraised Value) x 100. When it comes to LTV, lower is always better because it signals to the lender that you're a lower-risk borrower.

Let’s put it into practice. Say you want to refinance your remaining $300,000 mortgage and your home appraises for $400,000. Your LTV would be a healthy 75%. That kind of equity makes you a very attractive candidate for the best rates. But if that same home only appraises for $350,000, your LTV suddenly jumps to nearly 86%. That higher risk might limit your loan options or force you to pay for Private Mortgage Insurance (PMI).

Turning a Hurdle into a Tool

A lot of homeowners get nervous about the appraisal, seeing it as a hurdle they just have to clear. I encourage you to flip that mindset. See it as your opportunity to prove your home's real worth. This is your chance to show off all the hard work and money you've put into maintaining and improving the property. A high appraisal isn't just a number—it’s a validation of your investment and the equity you’ve worked so hard to build.

This step is especially critical for the most popular loan types. Conventional loans, which almost always require an appraisal, make up 46.4% of all mortgage applications. This shows just how central the appraisal is for the majority of homeowners looking to refinance. Even small shifts in property values, like the recent modest dip in average new home loan sizes to $376,992, can have a huge ripple effect on LTV and loan approvals. You can discover more insights about mortgage application trends on MBA.org.

By truly understanding what appraisers look for, you can transform this mandatory step from a source of anxiety into a powerful tool that helps you achieve your financial goals—whether that’s saving money every month or funding your next big life adventure.

What Appraisers See: A Guided Tour of Your Home's Value

To really wrap your head around the home appraisal for refinance, you have to learn to see your home through an appraiser's eyes. They aren't there to critique your family photos or your taste in paint colors. Their visit is all about one thing: gathering objective facts about your property's condition, quality, and overall functionality.

Think of them as property detectives. They're on a mission, methodically piecing together clues to build a solid case for your home's current market value. Let's walk through your property just like they would, from the curb to the crawlspace.

The Exterior: A First Impression That Counts

The appraisal begins the second the appraiser pulls up to your home. That term "curb appeal" isn't just a cliché for home improvement shows; it’s the opening argument for your property’s upkeep. A tidy, well-maintained exterior telegraphs that the inside is likely cared for, too.

Here’s what immediately catches their eye:

- Structural Integrity: They're scanning for obvious issues like cracks in the foundation, rotting wood on the siding or trim, and the general condition of the exterior walls.

- Roof and Gutters: The roof's age and condition are huge. Are shingles missing, curling, or covered in moss? Are the gutters sagging or pulling away from the house?

- Yard and Landscaping: A neat lawn, fresh mulch, and healthy trees all contribute to a positive impression and what we call "perceived value."

- Additional Features: Decks, patios, fences, and pools are all part of the equation. Their condition is what matters—are they a well-maintained asset or a potential liability waiting to happen?

A deck with peeling stain or a roof that's clearly seen better days sends up an immediate red flag. These aren't just cosmetic blemishes; they represent real, tangible costs that a new owner (or the bank, in a foreclosure) would have to sink into the property.

Stepping Inside: The Interior Assessment

Once they cross the threshold, the appraiser’s focus shifts to the heart of your home's value. They’ll get right to work, measuring rooms to confirm the official gross living area (GLA)—one of the most important metrics in their report. They'll also document the official count of bedrooms and bathrooms.

But it goes much deeper than just the numbers. They're also assessing the quality and condition of your interior spaces.

The appraiser's real goal is to determine the "effective age" of your home. A 50-year-old house with a sparkling new kitchen, updated bathrooms, and modern systems might have an effective age closer to 15 years, which can significantly lift its value.

This concept of effective age is absolutely crucial. It’s why a home with a pristine but dated 1980s kitchen gets a very different value than one with a fully renovated, modern culinary space. The appraiser is constantly looking for signs of updates versus wear and tear.

Kitchens and Bathrooms: The Value CentersThese two rooms carry the most weight when it comes to interior valuation. An appraiser will be taking detailed notes on:

- Appliances: Are they modern, energy-efficient, and in good working order?

