Home Buying Process Timeline: Your Week-by-Week Guide

November 19, 2025

Learn the complete home buying process timeline to navigate every step confidently. Discover key milestones and tips to succeed.

Understanding Your Personal Home Buying Journey

Embarking on the path to homeownership is an exciting, deeply personal adventure, and it's crucial to recognize that there's no single home buying process timeline that applies to everyone. Understanding this right from the start is your first step to a smoother experience, saving you from potential frustration. Some fortunate buyers might find themselves with keys in hand in as little as 30 days, while for others, the search and purchase process could extend to six months or even longer.

Factors Shaping Your Timeline

Several key elements will actively shape the duration of your unique home buying journey. The prevailing market conditions, such as the current inventory of homes and the level of buyer demand, can dramatically influence your search. For instance, a competitive seller's market with few homes available often means you'll face more competition, potentially stretching out the time it takes to find your perfect property. Similarly, the intricacies of financing, from securing that vital pre-approval to navigating the final loan underwriting, are significant factors that sway your timeline.

Your personal circumstances also play a substantial role in how long your home buying process timeline will be. These can include how swiftly you can gather all the necessary financial documents or how much flexibility you have for viewing properties and making those important decisions. Recognizing which factors are within your control, like getting your financial house in order early on, versus those you'll need to adapt to, such as shifts in the market, is absolutely key. This awareness will empower you to set realistic expectations from day one.

