Steps to Buying Your First Home A Realistic Guide

November 19, 2025

Ready to own? Our guide demystifies the steps to buying your first home. Learn about mortgages, offers, and closing with expert, real-world advice.

So, you're thinking about buying your first home. It's a huge milestone, and while it's incredibly exciting, the road from "just looking" online to actually holding the keys can feel like a marathon. It involves a lot more than just finding a house you love; it’s a journey that starts with some serious financial groundwork and getting pre-approved for a mortgage. After that, the real fun begins: teaming up with a great real estate agent, hunting for "the one," making a smart offer, and navigating all the paperwork to finally close the deal.

Your Realistic Journey to Homeownership

Welcome to the real-deal guide on buying your first place. Let's be honest—the process can feel overwhelming. It’s a world filled with confusing jargon, high stakes, and a market that seems to change by the minute. My goal here is to cut through the noise and give you a clear, achievable roadmap. This isn't just another checklist; it's a genuine look at the entire process, from start to finish.

The journey to homeownership actually begins long before you step foot in an open house. The most important work happens behind the scenes as you get your finances in order. We're talking about everything from polishing your credit score to building up your savings. Before you even think about browsing listings, creating a comprehensive financial plan is the single best thing you can do. It's your compass, helping you make smart, confident decisions when things get complicated.

Understanding Today's Market

It's no secret that today's market is tough. The financial hurdles for new buyers are real, and the data backs it up. It’s not just you—the number of first-time homebuyers has dropped significantly over the past few decades. Back in 1995, almost 3.2 million people bought their first home. Fast forward to 2024, and that number has plummeted to just 1.14 million.

Why the steep decline? A perfect storm of rising home prices—with the median now over $422,000—and mortgage rates that have been hovering near 7%.

But don't let those numbers discourage you. Owning a home is still very much an achievable dream. It just demands more strategy and preparation than it did for previous generations. With the right advice and a solid game plan, you can absolutely navigate this adventure and turn that dream into your reality.

Key Takeaway: The modern home-buying journey demands more than just desire; it requires strategic financial planning and a clear understanding of each phase to succeed in a competitive environment.

I've put together the following table to give you a bird's-eye view of the road ahead. Think of it as your cheat sheet for what's coming.

The First-Time Home Buyer's Roadmap at a Glance

This table lays out the core stages, but remember that the timing for each can vary. To get a better sense of how long everything might take, you can dive into our complete [https://www.tigerloans.com/post/home-buying-process-timeline]. It provides a practical framework for what to expect from day one to closing day.

Getting Your Financial House in Order

Long before you start daydreaming about paint colors or browsing listings online, the real work of buying your first home begins. It starts with a hard, honest look at your finances. This isn't just about saving money; it's about building a rock-solid financial profile that makes lenders eager to work with you. Getting this part right is what separates the dreamers from the homeowners.

Your journey kicks off with a deep dive into your financial health. Think of it less like balancing a checkbook and more like prepping for a big exam—you need to know exactly what the lenders will be grading you on. The two most critical numbers in their playbook are your credit score and your debt-to-income ratio.

Understanding the Numbers That Matter: DTI and Credit

Your debt-to-income (DTI) ratio sounds complicated, but it's a straightforward yet powerful metric. It’s simply your total monthly debt payments (think car loans, student loans, credit cards) divided by your gross monthly income. Most lenders want to see a DTI of 43% or lower.

So, if you bring in $6,000 a month before taxes, all your debt payments—including your potential new mortgage—should ideally stay under $2,580. A high DTI is one of the quickest ways to get a "no" from an underwriter.

Your credit score is the other half of this power duo. You don’t need a flawless 850, but a stronger score opens the door to much better interest rates. I've seen firsthand how a few points can save a buyer tens of thousands of dollars over the life of their loan. Aim for a score of 740 or higher to get the best possible terms. If you're not there yet, focus relentlessly on paying every bill on time and chipping away at high-interest credit card balances.

A Quick Reality Check: Lenders are looking for a track record of responsibility. It's not just about the money you have saved; it's about proving you can handle debt and live within your means. They want to see a story of financial stability.

Saving for Your Down Payment and Closing Costs

Let's talk about the elephant in the room: saving up a huge pile of cash. It’s one of the biggest hurdles, but I have good news. The old 20% down payment rule is more of a myth than a mandate these days. Many loan programs are built specifically to help first-time buyers get in the door with a lot less.

