How Does Reverse Mortgage Work? Complete Homeowner's Guide

November 19, 2025

Learn how does reverse mortgage work, including eligibility, payment options, and pros and cons. Find out if a reverse mortgage is right for you.

So, you’ve heard about reverse mortgages, but what are they, really? Let’s break it down in simple terms.

Think of the equity you've built in your home over the years as a locked savings account. You’ve diligently made payments, and the value has grown. A reverse mortgage is essentially the key that unlocks that account, letting you access the cash you've built up without having to sell your house.

How a Reverse Mortgage Really Works

This is where things get interesting and flip the script on everything you know about home loans. With a traditional mortgage, you pay the bank every month to build equity. With a reverse mortgage, the bank pays you from the equity you already have.

It’s a fundamental shift in how the money flows. Your loan balance actually goes up over time instead of down. Why? Because the cash you receive, plus any interest and fees, gets added to what you owe.

The Bottom Line: A reverse mortgage turns the traditional loan model on its head. Instead of you paying the lender, the lender pays you. You stop making monthly mortgage payments, and the loan is typically paid back only when you sell the home or it's no longer your main residence.

This unique structure can be a game-changer for older homeowners looking for extra income. To see what might work for you, it's a good idea to explore the different types of reverse mortgage loans available.

Understanding the Growing Loan Balance

So, how exactly does the amount you owe increase? It's pretty straightforward. Each month, two things get added to your loan balance:

- The Cash You Take Out: This includes any money you receive, whether it’s a one-time lump sum, regular monthly payments, or funds you draw from a line of credit.

- Interest and Fees: Just like any loan, interest accrues. These charges, along with any mortgage insurance premiums, are tacked onto your balance.

Since you're not making monthly payments to chip away at these costs, the total amount owed creeps up over time. This continues until the loan comes due, which usually happens when you sell the home, move out for more than 12 months, or pass away.

The loan is specifically designed for homeowners aged 62 and older and is structured to be repaid from the proceeds of the home's sale. This built-in protection means you and your heirs won't be on the hook for a loan that ends up being worth more than the home itself.

To clarify this even further, let’s compare a reverse mortgage side-by-side with a traditional home loan you're likely more familiar with.

Reverse Mortgage vs. Traditional Mortgage At a Glance

FeatureReverse MortgageTraditional MortgageWho Gets Paid?The lender pays you (the homeowner).You (the homeowner) pay the lender.Monthly Payments?No required monthly mortgage payments.Required monthly principal and interest payments.Loan Balance Over TimeIncreases.Decreases.Home Equity Over TimeDecreases as you draw funds.Increases as you pay down the loan.When is it Repaid?When the borrower sells the home, moves out permanently, or passes away.Over a set term (e.g., 15 or 30 years) through monthly payments.Primary PurposeTo access home equity for supplemental income in retirement.To purchase a home.

As you can see, they are truly opposite financial tools, each designed for a completely different stage of life and financial goal.

Discovering If You Are Eligible for a Reverse Mortgage

Thinking about a reverse mortgage? The good news is that qualifying isn't about having a stellar credit score or a high-paying job. The rules are built around things you likely already have: your age and the value of your home. It's a structure designed to help, not hinder, retirees who want to tap into their home's equity.

It helps to think of the eligibility criteria not as roadblocks, but as guardrails. They exist to make sure a reverse mortgage is a genuinely good and sustainable fit for your financial future. Let's walk through what lenders are looking for.

The Two Cornerstones: Age and Equity

At its heart, qualifying for a reverse mortgage comes down to two simple things: how old you are and how much of your home you actually own. These two factors are the foundation for everything else, determining not just if you can get one, but how much you might receive.

- Age: The magic number is 62. You (and any co-borrowers on the title) must be at least 62 years old. This is the standard for the most common and federally-insured option, the Home Equity Conversion Mortgage (HECM).

- Home Equity: You need to own your home outright or have a substantial amount of equity in it. There isn't a hard-and-fast rule, but a good benchmark is having at least 50% equity. If you still have a mortgage, the first thing your reverse mortgage will do is pay that off completely.