- Countertops and Cabinets: What are they made of, and what condition are they in? Granite or quartz will always appraise higher than older laminate.

- Fixtures: Upgraded sinks, faucets, and lighting all add up.

- Overall Condition: They’ll keep an eye out for leaky faucets, water damage under the sinks, and general wear.

Living Spaces and BedroomsIn the rest of the house, the focus is on general condition and flow. They’ll note the type and condition of the flooring (is it worn carpet or gleaming hardwood?), the state of the walls and ceilings, and whether the windows and doors function properly. The floor plan itself is also a factor—an open, intuitive layout is almost always more desirable than a choppy, closed-off one.

Behind the Walls: Systems and Structure

An appraiser’s job goes beyond what you can see. They also need to evaluate the core systems that make a house a safe and functional home. This part of the home appraisal for refinance is less about style and all about the property's operational health.

They will identify and assess these major components:

- HVAC System: The age and working condition of your furnace, air conditioner, and ventilation systems are carefully documented. A new, high-efficiency system is a major plus.

- Electrical and Plumbing: They’ll look for visible clues of modernization. An updated electrical panel is a great sign, while old knob-and-tube wiring is a concern. Modern plumbing like copper or PEX is valued over older galvanized pipes.

- Energy Efficiency: Appraisers are trained to spot value-adding features like double-pane windows, proper attic insulation, and energy-efficient appliances.

In the end, the appraiser synthesizes all these observations—from the landscaping out front to the furnace in the basement—to build a comprehensive profile of your home. This detailed tour is what allows them to create a factual, defensible report that truly reflects your home’s standing in the current market.

How Your Neighborhood Shapes Your Home's Worth

When it comes to your home's value during a refinance, what happens inside your four walls is only half the story. The single most powerful factor is often something you can't control at all: the homes that have recently sold right around you.

Think of it like this: your property is being graded on a curve. The appraiser's job is to act like a detective, digging up the sales of similar nearby homes to build a rock-solid case for your home's current market value. These are known as comparable sales—or "comps," as we call them in the business—and they are the absolute foundation of your appraisal report.

The Power of Comparable Sales

Comps are the bedrock of the entire appraisal process. The main valuation method, the sales comparison approach, is built on a simple principle: a buyer won't pay more for your property than what a nearly identical one just sold for. It’s just common sense.

Because of this, an appraiser's primary task is finding the best possible matches for your home. They’re on the hunt for properties that mirror yours in a few key ways.

What makes for a truly powerful comp?

- Proximity: The closer, the better. Ideally, comps are pulled from your subdivision or within a one-mile radius.

- Recency of Sale: A sale from last month is gold; one from last year is practically ancient history. Appraisers are laser-focused on sales within the last 90 days and rarely go beyond six months unless they absolutely have to.

- Physical Similarity: This is about comparing apples to apples. They look at style (is it a ranch or a two-story colonial?), square footage, the number of bedrooms and bathrooms, lot size, and overall condition.

An appraiser’s final number isn't just pulled out of thin air. It’s a carefully calculated value derived from three to five of the strongest, most recent comparable sales. This ensures the valuation is based on cold, hard market evidence—not just someone's opinion.

To get to that final number, the appraiser makes adjustments. If a comp has a brand-new kitchen but yours is dated, they'll subtract value from that comp's sale price to even the score. If your home has an extra bathroom that a comp lacks, they’ll add value to its price. This meticulous adjustment process is how they level the playing field to figure out what your home is really worth today.

Beyond the Four Walls

While your home's features are crucial, its location and the overall vibe of your neighborhood play an equally important role. Appraisers have to look at the bigger picture and consider all the external forces that influence what buyers are willing to pay.

Think of it as a peer review for your property. A beautiful home in a struggling area won't fetch the same price as the exact same house in a booming one. For example, a home that might easily appraise for $600,000 in a top-tier school district could be valued for much less just a few miles down the road in a different district.

Several key external factors have a direct impact on your bottom line:

- School District Quality: This is a huge one. For many families, it's non-negotiable, and homes in highly-rated districts consistently command premium prices.

