Using a Refinance Breakeven Calculator

November 19, 2025

Is refinancing worth it? Use our refinance breakeven calculator to see when you'll start saving and make a smarter financial decision on your mortgage.

So, you're thinking about refinancing your mortgage. It's a big decision, and the shiny new, lower interest rate can be tempting. But before you jump in, there's one critical question you absolutely have to answer: will it actually save you money?

This is where a refinance breakeven calculator becomes your best friend. Forget the sales pitches and complex loan documents for a moment. This simple tool boils everything down to one number: the exact month you’ll start seeing real savings after paying off all the upfront closing costs.

How a Breakeven Calculator Works for You

The whole point of refinancing is to lower your monthly payment. But it’s not free—you’ll have closing costs, just like when you first bought your home. The breakeven calculator helps you see if you'll stay in the house long enough for the monthly savings to eventually overcome those initial fees.

Think of it like this: if your closing costs are $4,000 and your new, refinanced mortgage saves you $150 every month, you just divide the costs by the savings. In this case, it would take you a little over 26 months to "break even." After that, every single dollar you save is pure profit in your pocket.

My Pro Tip: If there's even a small chance you'll sell your home before hitting that breakeven point, refinancing will end up costing you money. It's a hard and fast rule that I always tell my clients to consider first.

To give you a clearer picture, let's look at a few different scenarios. The relationship between your closing costs and monthly savings directly determines how quickly—or slowly—you'll get your money back.

Breakeven Point Scenarios at a Glance

This table illustrates how different closing costs and monthly savings impact the time it takes to reach your breakeven point.

Total Closing CostsMonthly SavingsMonths to Break Even$3,000$10030$5,000$15033.3$4,000$25016$6,000$12548

As you can see, higher savings or lower costs can dramatically shorten your payback period. A lower monthly savings rate combined with high closing costs, like in the last example, means you're committing to staying in your home for at least four years to make the refinance worthwhile.

Remember, smart financial planning goes beyond just your mortgage. Many homeowners find extra cash flow by focusing on saving money on household utilities and making other small adjustments.

Ultimately, the breakeven calculation gives you a clear, personalized timeline. If you're also exploring other ways to use your home equity, be sure to weigh all your options. Our guide on https://www.tigerloans.com/post/refinance-vs-home-equity-loan-which-is-right-for-your-financial-goals can help you decide which path best fits your financial goals.

Getting Your Loan Details in Order

Before you can get a truly useful answer from any refinance breakeven calculator, you have to feed it the right information. Let's be honest, guessing at numbers or using vague estimates won't get you very far. To do this right, you need to track down a few key details from your current loan and the new one you're eyeing.

First, let's look at what you're paying right now. Grab your most recent mortgage statement—nearly everything you need is on that one piece of paper.

- Current Loan Balance: Find the total amount you still owe. This is your starting point.

- Current Interest Rate: Look for your current APR. This number dictates how much interest you're currently paying.

- Monthly Payment (P&I): This one is important. You need the principal and interest portion of your payment only. Don't include the amount you pay for property taxes or homeowner's insurance (escrow), as those will continue regardless of your loan.

With these numbers, you have a clear picture of your existing mortgage. This is the baseline we'll use to see if refinancing actually makes sense.

Finding Realistic New Loan Numbers

Now for the other side of the equation: the new loan. This is where a lot of people get tripped up. They see a rock-bottom rate advertised online and plug it into a calculator, but that's not how it works. You need real numbers based on your specific financial situation.

The only way to get these is to talk to a few lenders and get a real quote, often called a Loan Estimate.

A lender's quote is your crystal ball. It will show you the new interest rate you actually qualify for and give you an itemized list of closing costs. These costs—which can range from 2% to 6% of your new loan amount—are the biggest factor in your breakeven point.

To get a legitimate quote, you'll need to share your credit score and some basic income info. Don't just stop at the first lender you talk to! I always advise clients to get quotes from at least three different lenders to make sure they're getting a competitive deal.

Finally, you need a good-faith estimate of your home's value. While the lender will eventually order a formal appraisal, you can get a solid starting number by checking recent sales of comparable homes in your area or using a reputable online estimator.

Once you have all this information gathered, you're ready to get a breakeven analysis that you can actually count on.

Making the Refinance Breakeven Calculator Work for You

Alright, you've gathered all your loan documents and numbers. Now for the fun part: plugging them into the refinance breakeven calculator to see if a refi actually makes sense for you. It might look like a lot of boxes to fill in, but think of it as a simple machine that turns your financial data into a clear, easy-to-understand timeline.

