.avif)

When homeowners need funds for home improvements, debt consolidation, or other major expenses, two common options are a Refinance loan and a home equity loan. Both allow you to tap into your home’s value, but each works differently and has unique advantages and risks.

Understanding the differences between these two options is crucial to making the right financial decision. This article explores the key aspects of refinancing and home equity loans, helping you determine which is better for your situation.

What Is a Refinance Loan?

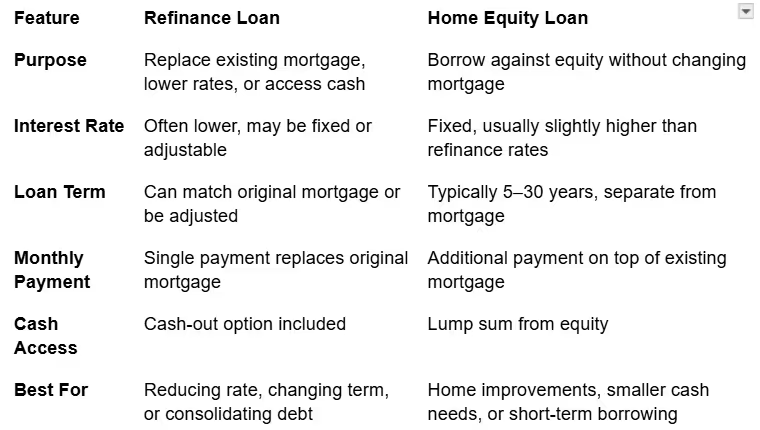

A Refinance loan replaces your existing mortgage with a new one, often with different terms, interest rates, or loan amounts. Homeowners can also use a cash-out refinance to access their home equity in the form of cash.

Key Features of a Refinance Loan:

- Interest Rate: Can be lower than your current mortgage, reducing monthly payments.

- Loan Term: Adjustable to shorten or lengthen the repayment period.

- Cash-Out Option: Borrow more than your current mortgage balance to receive cash for other needs.

- Consolidation: Combine multiple debts into a single loan.

A Refinance loan is typically ideal when your goal is to lower your interest rate, change your mortgage term, or access equity while also refinancing your existing mortgage.

What Is a Home Equity Loan?

A home equity loan is a second mortgage that allows homeowners to borrow against the equity in their home without replacing the original mortgage. It provides a lump sum of money, usually at a fixed interest rate, which is repaid over a set term.

Key Features of a Home Equity Loan:

- Lump Sum: Borrow a fixed amount based on your home’s equity.

- Fixed Interest Rate: Monthly payments are predictable.

- Separate from Mortgage: You maintain your original mortgage while repaying the home equity loan.

- Uses: Ideal for home improvements, education costs, or debt consolidation.

Unlike a Refinance loan, a home equity loan does not replace your current mortgage but adds an additional loan secured by your home.

Comparing Refinance Loan and Home Equity Loan

Benefits of a Refinance Loan

- Lower Interest Rates

Refinancing can help secure a lower rate than your current mortgage or other debts, reducing monthly payments and total interest paid. - Single Loan Payment

A cash-out Refinance loan allows you to consolidate debts into a single payment, simplifying finances. - Potential Tax Benefits

Interest on a cash-out refinance used for home improvements may be tax-deductible. - Flexibility in Loan Term

You can shorten or lengthen your mortgage term to suit your financial goals. - Access to Large Amounts of Cash

Cash-out refinancing can provide more funds than a home equity loan in many cases.

Benefits of a Home Equity Loan

- Predictable Payments

Fixed interest rates provide stability for budgeting. - Separate Loan

Keep your original mortgage intact, which may be useful if your existing mortgage has favorable terms. - Quick Access to Funds

Home equity loans can be processed faster for smaller amounts of money. - No Changes to Original Mortgage

Homeowners with favorable mortgage terms can borrow without altering their existing mortgage.

Drawbacks of a Refinance Loan

- Closing Costs: Fees, appraisal, and lender costs may reduce savings.

- Longer Loan Term: Extending the term may increase total interest paid.

- Risk to Home: Your home is collateral; missed payments could lead to foreclosure.

Drawbacks of a Home Equity Loan

- Separate Payment: Adds to your monthly financial obligations.

- Higher Interest Rate: Usually higher than a cash-out Refinance loan.

- Limited Amount: Based on available equity; may not provide enough funds for larger projects.

Which Option Is Right for You?

Choose a Refinance loan if:

- You want to lower your interest rate or monthly payments

- You plan to consolidate high-interest debt

- You need a significant amount of cash for major expenses

- You are comfortable replacing your existing mortgage

Choose a Home Equity Loan if:

- You want to borrow a smaller, fixed amount

- You prefer to keep your original mortgage intact

- You need a predictable, fixed-rate payment

- You want a faster, simpler application process for a smaller loan

Tips to Make the Right Decision

- Assess Your Financial Goals

Decide whether your priority is lower payments, cash access, or loan term adjustment. - Calculate Total Costs

Consider closing costs, fees, and interest over time to determine the real financial impact. - Evaluate Your Home Equity

Ensure you have enough equity for either option, typically at least 20%. - Compare Multiple Lenders

Rates and fees vary; shopping around ensures the best Refinance loan or home equity loan. - Consult a Financial Advisor

Professionals can help you choose the best option for your long-term financial stability.

Conclusion

Both a Refinance loan and a home equity loan provide access to your home’s equity, but they serve different purposes. A Refinance loan replaces your existing mortgage and may provide a lower interest rate, cash-out options, and flexibility in loan terms. A home equity loan allows you to borrow a fixed sum without altering your current mortgage.

Choosing the right option depends on your financial goals, loan amount needed, repayment preferences, and risk tolerance. Careful evaluation and comparison of options will ensure you select the best solution for your needs.

With the right planning, a Refinance loan or home equity loan can strengthen your financial position, simplify payments, and provide funds for major life expenses while protecting your home and long-term financial health.

Alex Chen

Alex Chen

Get in touch with a loan officer

Our dedicated loan officers are here to guide you through every step of the home buying process, ensuring you find the perfect mortgage solution tailored to your needs.

Options

Exercising Options

Selling

Quarterly estimates

Loans

New home

Stay always updated on insightful articles and guides.

Every Monday, you'll get an article or a guide that will help you be more present, focused and productive in your work and personal life.

.png)

.png)

.png)

.avif)

.avif)

.avif)

.png)

.png)

.png)

.avif)

.png)

.png)

.avif)

.png)

.avif)

.png)

.avif)

.avif)