- Local Market Trends: Is your area hot, with homes flying off the market and prices climbing? Or is it a slower, buyer's market? Appraisers make "market conditions" adjustments to account for this momentum.

- Neighborhood Amenities: Being close to parks, trendy shops, public transit, and good jobs adds real, tangible value.

- Property Taxes: While not a direct input to the valuation formula, sky-high property taxes can definitely make a home less attractive to buyers, which indirectly affects demand and value.

What to Do with a Weak Appraisal

Understanding how comps and neighborhood factors work is your best defense. If your appraisal comes in lower than you expected, the very first thing you should do is take a hard look at the comps the appraiser used.

Were they truly similar? Did the appraiser miss a more recent, more relevant sale right on your own street? Did they overlook a major upgrade you made, like a new roof or a finished basement that the comps didn't have? If you can find legitimate factual errors or point to better, more accurate comps, you can take that evidence to your lender. It’s often enough to successfully appeal the appraisal for a reconsideration of value.

A Strategic Guide to Maximizing Your Appraisal Value

Your home appraisal for refinance isn't something you just sit back and wait for. It’s your chance to step up and actively influence the outcome. Think of it like prepping your home for a showing, but your only guest is the person who holds the key to your financial future. A little bit of smart preparation can easily translate into thousands of dollars in home equity and help you lock in the valuation you need.

This isn’t about starting a massive, wallet-draining renovation a week before the appraiser shows up. Not at all. The real secret lies in focusing on high-impact, low-cost improvements that scream "well-maintained" and show off your home's true potential. You're basically becoming your home's best advocate, making sure its best features get the spotlight they deserve.