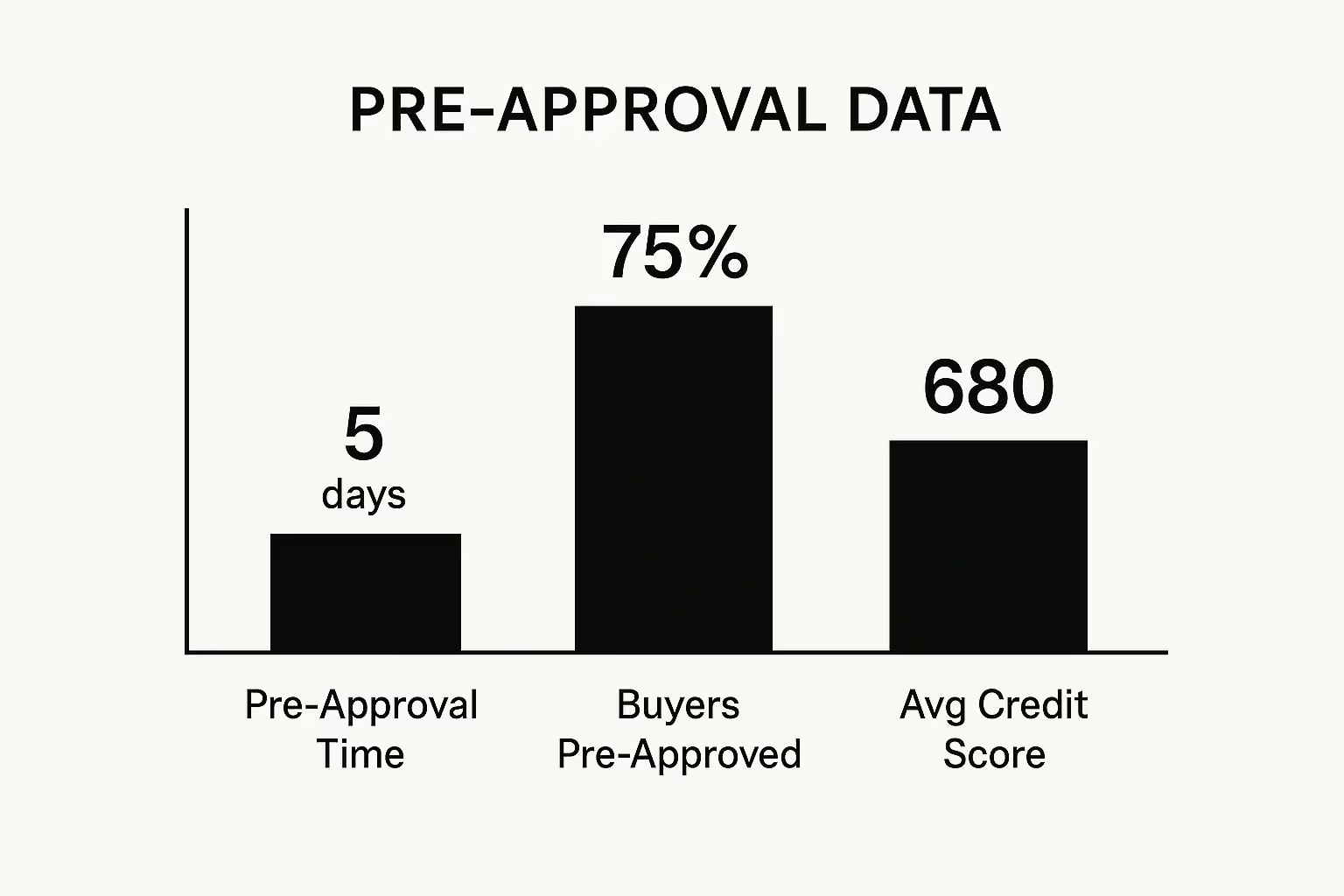

To give you an idea of a critical early step, the image below highlights key aspects of mortgage pre-approval, a cornerstone for a well-prepared buyer. This visual information reveals that while pre-approval can be relatively quick, often around 5 days, a commanding 75% of buyers successfully secure it. Typically, this involves an average credit score around 680, underscoring just how important this step is if you're aiming for an efficient home buying experience.

This visual information reveals that while pre-approval can be relatively quick, often around 5 days, a commanding 75% of buyers successfully secure it. Typically, this involves an average credit score around 680, underscoring just how important this step is if you're aiming for an efficient home buying experience.

Generational Nuances in Home Searching

Interestingly, the home buying process timeline can also reveal some fascinating differences when we look across various generations of buyers. In 2025, homebuyers on average are dedicating about 10 weeks to their property search, looking at a median of seven homes. However, this isn't set in stone; Younger Millennials and members of the Silent Generation often manage to find their ideal home more quickly, in about eight weeks. For a significant 55% of all buyers, the task of pinpointing the right property stands out as the most demanding part of the process, a challenge felt even more keenly by Younger Millennials, with 60% reporting this difficulty. The power of online resources is undeniable, with a staggering 86% of Older Millennials finding property photos to be the most valuable feature in their online search.

To give you a clearer picture of how these timelines can differ, let's look at a comparison of average search durations and key preferences across various buyer generations. This can help you situate your own expectations.

Home Buying Timeline by Generation

Comparison of average search duration and key preferences across different buyer generations

As you can see from the table, while there are general trends, specific generational experiences highlight that your personal pace might vary. Knowing this helps you approach your search with a more informed and patient perspective. You can discover more insights about generational home buying trends to further inform your journey.

Ultimately, when you approach your home purchase armed with a clear understanding of these potential influences, you're setting yourself up for strategic planning and a much more positive experience. This foundational knowledge is what empowers you to navigate the home buying process timeline with greater confidence, helping you steer clear of common delays and significantly reduce any accompanying anxiety.

Smart Financial Preparation That Actually Works

- W-2 forms (past two years)

- Tax returns (past two years)

- Bank account statements (recent 2-3 months)

- Statements for any investment or retirement accounts

- Identification (driver's license, social security card)

Beyond paperwork, your credit score plays a huge role. This three-digit number is what lenders look at to gauge how reliable you are with credit and, crucially, what interest rates they'll offer you. Strive for the best score you can by consistently paying bills on time, keeping credit card balances low, and holding off on new credit until after you've bought your home.

Securing Your Buying Power

With your documents organized and your credit looking sharp, it's time for a real power move: mortgage pre-approval. This isn't just a rough guess; it's a lender's conditional promise for a specific loan amount, instantly making you a competitive buyer. It clearly shows sellers and agents you mean business and defines your buying power.

With 15% of Americans planning to purchase a home in the next 12 months in 2025, and looking to spend an average of $259,088, robust financial groundwork is more important than ever. Effective financial planning can truly pave the way for a smoother home buying experience amidst these conditions. Explore this topic further to get ahead.

Don't stop at just one loan quote! Investigating various loan options is key to finding the one that truly suits your financial picture. Whether it's a conventional loan, FHA, VA, or USDA loan, each type comes with its own set of rules and advantages for down payments and credit scores. Getting familiar with these choices early on can save you from unexpected hold-ups.

Avoiding Common Financial Pitfalls

You’re on the home stretch, so don't let common financial missteps throw a wrench in your home buying process timeline! Big credit purchases, like financing a new car, or switching jobs without a heads-up to your lender, can jeopardize your loan approval right when it matters most. These moves can shift your debt-to-income ratio, which lenders watch very closely.