As you start socking money away, where you put it matters. You need it to be safe, but you also want it to work for you. Looking into the best short-term investments for savers is a smart move. Options like high-yield savings accounts can give your funds a nice little boost without the risks of the stock market.

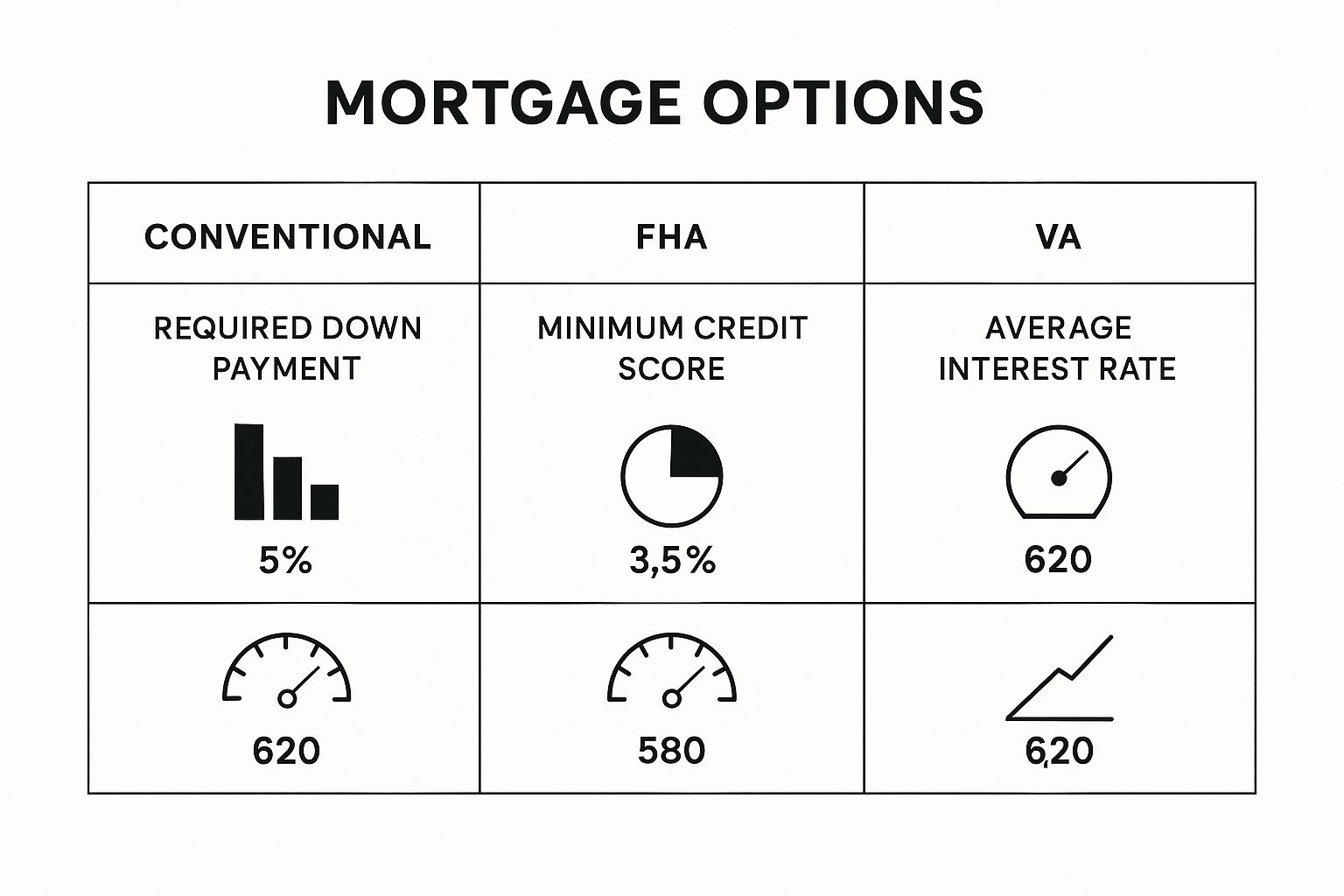

To help you see what’s possible, let’s compare some of the most common loan types available to first-time home buyers.

Comparing Popular First-Time Home Buyer Loan Types

This table breaks down the key features of different mortgages. It's designed to help you quickly see which one might be the best fit for your financial situation.

As you can see, programs like FHA and VA loans are game-changers, making homeownership a real possibility for people who don't have a 20% down payment saved up.