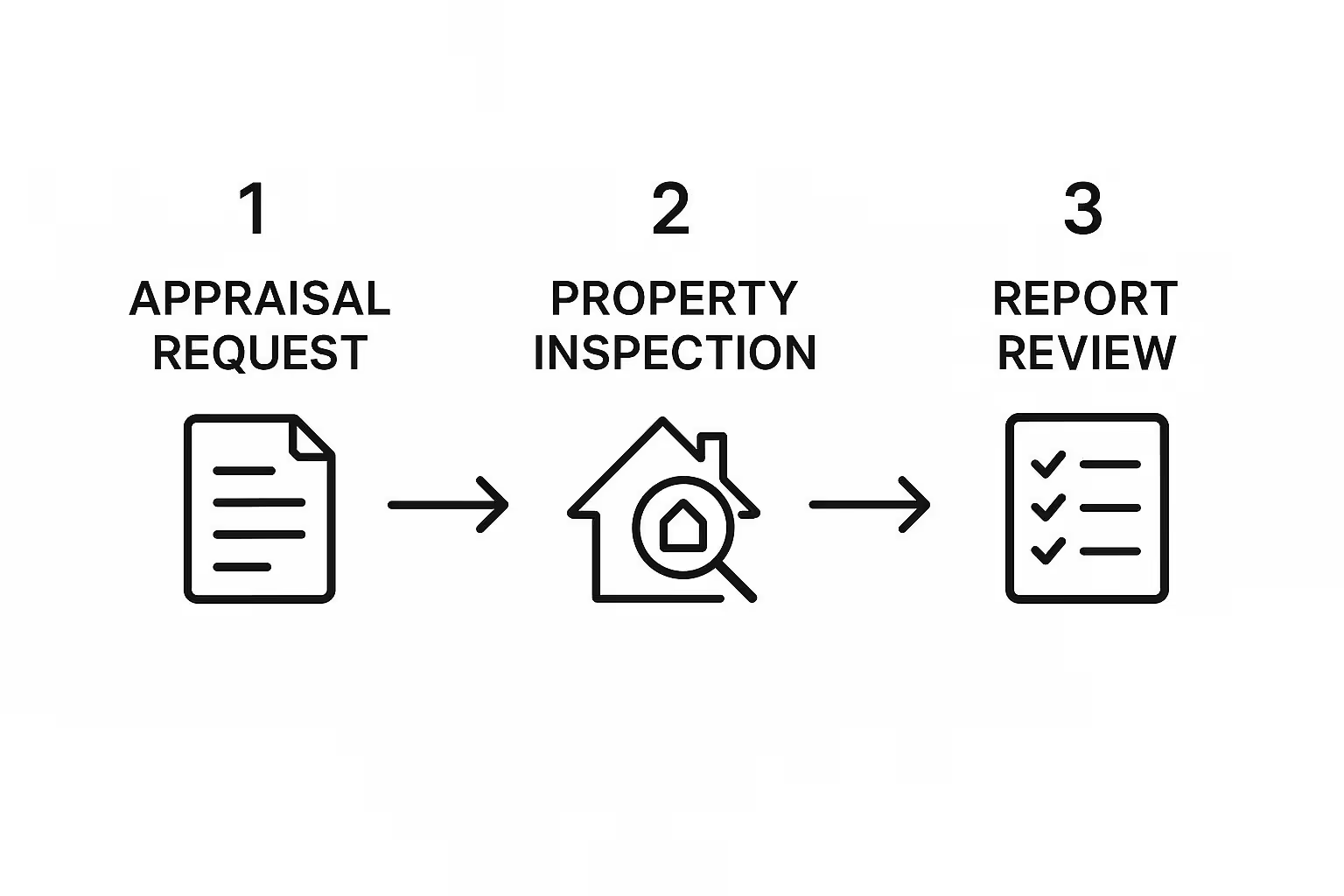

This image below breaks down the refinance appraisal journey, showing you exactly where the on-site inspection fits into the bigger picture.

As you can see, that property inspection is the hands-on moment where all your prep work really pays off, directly shaping the appraiser's final report.

The Weekend Warrior Checklist

If you’ve only got a weekend to spare, you can still make a huge difference. This isn’t about a complete overhaul; it’s about tackling the small stuff that adds up to a powerful first impression.

- Declutter and Deep Clean: This one is non-negotiable. Clear off those countertops, organize closets so they don't burst open, and make sure the floors are spotless. Clean, open spaces feel bigger and signal that a home is well-cared for. Remember, the appraiser is there to see the house, not your stuff.

- Tackle Minor Repairs: You know that leaky faucet, sticky door, or cracked switch plate you've been meaning to get to? Now’s the time. These little nagging issues can suggest neglect, which can subtly chip away at your home's perceived value.

- Freshen Up with Paint: A fresh coat of neutral paint is one of the cheapest and most effective ways to make a room feel bright, clean, and modern. Hit the high-traffic areas or any rooms with scuffed-up walls.

- Boost Curb Appeal: First impressions are everything. Mow the lawn, trim the bushes, lay down some fresh mulch, and maybe put a nice potted plant by the front door. Setting a positive tone before the appraiser even walks inside is a massive win.

Create a Homeowner's Brag Sheet

Here’s your secret weapon. The appraiser is a pro at valuing homes, but they can't read your mind. They have no way of knowing you installed a brand-new, top-of-the-line HVAC system last winter or that your roof is only two years old—unless you tell them.

This "brag sheet" is basically your home's resume. It's a simple, one-page document you hand to the appraiser that ensures none of your hard work and valuable upgrades go unnoticed.

Your brag sheet isn't a wish list or a list of complaints. It's a factual, organized summary of every significant investment you've put into the property. Be sure to present it politely when the appraiser arrives.

Keep it professional—typed, organized, and easy to scan.

What to Include on Your Brag Sheet:

- Major System Upgrades: List any new HVAC units, water heaters, electrical panel updates, or plumbing projects. Don't forget to include the installation date and the approximate cost.

- Significant Renovations: Did you remodel the kitchen or a bathroom? Finish the basement? Detail these projects and mention key features like new granite countertops, custom cabinets, or high-end fixtures.

- Exterior Improvements: Note the dates and costs for a new roof, replacement windows, siding, a new deck, or any major landscaping work.

- Energy-Efficient Features: If you've added new insulation, installed energy-efficient windows, or put up solar panels, make sure it's on the list.

Providing this document shows you have pride of ownership and gives the appraiser concrete data to justify a higher valuation in their report. To get strategic, you could highlight updates with a high kitchen renovation ROI, as this is something appraisers consistently rank as a top value-add.