The focus on homeowners over 62 with significant equity really defines who uses this tool. Industry data shows the average borrower is in their late 60s or early 70s with a home valued well into the six figures. You can dig deeper into the reverse mortgage market trends at DataInsightsMarket.com to see how things are evolving.

Your Property and Financial Responsibilities

Beyond your age and equity, the home itself has to meet certain criteria. Lenders also need to be sure you can handle the ongoing financial responsibilities that come with homeownership.

First, the house must be your primary residence—the place you live most of the year. Not all properties are eligible, but most common types are, including:

- Single-family homes

- Homes in 2-4 unit properties (as long as you live in one of the units)

- Approved condominiums and townhomes

- Some manufactured homes that meet specific FHA standards

Lenders will also perform a financial assessment. This isn't like a typical loan application where they check if you can make monthly payments. Instead, they're simply confirming you have the financial means to cover future property taxes, homeowners insurance, and basic maintenance. It’s a crucial check to ensure you can comfortably afford to stay in your home for the long haul.

The Mandatory Counseling Session: Your Personal Guide

Before you can even fill out an application, there's one step you absolutely cannot skip: a counseling session with a government-approved, independent reverse mortgage counselor. This isn't just a box to check; it’s one of the most valuable parts of the process.

This session is 100% for your benefit. The counselor is your advocate, there to make sure you understand every detail—the costs, the benefits, and the potential downsides. They’ll look at your finances, discuss other options you might have, and answer all your questions. Think of it as your own private workshop, designed to give you the confidence and clarity you need to decide if a reverse mortgage is truly right for you.

The Reverse Mortgage Application: A Step-by-Step Walkthrough

Getting a reverse mortgage isn't a race to the finish line. Think of it more like a deliberate, guided process with built-in checkpoints, all designed to make sure you're comfortable and fully informed before making any big decisions. It’s a journey that actually starts with education, not paperwork.

This careful, step-by-step approach puts you in control, ensuring you grasp exactly how this financial tool would work for you and your unique circumstances.

Your First Step: The Counseling Session

Before any lender can even look at your application, federal law requires you to complete a counseling session. This isn't just a box to tick; it's a mandatory and incredibly valuable part of the process for a Home Equity Conversion Mortgage (HECM), which is the most common kind of reverse mortgage.

You’ll connect with an independent, HUD-approved counselor who works for you, not the lender. Their job is to be your advocate. They'll go over your finances, clearly explain what the loan means for your future, and even talk through other options you might not have considered. This is your dedicated time to ask absolutely anything in a completely neutral, no-pressure setting.

The whole point of this session is to empower you. It’s set up to give you a clear, unbiased picture of how a reverse mortgage works—including the costs and your responsibilities—so you can move forward with total confidence.

The Application and Documentation Phase

With your counseling certificate in hand, you're ready to formally apply. Now you’ll work directly with your lender to pull together the required documents. It’s a fairly straightforward process aimed at confirming who you are and the details of your property.

Here's what you'll generally need to gather:

- Proof of Age: Your driver’s license, passport, or birth certificate to show you meet the 62+ age minimum.

- Property Ownership Documents: The title or deed to your home, along with recent property tax statements.

- Existing Mortgage Information: If you still have a mortgage, you'll need the most recent statement showing the balance.

- Counseling Certificate: The official document you received from your HUD-approved counseling session.

Appraisal and Underwriting

Once your application is submitted, the lender will arrange for a home appraisal by an FHA-approved professional. This is a crucial step. The amount of money you can access is calculated based on a combination of your home's current market value, your age, and the interest rates at that time. The appraiser will evaluate your home's condition and compare it to similar properties that have recently sold in your neighborhood.

At the same time, your application goes into underwriting. This is where a specialist double-checks all your documentation, runs a financial assessment to ensure you can handle the ongoing obligations (like taxes and insurance), and makes sure every federal guideline has been met. It’s the final review before your loan gets the green light.