It's also vital to budget for the full scope of homeownership. We're talking more than just the down payment and closing costs; think about property taxes, homeowners insurance, and those inevitable maintenance tasks. Want to make sure you’ve covered all bases? You might be interested in checking out these 5 Hidden Costs of Buying a Home. By tackling these financial details head-on, you're paving the way for a much more assured and rewarding home buying journey.

Strategic House Hunting That Gets Results

So, your finances are sorted, and that pre-approval letter is probably in your grasp. Now comes the exciting part: finding your dream home! But hold on, before you jump into endless online scrolling, understand that a clever approach here can significantly cut down your search time. Imagine shrinking months of looking into just a few productive weeks – it’s entirely possible.

To truly succeed and keep your home buying process timeline on track, you need more than casual browsing. It's about taking control of your search, making deliberate choices, and keeping the energy high to get those fantastic results.

Honing Your Must-Haves and Nice-to-Haves

Your first power move? Get crystal clear on your needs versus your wants. Seriously, before you peek at a single listing, sit down and make this vital distinction. Think of it this way: a top-rated school district might be a must-have, something you absolutely cannot compromise on. On the other hand, that chef’s kitchen with marble countertops? That could be a nice-to-have.

This upfront honesty is your secret weapon against wasted viewings and a dragging home buying process timeline. You’ll be laser-focused. Here’s a great starting point for that conversation with your agent:

- Location is Key: How close do you need to be to work, schools, your favorite coffee shop, or family? This often becomes a non-negotiable anchor for your search.

- The Right Fit (Size & Layout): Nail down the number of bedrooms and bathrooms essential for your comfort. Consider the overall square footage and if the flow of the home works for your daily life.

- Condition Check: Are you dreaming of a move-in ready haven, or does the idea of a fixer-upper excite you? Be truthful about your willingness and budget for renovations.

- Looking Ahead: Will this home still be a great fit for your plans in 5 to 10 years? Thinking long-term now saves headaches later.

Embracing these priorities realistically is what allows you and your real estate agent to zero in on the best properties. While the perfect "dream list" home is a unicorn, finding one that ticks all your essential boxes and many of your desires is absolutely achievable.

Making the Most of Your Support System and Technology

Think of your real estate agent as your indispensable guide on this journey. They bring a treasure trove of local market insights, access to the freshest listings through the Multiple Listing Service (MLS), and the sharp negotiation skills you'll need. To make this partnership truly shine, share your well-defined priorities openly and often.

And don't forget the power of technology! Dive into online search platforms and real estate apps like Zillow or Realtor.com. These resources offer fantastic tools: think stunning photo galleries, immersive virtual tours, and rich details about neighborhoods, from school ratings to local cafes. It’s no surprise that for many, property photos are the most useful online feature, offering a quick way to decide if a home is worth seeing in person.

Making Viewings Count

When it's time to see homes in person, a smart, organized plan will serve you well. Schedule viewings strategically – try clustering them by neighborhood to make the most of your time and energy. As you walk through, train your eye to see past the pretty staging. Focus on the core: what's the condition of the roof, the heating and cooling system, the windows, and any visible parts of the foundation?

Don't be shy about taking notes and snapping photos (if allowed, of course!). These become invaluable when you're trying to remember details and compare your options later. This methodical way of looking at homes helps you recognize quality properties more quickly. More importantly, it stops you from getting sidetracked by minor cosmetic issues that are easy fixes, while potentially missing bigger, costlier problems. Staying organized and focused means your house hunt remains an exciting adventure, not a draining marathon.

Crafting Winning Offers In Today's Market

You've found a promising property after diligent searching. Now, making an offer is a critical step. A strong offer is more than just price; it's a carefully crafted package to attract sellers while safeguarding you. Mastering this moves your home buying process timeline from viewings to contract talks.

To make your offer compelling, understanding the seller's motivations is key. Do they need a quick sale, the highest price, or a flexible closing or leaseback? Your agent can uncover these crucial clues, directly shaping your offer strategy and giving you an edge.

Key Components of a Standout Offer

Price is key, but sellers view the whole package. They assess your financing, the size of your earnest money deposit, and any contingencies. In hot markets, fewer contingencies are appealing, but understand the risks, like waiving an inspection.