Ultimately, taking these steps is about presenting your home in its absolute best light. You're giving the appraiser the documented proof they need to see its full worth. This effort could be the deciding factor between an average valuation and one that opens up incredible financial opportunities, whether you're trying to lower your rate or take out a large sum of cash. Deciding which path is best depends on your goals, and understanding the differences between a refinance vs. home equity loan is a great place to start.

Making Sense of Your Appraisal Report and Deciding What's Next

The appraisal report has finally hit your inbox. It’s a dense document, packed with the appraiser's research and inspection notes, and it's time to find out what they think your home is worth. It can look a little intimidating with all the technical jargon, but once you know what to look for, it's actually pretty easy to understand.

Think of the report as your home's official biography. It starts with the basics: legal description, tax records, and a rundown of the essentials like square footage, bed and bath count, and any special features. Your first job is to comb through this section for any mistakes. Something as simple as getting the square footage wrong or missing a bathroom can throw the final number off.

Understanding the Valuation and What It Means for You

As you flip through the pages, you'll hit the comparable sales section, often just called "comps." This is the heart of the report, where the appraiser lays out the nearby, recently sold homes they used to justify your property's value. Pay close attention here. Are these comps genuinely similar to your house in size, condition, and location? Sometimes an appraiser might use a sale from a less desirable block or a home that was in much worse shape.

Then you get to the grand finale: the appraised value. This single number is the key to your refinance. A good valuation can open up a world of financial opportunities, from snagging a much lower interest rate to tapping into your home's equity.

This is especially true if you’re doing a cash-out refinance. Using home equity has become a go-to financial tool for homeowners across the country. In 2021, cash-out refinances made up a massive 42% of all refinance mortgages, with the average homeowner pulling out $60,214. All told, Americans tapped into an estimated $248 billion in home equity that year, which just goes to show how much financial leverage is tied to your home's value. You can dig into the full trends report over on Freddie Mac's website.

What to Do If the Appraisal Comes in Low

Getting a low appraisal feels like hitting a brick wall, but it’s not a dead end. It’s easy to get frustrated, but the best approach is a calm and strategic one. You have the right to challenge the appraisal through a formal process called a Reconsideration of Value (ROV).

A Reconsideration of Value isn’t a complaint—it’s a formal request, backed by evidence, asking the appraiser to review their work based on new information you provide through your lender.

To build a solid case for an ROV, you need to bring facts, not feelings. Simply saying, "I think my house is worth more," won't get you anywhere. You need to give them concrete proof.

Here’s how you can mount an effective challenge:

- Pinpoint the Errors: Make a simple, clear list of any factual mistakes in the report. Did they list three bedrooms instead of four? Get the square footage wrong? Forget about your finished basement?

- Find Better Comps: If you know of a more similar home that sold nearby, give them the address and sale details. Your real estate agent can be your best friend here, helping you find stronger comps the appraiser might have overlooked.

- Present Your Brag Sheet: If you didn't give the appraiser a list of your home improvements before, now's the time. This provides documented proof of the money and effort you've invested in the property.

By presenting a professional, evidence-based challenge, you give yourself a real second chance. This proactive step can be the difference between a stalled refinance and one that gets you back on track to unlocking your home's full value. And if your main goal is to pull out cash, getting the highest possible valuation is critical. For a deeper dive, check out our guide on what is a cash-out refinance and how it all works.

What's Next? Appraisal Waivers and New Tech Are Changing the Game

If you're thinking the old-school, on-site appraisal is the only way to get a refinance done, think again. The mortgage world is getting smarter and faster. Thanks to some impressive technology and a mountain of data, lenders are now finding new ways to value your home—methods that can save you a ton of time and a nice chunk of change.

Picture this: your lender already has so much confidence in your home's value and your financial standing that they don't even need to send an appraiser to your door. That’s not a fantasy; it's an appraisal waiver, and it's becoming a popular shortcut for well-qualified homeowners.