Closing and Receiving Your Funds

The last stage is closing. You’ll sign the final loan papers, much like you did when you first bought your home. But the next step is what really sets this process apart. After a mandatory three-day "right of rescission" period—which gives you a window to change your mind and cancel the loan for any reason—the funds are officially yours.

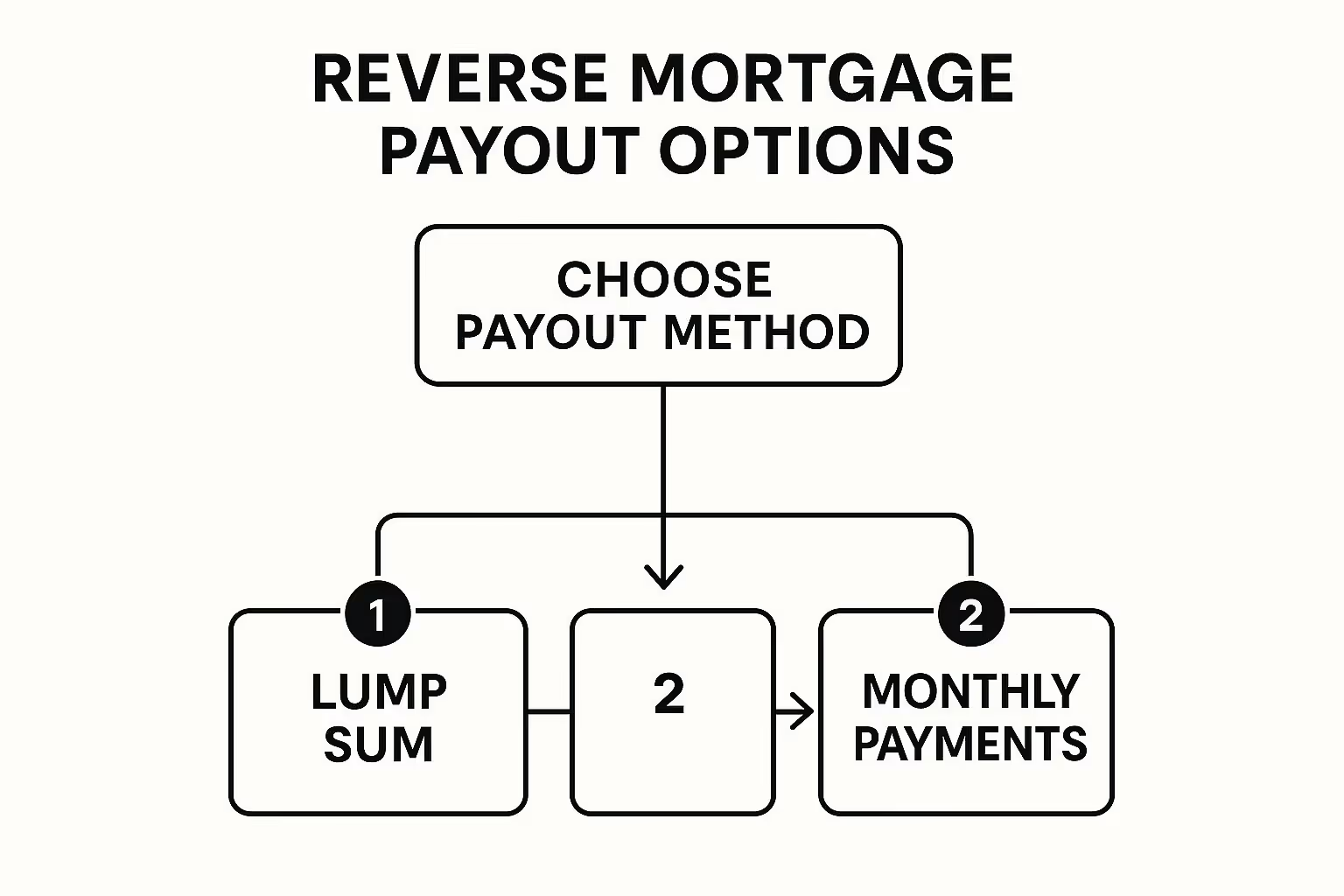

This is the moment you put your chosen payout plan into action. The infographic below illustrates the different ways you can choose to receive the money.