At its heart, the calculator does one simple thing. It takes the total cost to get your new loan (the closing costs) and divides that by how much you'll save each month. The answer it spits out is your "breakeven point"—the exact number of months it'll take for the refinance to pay for itself. After that, it's all pure savings.

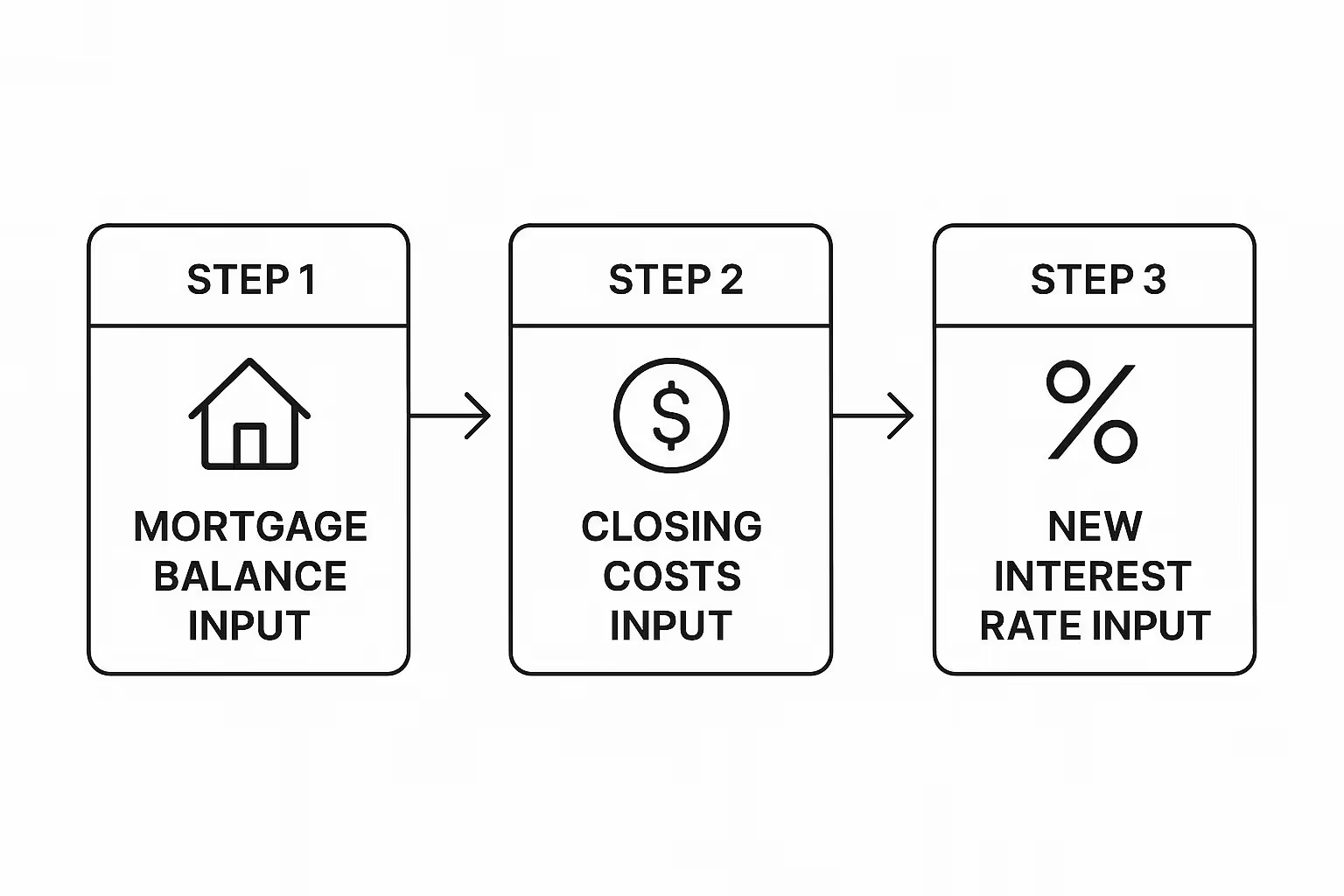

To get a reliable result, you just need to focus on three key pieces of information.

As you can see, the quality of your calculation depends entirely on the accuracy of these numbers. Garbage in, garbage out, as they say.

Decoding Your Closing Costs

For most homeowners I've worked with, the long list of closing costs on the Loan Estimate form is the most confusing part. These fees can add up quickly, typically falling between 2% and 6% of your total loan amount. Let's break down a few of the big ones you'll definitely see:

- Loan Origination Fee: This is the lender's fee for the work of preparing and processing your loan application. It's often around 1% of the loan value.