Contingencies are offer clauses protecting you, the buyer. Common ones cover financing, appraisal, and inspection. An appraisal contingency, for example, lets you adjust or withdraw if the appraisal is low, without losing your deposit. Balancing protection and competitiveness is key.

Beyond finances, flexibility can make your offer shine. A closing date matching the seller's timeline is a big plus. Sometimes, a personal letter about why you love their home can create an emotional connection, making your offer more human and memorable.

The Negotiation Dance

Getting a counteroffer is normal in the home buying process timeline; it means negotiations are on! Your agent's guidance here is priceless. They'll help you assess each point objectively, so you can respond thoughtfully, not emotionally.

It's crucial to set your absolute walk-away price before negotiating. This clear limit gives you leverage and stops you from overpaying, especially with multiple offers. A successful purchase must also fit your long-term financial comfort.

Market conditions, especially mortgage rates, greatly influence your offer. Good news: rates are forecast to stabilize around 6% in 2025. This welcome stability, after recent volatility, could bring more buyers as homes become more accessible.

If rates dip below 6.5%, the income for a median-priced home might drop under $100,000. This could open doors for 6.2 million more households. Such a steadier market impacts how aggressive your offer needs to be. Explore this topic further for a deeper understanding of 2025 market predictions.

Strong loan terms are vital for a compelling offer. A lower interest rate boosts buying power and shows sellers your financial stability, making your offer more attractive. Get tips from our guide: How to Secure the Best Interest Rates for Your Housing Loan.

Ultimately, a winning offer is a complete package that meets seller needs while protecting your own. This smart approach is vital for navigating this key stage of your home purchase and confidently reaching the closing table.

Mastering Due Diligence Without Delays

So, your offer has been accepted – congratulations! Now, you’re stepping into the crucial due diligence period. Think of this part of the home buying process timeline as your golden opportunity. It’s your dedicated time to really dig in and examine the property thoroughly, turning what could be a nail-biting wait into a smart, proactive step to protect your major investment. This is where savvy buyers make sure the home is truly what it seems and keep the purchase moving smoothly.

The Critical Role of Home Inspections

One of the most powerful tools in your due diligence toolkit is the home inspection. You’ll want to get this on the calendar with a certified professional right away, ideally within 3-7 days after your offer is accepted. This isn't just a quick look-around; it’s a deep dive into the property's true condition, giving you the power to uncover potential problems before you're locked in.

Your inspector will meticulously check key areas, including:

- The foundation and overall structural soundness

- The roof’s current state and how much life it has left

- How well the HVAC (heating, ventilation, and air conditioning) system is working

- The safety and compliance of plumbing and electrical systems

Don't stop there if the property calls for it. Depending on its age, features, or location, you might also need specialized checks for things like radon, termites, or even a more in-depth HVAC assessment. Budgeting around $343 for a general inspection is a good starting point, but remember this figure can shift based on the home’s size, age, and where it's located, so factor that into your expenses for this phase.

Navigating Inspection Reports and Negotiations

Once that inspection report lands in your hands, it's decision time. This comprehensive document lays out everything the inspector found, from small, easy fixes to more serious issues that could give you pause. This information is your leverage to make smart choices about moving forward.

This report is also your ticket to the negotiating table. You can now make repair requests or ask the seller for credits to cover the cost of fixes. For instance, if the inspection uncovers an aging water heater on its last legs, you’re in a strong position to ask the seller to replace it or chip in for a new one. Understanding what's worth negotiating and what might be a genuine deal-breaker is absolutely vital to protect your investment and peace of mind.

Understanding the Home Appraisal Process

While you're focused on inspections, your lender will be setting up a home appraisal. This isn't for you directly, but it's a critical step: it's an unbiased evaluation of the property's fair market value. The lender needs this to ensure they aren’t lending more than the home is actually worth. An appraiser achieves this by looking at recent sales of comparable homes and assessing the property's current condition.

What if the appraisal comes in below your offer price? This can indeed throw a wrench in your home buying process timeline, but you have options. You could try to renegotiate a lower price with the seller, cover the difference yourself, or, if you wisely included an appraisal contingency in your offer, you can walk away from the deal without penalty. Keep in mind that an appraisal for a single-family home typically costs around $357.

To help you manage this critical phase effectively, here’s a breakdown of key inspection tasks, their typical timeframes, and what you should be thinking about at each stage. This "Home Inspection Timeline and Checklist" is designed to keep you organized and proactive, detailing key inspection tasks, typical timeframes, and decision points during the due diligence period.