As you can see, you have a lot of flexibility in how you access your equity, which allows you to tailor the payments to fit your specific financial needs and goals.

Choosing the Right Payout Plan for Your Lifestyle

This is where a reverse mortgage stops being a concept and starts becoming your personal financial tool. Picking how you get your money isn’t a small detail—it’s the most important decision you'll make in the process. It's all about matching the flow of cash to your real-world needs and long-term vision for retirement.

Think of your home equity as a reservoir you've spent years filling. Now you get to decide how to open the tap. Do you need one big gush of water for a major project? Or would you prefer a steady, predictable stream to supplement your monthly budget? Maybe you just want a flexible spigot you can turn on and off as life happens.

Let's break down the options.

The Lump Sum Distribution

The lump sum is exactly what it sounds like. You get all the available cash from your reverse mortgage in one big check right after closing. It's straightforward and built for immediate, significant financial goals.

For example, I've seen homeowners use a lump sum to completely pay off their old mortgage and lift the weight of monthly payments off their shoulders for good. Others use it to wipe out high-interest credit card debt or finally pay for a major home renovation that makes aging in place a reality.

The crucial thing to understand here is that interest starts building on the entire loan amount from day one. This makes the lump sum best suited for people who have a clear, one-time need for the funds.

Monthly Payments for Predictable Income

If your main goal is to create a more reliable monthly cash flow, then opting for regular payments is a fantastic choice. This plan gives you a consistent check you can count on, month after month, which makes budgeting for regular living expenses so much easier.

You generally have two ways to structure this:

- Tenure Payments: You receive a fixed monthly payment for as long as you live in the home as your primary residence. This offers incredible peace of mind because you know that stream of income won't run dry.

- Term Payments: You get fixed monthly payments, but only for a specific number of years that you choose upfront. This can be a great bridge if you know you have a temporary income gap to fill.

This approach feels a lot like getting a pension or a steady paycheck, effectively turning your home equity into a dependable source of income.

A reverse mortgage's power is in its adaptability. Choosing between a lump sum for immediate needs or monthly payments for ongoing stability is the core decision that aligns the loan with your life.

The Flexible Line of Credit

The line of credit is easily the most popular choice, and for good reason. It works a bit like a Home Equity Line of Credit (HELOC), but with one game-changing difference: you don't have to make monthly payments on the money you use.

With this plan, you're approved for a certain amount of credit, but you only pull out money as you need it. The biggest advantage? You only pay interest on the funds you actually withdraw, not the total amount you're approved for. This makes it a perfect financial safety net for those "what if" moments in life—unexpected medical bills, a new roof, or helping a grandchild.

Here's another unique perk: the unused portion of your credit line actually grows over time. That means you could have access to even more money down the road. When weighing your options, the interest rate structure is also a key factor; you can get a better handle on this by understanding the differences between adjustable-rate and fixed-rate mortgages. It’s this combination of control and security that makes the line of credit such a powerful tool.

Weighing the Benefits and Risks of a Reverse Mortgage

Any major financial decision requires looking at the full picture—the good, the bad, and everything in between. A reverse mortgage is no different. For many, it's a powerful tool that unlocks financial freedom in retirement, but it's absolutely essential to understand both sides of the coin before deciding if it's the right move for you. An honest look at the benefits and potential risks is how you make a choice with confidence.

Let's start with the advantages, which are usually what gets homeowners interested in the first place.

The Upside of a Reverse Mortgage

The most immediate and impactful benefit? No more monthly mortgage payments. For anyone who has spent decades sending checks to a lender, this alone can feel like a massive weight has been lifted. It can instantly free up hundreds or even thousands of dollars in your monthly budget.

Another huge plus is the ability to stay right where you are. You've built a life within those walls, surrounded by memories and a community you know and love. A reverse mortgage can provide the financial means to age in place comfortably, without being forced to sell a cherished home just to access its value.