- Appraisal Fee: Before lending you a huge chunk of money, the lender needs to confirm your home is worth what you say it is. You'll pay for an independent appraiser to do this.

- Title Insurance: A necessary protection for both you and the lender. This policy guards against any old claims or liens on your property's title from popping up down the road.

Never just glance at these fees and accept them. I always tell my clients to ask essential questions before refinancing to make sure they know exactly what they’re paying for.

The real magic of the breakeven calculator isn't just getting one number; it's the power to play "what if." Don't stop at one calculation. What happens if you can lock in a rate that's a quarter-point lower? What if you negotiate $1,000 off your closing costs?

Let’s run a quick scenario. Say the calculator tells you it'll take 30 months to break even. But then you successfully negotiate a lower origination fee, which cuts $1,500 from your closing costs. If your monthly savings are $200, that one phone call just shortened your breakeven point by more than seven months.

This is how you go from just crunching numbers to making savvy financial moves that put real money back in your pocket.

So, What Do Your Breakeven Results Actually Mean?

The refinance calculator just handed you a number. This is your breakeven point, and it’s the heart of your decision. But that number, whether it's 18 months or 48 months, is just a piece of the puzzle. To see the full picture, you have to connect it to your own life.

Think about it. A breakeven point of 21 months seems like a no-brainer, right? But what if you’ve been eyeing a job in another state and might sell the house in a year and a half? In that case, refinancing would actually cost you money.

On the other hand, a longer breakeven of 40 months could be a brilliant move if you’ve just planted roots in your forever home. The calculator handles the math; you have to supply the real-world context. Your timeline is everything.

Look Past the Immediate Monthly Win

It's tempting to focus solely on that shiny new, lower monthly payment. I get it—seeing that number drop feels like an instant victory. But you have to resist that temptation and look deeper at the total interest paid over the life of the new loan. This is especially critical if you’re stretching out your loan term again.

Let’s say you’re 12 years into your current 30-year mortgage, leaving you with 18 years of payments. If you refinance into a brand-new 30-year loan, your payment will almost certainly be lower. But you've just reset the clock and added 12 extra years of interest payments.

Always ask your lender for amortization schedules for both loans. Seeing the total interest figures side-by-side can be a real eye-opener.

The goal isn't just to win the monthly payment battle; it's to win the long-term financial war. A successful refinance should improve your overall net worth, not just your short-term cash flow.

This trade-off has always been at the core of the refinance decision. I've seen homeowners save a fortune by making a smart move here. For example:

- Scenario: You move from a 30-year loan at 5% APR to a 15-year term at 3.25% APR.

- Upfront Cost: Let's say closing costs are $6,000.

- The Payoff: You could save over $63,000 in total interest.

In this case, you'd hit your breakeven point in about 21 months and start building equity at a much faster clip. You can play with different numbers and discover more insights about mortgage calculations to see how these variables interact.

When you weigh your breakeven point against your life plans and the total interest cost, you're no longer just looking at calculator results. You're building a confident, smart financial strategy.

Common Refinancing Mistakes to Avoid

It’s so easy to get fixated on a lower monthly payment. When you see that number drop, it feels like an instant win. But I’ve seen this become one of the biggest traps in refinancing time and time again.

A truly successful refinance isn't just about freeing up cash flow this month; it’s about improving your financial position for the long haul. Focusing only on that monthly payment can easily hide some serious long-term costs that come back to bite you.

Resetting the Clock on Your Loan

One of the costliest mistakes is extending your loan term without a good reason. Let’s say you’re 15 years into a 30-year mortgage. If you refinance into a new 30-year loan, your payment will almost definitely be lower. But think about what just happened—you’ve reset the clock and tacked on an extra 15 years of interest payments. You could end up paying tens of thousands more than if you’d just stayed the course.

Overlooking the Real Costs of the Deal

Another classic misstep is glossing over the upfront expenses. Closing costs aren't trivial; they typically run anywhere from 2% to 6% of your new loan amount. It’s crucial to account for every single fee, from the appraisal and origination fees to title insurance. Miss these, and your breakeven calculation will be completely off.

This is exactly why a refinance breakeven calculator is so valuable. We’ve seen huge swings in interest rates over the years. Think back to the period from 2007 to 2015, when average rates fell from 6.34% to 3.8%. Those drops made refinancing a no-brainer for many, but you need to be sure the math works for you today, especially with average closing costs hovering around $3,860.

A refinance that looks good on the surface but costs you more in total interest is a bad deal, period. Always compare the total interest you'll pay on the new loan against what you would have paid on the old one.