How Lenders Are Using Automation

Lenders aren't just crossing their fingers and hoping for the best. They’re using incredibly sophisticated tools to decide if they can skip the traditional appraisal. The heavy hitters behind most U.S. mortgages, Fannie Mae and Freddie Mac, are leading the charge with their own powerful systems.

- Fannie Mae’s Property Inspection Waiver (PIW): This program dives into a massive database of property information using a system called Collateral Underwriter®. It crunches the numbers to see if your home's value is a safe bet.

- Freddie Mac’s Automated Collateral Evaluation (ACE): This works much the same way, using its own proprietary models to analyze risk and decide if an in-person visit is really needed.

These systems look at everything—from previous appraisals on your property to what your neighbors’ homes have sold for recently. If all the data points line up and the risk looks low, your lender gets the green light to waive the appraisal.

You can think of it like a "fast pass" for your refinance. When you have a solid payment history and plenty of equity in a stable market, your property essentially pre-qualifies for a quicker valuation. It’s a simple way to clear one of the biggest hurdles in the entire refi process.

And here’s the best part: getting one of these waivers is becoming more common. In 2025, the rules changed to allow some appraisal waivers for loans with a loan-to-value (LTV) ratio as high as 90%.

What does that mean for you? It means more homeowners now have a shot at skipping the appraisal fee, which often tops $500, and cutting weeks off their closing timeline. It’s worth digging into how appraisal waivers work in 2025 to see if you might be eligible. This is a huge leap forward, making refinancing a much smoother, data-driven experience for countless people.

Your Top Refinance Appraisal Questions, Answered

As you get closer to the finish line of your refinance, it’s completely normal for a few key questions to pop up. Getting straight answers is the best way to feel confident and in control. Let's walk through some of the most common things homeowners want to know about the appraisal process.

How Much Does a Refinance Appraisal Cost?

You can generally expect a refinance appraisal to cost somewhere between $400 and $700. This isn't a fixed number, though; it can fluctuate based on factors like your home's size, its unique features, and even your local real estate market.

As the homeowner, this fee is your responsibility. It's typically paid directly to the appraisal management company when your lender orders the report.

What if My Appraisal Comes in Too Low?

A low appraisal can feel like a major roadblock, but it's not the end of the world. Don't panic. The first thing you should do is get a copy of the report and review it with a fine-tooth comb. Look for simple, factual errors—did they list the wrong square footage, miss a bathroom, or overlook a key feature?

If you spot mistakes or feel the appraiser used poor "comps" (comparable sales), you have the right to challenge the valuation. You'll work with your lender to file what's called a "Reconsideration of Value."

Pro Tip: A successful challenge is all about the evidence. You can't just say you think your home is worth more. You need to come prepared with better comparable sales, receipts for recent upgrades the appraiser may have missed, and clear documentation of any factual errors you found in the report.

Is an Appraisal Always Required for FHA or VA Loans?

Not always! One of the biggest perks of programs like the FHA Streamline Refinance and the VA Interest Rate Reduction Refinance Loan (IRRRL) is that they often don't require a new appraisal at all. These programs are designed to be fast and simple, focusing on getting you a lower interest rate without all the usual hurdles.

Asking smart questions from the start is the key to a stress-free refi. To make sure you're fully prepared, check out these 10 essential questions to ask before refinancing for even more ways to save money and sidestep potential headaches.

At Tiger Loans Inc, our whole goal is to give you the expert support you need to navigate the refinance process with total confidence. Whether you’re trying to lock in a lower rate or pull out some equity, our team is ready to help you hit your financial targets. Explore your personalized mortgage options today.

Alex Chen

Alex Chen

Get in touch with a loan officer

Our dedicated loan officers are here to guide you through every step of the home buying process, ensuring you find the perfect mortgage solution tailored to your needs.

Options

Exercising Options

Selling

Quarterly estimates

Loans

New home

Stay always updated on insightful articles and guides.

Every Monday, you'll get an article or a guide that will help you be more present, focused and productive in your work and personal life.

.png)

.png)

.png)

.avif)

.avif)

.avif)

.png)

.png)

.png)

.avif)

.png)

.png)

.avif)

.png)

.avif)

.png)

.avif)

.avif)