On top of that, the funds you receive are generally tax-free. Whether you opt for a lump sum, monthly payments, or a line of credit, the money is considered a loan advance, not income. This means it typically won't mess with your Social Security or Medicare benefits.

Perhaps one of the most reassuring features is the non-recourse clause. This is a critical protection built into FHA-insured loans. It guarantees that you or your heirs will never owe more than the home's appraised value when the loan is repaid. Even if the loan balance balloons to more than what the home is worth, FHA insurance covers the difference.

The Downside and Potential Risks

Now for the other side of the equation. Just as there are compelling benefits, there are significant risks and costs you absolutely must consider.

The most obvious drawback is that a reverse mortgage isn't free—not by a long shot. You'll run into some pretty substantial upfront costs.

Summary of Potential Costs in a Reverse Mortgage

To give you a clearer picture, let's break down the common fees you're likely to encounter. These costs are often rolled into the loan balance, but it's vital to know what they are.

Cost ComponentTypical Range or DescriptionWhen It's PaidOrigination FeeCapped at $6,000. Calculated based on your home's value.Upfront (usually financed)Mortgage Insurance Premium (MIP)2% of the home's value upfront, plus 0.5% annually on the loan balance.Upfront and ongoingThird-Party Closing CostsVaries. Includes appraisal, title search, recording fees, etc.Upfront (usually financed)Servicing FeeCan be up to $35 per month.Ongoing (added to loan balance)InterestAccrues on the loan balance, including financed fees.Ongoing (added to loan balance)

Seeing these costs laid out makes it clear that while you aren't writing a check each month, the loan's cost is very real and grows over time.

This leads us to the next major point: the growing loan balance and diminishing equity. Since you aren't making payments, the interest and fees just keep piling up. Over time, the amount you owe increases, which means the equity you hold in your home shrinks.

This has a direct impact on what you can leave to your heirs. The more equity you use, the less will be left for your family. While your heirs can choose to repay the loan and keep the home, they'll only get what's left after the full loan balance is settled.

Finally, the loan becomes due and payable when a "maturity event" occurs. This is triggered if you sell the home, pass away, or move out for more than 12 consecutive months. That last point is critical—especially for anyone who might need to move into a long-term care facility. The loan has to be repaid, which usually means the home must be sold.

If you're curious how this stacks up against other ways to tap into your home's value, our guide on understanding your monthly home equity loan payments offers a helpful comparison. By carefully balancing these pros and cons, you can get a sense of how a reverse mortgage works not just on paper, but how it would actually play out in your life.

Understanding When the Loan Becomes Due

One of the biggest questions I hear from homeowners is, "So, when does all this money actually have to be paid back?" It's a natural concern. People worry about their family being suddenly saddled with a massive bill.

The good news is that a reverse mortgage isn't like a traditional home loan with a ticking clock and a fixed end date. Instead, the loan is designed to come due only when a specific life event happens. This structure is what allows you to stay in your home without the monthly stress of a mortgage payment.

Let's pull back the curtain and look at exactly what these triggers are.

The Three Triggers for Loan Repayment

Think of these as the three main "maturity events" that cause the loan balance to come due. Knowing these upfront helps you and your family plan for the future with confidence.

- You Sell or Transfer the Home's Title: If you decide it's time to sell and move, the reverse mortgage gets paid off from the sale proceeds. Simple as that. Whatever money is left over after the loan is settled is yours to keep.

- The Last Borrower Moves Out for Good: Your home must be your primary residence. If you, as the last remaining borrower, move out for more than 12 consecutive months—say, into an assisted living facility or with a relative—the loan will need to be repaid.

- The Last Borrower Passes Away: When the final borrower on the loan dies, the loan balance is due. This is when your heirs or your estate will step in to settle the account.

These triggers are clearly defined in your loan agreement, so there are no last-minute surprises.

What This Means for Your Heirs and Estate

When the loan does come due, your heirs are given clear instructions and a reasonable timeframe to handle things—usually up to six months, with potential extensions. Most importantly, they are never personally on the hook for the debt.