Home Inspection Timeline and ChecklistKey inspection tasks, typical timeframes, and decision points during the due diligence period

By diligently working through this checklist, you're not just ticking boxes; you're empowering yourself to make a confident, well-informed purchase. Successfully managing these steps is your best path to a smooth closing and the keys to your new home, avoiding frustrating delays in your home buying process timeline.

Juggling all these elements—inspections, reports, appraisals, and negotiations—demands good organization to keep your closing day on the horizon. Constant, clear communication with your real estate agent, inspector, appraiser, and lender is your secret weapon. This teamwork ensures everyone is on the same page and all deadlines are met throughout the due diligence period, which typically lasts from 14 to 30 days. Master this, and you're well on your way to a successful purchase.

Closing Day Success And Final Preparations

You're on the home stretch of your home buying process timeline! These last few weeks are bustling with activity, and careful organization is your best friend. It's this final push that ensures you step smoothly into homeownership, because every single detail counts for a triumphant closing day.

Navigating the Final Hurdles

The champagne isn't quite ready to pop just yet; a few more vital steps pave the way in your home buying process timeline. Your lender is about to give the green light with the final loan approval, also known as the "clear to close." This is a huge moment, signaling they're prepared to fund your mortgage because all underwriting requirements are satisfied.

While that's happening, your closing attorney or title company is deep in title work. They're meticulously checking that the property's title is spotless – no unexpected claims or ownership squabbles – protecting your big investment. They'll also be the ones to schedule your closing day, making sure everyone's calendars align.

The Crucial Final Walkthrough

Don't skip the final walkthrough! This critical step, usually scheduled 24-48 hours before closing, isn't a repeat inspection. Instead, it’s your chance to confirm the home is exactly as you agreed in the purchase contract and all negotiated conditions are fulfilled.

Pay close attention during this visit. You'll want to ensure:

- Any negotiated repairs are finished to your satisfaction.

- All included appliances and fixtures (as outlined in your contract) are there and functioning correctly.

- The home meets the agreed-upon standard of cleanliness (like "broom clean," if that was the term).

- No new damage has appeared since your last thorough look or the inspection.

Spotting and addressing any issues now, no matter how minor, is key to preventing hiccups or holdups on the big day.

Preparing for the Closing Table

Getting ready for the closing table with care is your ticket to a smooth experience as you approach this major milestone in your home buying process timeline. A big piece of this puzzle is scrutinizing your Closing Disclosure (CD). You are legally entitled to receive this crucial document at least three business days before closing. It lays out all the final loan details, estimated monthly payments, and the various fees and closing costs you'll owe, so take the time to compare it line-by-line with your original Loan Estimate.

You'll also need to get your funds ready for closing costs and any outstanding down payment. Usually, this means a certified payment like a cashier's check or a confirmed wire transfer – your closing agent will give you the exact details. Keep in mind, these closing costs typically fall between 2% and 5% of the home's purchase price. Finally, don't let homeowners insurance slip your mind; you'll need to have a policy in place and show proof to your lender before they can officially release the loan funds. For a deeper dive into this final financial phase, you might find our article on Understanding Loan Closures: Tips to Navigate the Final Step in Your Mortgage Journey quite helpful.

What to Expect on Closing Day

Closing day means paperwork – quite a bit of it, actually! So, give yourself plenty of time and don't hesitate to ask questions about anything you're signing. Two of the most important documents will be the promissory note, which is your official IOU for the loan, and the deed of trust (or mortgage document), which uses the property as security for that loan. The closing agent, who is usually an attorney or someone from the title company, will walk you through everything, making sure you understand what each document means.

Once every signature is in place from all parties, and all the money has been confirmed and correctly distributed, that incredible moment you've diligently worked for throughout your home buying process timeline is finally here. You are officially a homeowner, and the keys to your new place are yours! Smart preparation turns this last hurdle from a potential stressor into a true reason to celebrate.

Key Takeaways For Home Buying Success

Mastering the home buying process timeline isn’t a matter of luck—it’s the result of clear expectations, thoughtful strategy, and decisive action. You're not just aiming to sign the final papers; you're aiming to do it smartly, safeguarding your financial health. Let this be your essential guide to making sound decisions at each important stage.