Finally, don't forget the other details. Will your new loan trigger Private Mortgage Insurance (PMI)? If refinancing pushes your loan-to-value ratio above 80%, you could get hit with a new PMI payment that wipes out your savings.

Remember, refinancing is just one tool in your toolbox. It’s very different from a home equity loan, and it’s important to understand which is the right fit. If you're weighing your options, our guide on a home equity loan vs. a refinance can help you make a smarter decision.

More Than Just a Number: Thinking Beyond the Breakeven Point

So, you've plugged your numbers into a refinance breakeven calculator and have your magic number—the exact month you’ll start saving money. That’s a fantastic starting point, but it's just that: a start. Making a truly savvy refinancing decision means looking at the entire chessboard, not just the next move.

Think of it this way: your breakeven point is the quantitative answer, but the qualitative side of the equation is just as important. For example, you’ll almost certainly run into offers for a "no-cost" refinance. It sounds tempting, right? No out-of-pocket closing costs. But lenders aren’t just giving away free money; they typically build those fees into a slightly higher interest rate. The real question is whether paying those costs upfront for a rock-bottom rate will save you more in the long run. Your breakeven analysis needs to account for both scenarios to see which one truly comes out ahead.

Tapping Into Your Home's Potential

Sometimes, the goal of refinancing isn't just about snagging a lower monthly payment. For many homeowners, it's a strategic move to unlock the wealth they've built in their homes. This is where a cash-out refinance enters the picture. It lets you borrow more than you currently owe and walk away with the difference in cash.

What do people do with that money? The possibilities are huge.

- Smart Home Improvements: Funding that kitchen remodel or adding a new bathroom can significantly boost your property's value.

- Debt Consolidation: Rolling high-interest credit card or personal loan debt into your new, lower-rate mortgage can free up hundreds in cash flow each month.

- Life's Big Expenses: Using your home's equity can be a smarter way to pay for things like college tuition or unexpected medical bills.

A cash-out refinance isn't a simple mortgage swap; it's a wealth management tool. The calculation is no longer just about recouping closing costs. You're now weighing the cost of that new, larger loan against the long-term financial benefit of the cash you’re pulling out.

This is a powerful strategy, but it requires serious consideration. You are increasing your total mortgage debt and reducing your home equity. The key is to ensure this move aligns with your long-term financial health, not just your immediate cash needs.

Still on the Fence? Let's Tackle Those Lingering Refi Questions

Running the numbers is a huge first step, but it’s completely normal to have some questions still bouncing around in your head. Let's walk through some of the most common "what-ifs" I hear from homeowners, so you can move forward with total confidence.

What if I Have to Sell Before I Break Even?

This is the single most important question to ask yourself. If you sell your home before hitting that breakeven date, the refinance will have been a net loss. You’ll have paid all those closing costs without sticking around long enough for the monthly savings to pay you back.

That's precisely why it's so critical to be honest about your future plans. Your breakeven timeline must align with how long you genuinely expect to stay in the home.

Are "No-Closing-Cost" Refinances Actually a Good Deal?

There's no such thing as a free lunch, especially in the mortgage world. A "no-closing-cost" refinance isn't truly free; the lender is simply rolling those costs into your loan in a different way.

Typically, this means you'll be offered a slightly higher interest rate. So, while you avoid paying cash out-of-pocket, you end up paying more in interest over the long haul.

It's always a trade-off. You're choosing between paying more now (closing costs) for a lower rate or paying nothing upfront for a higher rate over time. Always calculate both scenarios.

Is It Worth Refinancing for Just a Small Rate Drop?

It absolutely can be. Don't underestimate the power of a small percentage point over the life of a mortgage. A seemingly minor drop of just 0.5% can easily add up to tens of thousands of dollars in savings over a 15 or 30-year loan.

This is where the refinance breakeven calculator becomes your best friend. If the math shows you'll break even well before you plan to move, even a small rate improvement is often a brilliant financial move.

Ready to explore your refinancing options with confidence? The expert team at Tiger Loans Inc can help you analyze your breakeven point and find the perfect loan for your financial goals. Start your personalized consultation today.

Alex Chen

Alex Chen

Get in touch with a loan officer

Our dedicated loan officers are here to guide you through every step of the home buying process, ensuring you find the perfect mortgage solution tailored to your needs.

Options

Exercising Options

Selling

Quarterly estimates

Loans

New home

Stay always updated on insightful articles and guides.

Every Monday, you'll get an article or a guide that will help you be more present, focused and productive in your work and personal life.

.png)

.png)

.png)

.avif)

.avif)

.avif)

.png)

.png)

.png)

.avif)

.png)

.png)

.avif)

.png)

.avif)

.png)

.avif)

.avif)