The key to this protection is a feature called the non-recourse clause.

This is a powerful, built-in safeguard on FHA-insured reverse mortgages. It guarantees that you or your heirs will never owe more than the home is worth at the time it's sold. If the housing market dips and your loan balance is higher than the home's value, the FHA insurance fund covers the shortfall. Not you, not your family.

This leaves your heirs with two straightforward choices:

- Pay Off the Loan and Keep the Home: They can decide the home is a keeper. By refinancing the debt or using other funds, they can pay off the reverse mortgage balance and keep the property in the family.

- Sell the Home to Settle the Loan: This is the more common path. They sell the property, and the proceeds are used to pay back the loan. Any equity left over goes straight to your heirs or the estate.

This process is designed to protect your legacy. For veterans and their families exploring different financing paths, understanding these end-of-life-cycle terms is essential. To see how these terms compare with other government-backed programs, you can learn more about how VA loans work on TigerLoans.com. Ultimately, a reverse mortgage is structured to give you financial breathing room while keeping your family's financial future secure.

Answering Your Biggest Reverse Mortgage Questions

Even when you grasp the basics, a few important questions always seem to pop up. These are the personal "what if" scenarios that can make anyone pause. Getting straight answers is the final piece of the puzzle to understanding if a reverse mortgage truly fits into your life.

Let's tackle these common concerns head-on and clear up any confusion.

Will the Bank Take My Home?

This is, without a doubt, the number one fear people have, and the answer is a firm no. You absolutely keep the title and ownership of your home, just like you would with any standard mortgage. The lender simply places a lien on the property, but it remains yours.

Your end of the bargain is to keep up with property taxes, maintain homeowners insurance, and generally take care of the house. As long as you meet these responsibilities, you can stay in your home for as long as you wish.

What Happens If My Home's Value Drops and I Owe More Than It’s Worth?

This is where one of the most powerful safeguards of an FHA-insured reverse mortgage kicks in: it's a non-recourse loan. This is a fancy way of saying you and your family are protected if the housing market takes a dive and your loan balance ends up higher than what your home is worth.

When it comes time to sell the home and repay the loan, the FHA's insurance fund covers any shortfall. This is a critical guarantee: you or your estate will never owe more than the home's sale price. It’s a huge source of peace of mind.

How Does This Affect My Heirs?

When you pass away or move out, your heirs are left with options, not obligations. They can choose to pay off the reverse mortgage balance and keep the home in the family—often by selling it or refinancing with a traditional mortgage.

Alternatively, they can simply sell the property. After the reverse mortgage is paid off from the proceeds, any leftover money—the remaining equity—belongs entirely to them.

Will a Reverse Mortgage Affect My Social Security or Medicare?

For most people, the answer is no. The funds you receive from a reverse mortgage are treated as loan proceeds, not as income. Because of this, it shouldn't have any impact on your Social Security or Medicare benefits.

A word of caution, though: if you receive needs-based assistance like Medicaid or Supplemental Security Income (SSI), it’s a smart move to talk with a financial advisor. Having a large sum of cash in your bank account could potentially affect your eligibility for those specific programs.

Ready to explore your options with a team that puts you first? The experts at Tiger Loans Inc can provide a clear, no-obligation assessment to see if a reverse mortgage is the right fit for your financial goals. Start your journey with us today!

Alex Chen

Alex Chen

Get in touch with a loan officer

Our dedicated loan officers are here to guide you through every step of the home buying process, ensuring you find the perfect mortgage solution tailored to your needs.

Options

Exercising Options

Selling

Quarterly estimates

Loans

New home

Stay always updated on insightful articles and guides.

Every Monday, you'll get an article or a guide that will help you be more present, focused and productive in your work and personal life.

.png)

.png)

.png)

.avif)

.avif)

.avif)

.png)

.png)

.png)

.avif)

.png)

.png)

.avif)

.png)

.avif)

.png)

.avif)

.avif)