Your Roadmap to an Efficient Home Buying Timeline

Each stage of your home buying adventure sets the stage for the next. Grasping the vital elements for success in each phase can truly compress your overall home buying process timeline, getting you into your new home faster.

Build a Strong Base: Start by getting a crystal-clear picture of your finances and current market conditions. Taking steps like confirming your credit score—you'll want 620+ for conventional loans, or 580+ for an FHA loan with a 3.5% down payment—and securing a mortgage pre-approval gives you a solid budget and positions you as a buyer sellers take seriously.

Search Smarter, Not Harder: Pinpoint your absolute must-haves before you start looking. The typical house hunt can stretch for about 10 weeks, but a sharp, focused search, especially with a skilled agent by your side, can cut that time down considerably.

Make a Powerful Offer: A successful offer isn't just about the dollar amount. When you understand what sellers want and keep an eye on mortgage rates (projected to settle near 6% in 2025), your offer will stand out from the crowd.

Investigate Thoroughly: This crucial period, usually 14 to 30 days, is your best chance to find any hidden problems. Don't skip the home inspection (averaging $343) or the appraisal (around $357)—these are essential to protect your hard-earned money.

Seal the Deal Seamlessly: The home stretch demands careful focus on every detail. This means thoroughly checking your Closing Disclosure—which must arrive at least three business days before your closing date—and arranging your final walkthrough to ensure everything is perfect.

Staying on Track: Key Milestones and Checklists

Want to stay in control and keep things moving? Using clear milestones and practical checklists will keep you organized and driving forward on your home buying process timeline. This forward-thinking method means you're always ready for what's next.

Milestone: Financial Readiness Achieved

- Credit report reviewed and score understood.

- Detailed budget created, including potential mortgage payments and closing costs (typically 2-5% of purchase price).

- Mortgage pre-approval letter secured from a lender.

Milestone: Offer Accepted & Under Contract

- Earnest money and any due diligence fees submitted promptly.

- Home inspection scheduled (ideally within 3-7 days of contract).

- Lender formally notified to begin the mortgage application and appraisal process.

Milestone: "Clear to Close" Received

- Homeowners insurance policy secured.

- Final walkthrough completed (24-48 hours before closing).

- Closing Disclosure reviewed thoroughly for accuracy.

- Funds for closing prepared (cashier's check or wire transfer).

Avoiding Delays: Proactive Strategies for a Smooth Journey

Don't let common setbacks slow down your home buying process timeline. Many frustrating delays are entirely preventable if you plan ahead and act decisively.

Stay in Constant Contact: Keep the lines of communication wide open with your real estate agent, lender, and attorney. Responding swiftly when they need information is absolutely critical to keep things on schedule.

Get Your Paperwork Perfect: Gather all your financial documents—like W2s, pay stubs, and bank statements—and have them organized before you even think about making an offer. Lenders will ask for these quickly, and being unprepared can cause significant hold-ups to your closing.

Master Your Contingencies: Make sure you fully grasp all the contingencies in your offer, such as those for inspection, appraisal, or financing, and be very clear on their deadlines. Overlooking these can put your earnest money at risk, or even cause the entire deal to fall through.

Keep Your Finances Stable: Once you're in the mortgage process, resist the urge to make big purchases, apply for new credit, or switch jobs. Any of these moves can alter your debt-to-income ratio and could jeopardize your final loan approval, so play it safe!

When you concentrate on these vital aspects—grasping each step, monitoring your progress, and tackling potential hurdles head-on—the home buying process timeline changes from a daunting challenge into an organized and thrilling journey to owning your new home.

Are you prepared to take control of your home buying process timeline with confidence? At Tiger Loans Inc., we offer the deep knowledge and essential tools to support you at every turn, from fast pre-approvals right through to a hassle-free closing. Start your journey with Tiger Loans today!

Alex Chen

Alex Chen

Get in touch with a loan officer

Our dedicated loan officers are here to guide you through every step of the home buying process, ensuring you find the perfect mortgage solution tailored to your needs.

Options

Exercising Options

Selling

Quarterly estimates

Loans

New home

Stay always updated on insightful articles and guides.

Every Monday, you'll get an article or a guide that will help you be more present, focused and productive in your work and personal life.

.png)

.png)

.png)

.avif)

.avif)

.avif)

.png)

.png)

.png)

.avif)

.png)

.png)

.avif)

.png)

.avif)

.png)

.avif)

.avif)