But the down payment isn't the only cash you'll need. Don't forget about closing costs. These are the fees you pay to finalize the mortgage, and they typically run between 2% to 5% of the home's purchase price.

These costs cover a variety of essential services, including:

- Loan Origination Fees: What the lender charges for creating the loan.

- Appraisal Fees: Paying a professional to confirm the home is worth what you're paying.

- Title Insurance: Protects you and the lender from future ownership claims.

- Home Inspection Fees: A must-do step to uncover any hidden problems with the house.

- Prepaid Expenses: Your first payments for property taxes and homeowner's insurance.

These fees should never be a last-minute surprise. Your lender will provide a detailed Loan Estimate that itemizes every single cost, so you know exactly how much to budget. By strengthening your credit, managing your DTI, and strategically saving for both the down payment and closing costs, you’ll walk into a lender's office with the confidence of a well-prepared buyer they can't afford to turn away.

Getting Pre-Approved and Building Your A-Team

Alright, you've done the hard work of getting your financial ducks in a row. Now it’s time for the step that officially gets you in the game: securing a mortgage pre-approval.

Think of a pre-approval letter as your golden ticket. It transforms you from someone just window-shopping on Zillow into a serious, qualified buyer who sellers will actually pay attention to. In today's market, it’s not just a nice-to-have; it's an absolute must.

It's easy to mix up pre-qualification and pre-approval, but they couldn't be more different. A pre-qualification is basically a quick, informal guess of what you might be able to borrow based on what you tell a lender. A pre-approval, on the other hand, is the real deal. It’s a lender’s conditional promise to loan you a specific amount of money, and it only comes after they’ve dug into your finances and pulled your credit.

Sellers see an offer backed by a pre-approval letter and know you’re a sure thing. That confidence can give you a powerful advantage, sometimes even enough to beat out a slightly higher offer from a buyer who hasn't done their homework.

What Lenders Look For

Getting pre-approved does mean you’ll need to gather a bit of paperwork. It feels like a lot, but remember, you're asking someone to lend you hundreds of thousands of dollars. They need to be absolutely certain you're a good bet.

Here’s a quick rundown of what you’ll likely need to pull together:

- Income Verification: This means recent pay stubs (usually from the last 30 days), your W-2s from the past two years, and your last two years of federal tax returns.

- Asset Statements: Lenders want to see your bank statements (checking and savings) for the last two or three months. They're making sure you have the funds ready for your down payment and closing costs.

- Debt Records: You'll need to provide recent statements for any debts you have, like credit cards, car loans, or student loans.

- Personal ID: A copy of your driver's license and your Social Security number are standard for verifying your identity and running that all-important credit check.

Want a full checklist of the documents and a deeper dive into what underwriters are looking for? Check out our essential guide to getting pre-approved for a home loan.

Expert Insight: Here's a pro tip: avoid making any large cash deposits into your bank accounts for a few months before you apply. Lenders have to source every penny, and a sudden, unexplained chunk of cash can create major headaches and slow down your approval.

Finding an Agent Who's in Your Corner

Your pre-approval letter gets you in the door, but a great real estate agent is the one who will guide you to the finish line. This isn't just about finding someone to unlock houses for you. You need a true advocate, someone who gets the jitters of being a first-time buyer and will fight for your best interests.

A fantastic place to start is by asking friends, family, or colleagues who they used and loved. Personal referrals are often gold. You can also research agents who specialize in your target neighborhoods and have a track record of working with first-timers.

When you start talking to potential agents, don't hold back. This is a job interview, and you're the one hiring. Ask pointed questions like:

- How many first-time buyers did you work with last year?

- What’s your communication style? How often will I hear from you?

- In a bidding war, what’s your strategy for making my offer win?

A top-notch agent does so much more than show you properties. They offer priceless market knowledge, recommend other pros like inspectors and attorneys, and act as your strategic partner from day one. Building this team is one of the most important things you'll do on your journey to homeownership.

Winning the House Hunt and Making Your Offer

Alright, you’ve got your pre-approval letter and a great agent in your corner. Now for the fun part: the hunt. This is where your dream of homeownership starts to feel real, but it’s also where you need a clear strategy to keep your emotions in check.

Let’s be honest, finding the “perfect” house is a myth. The real goal is finding the right house for you, right now.

The first step is to get brutally honest about your wishlist. You need to separate your absolute, non-negotiable must-haves (like three bedrooms or a specific school district) from your nice-to-haves (that gorgeous clawfoot tub or a brand-new kitchen). This simple exercise will keep you from getting sidetracked by pretty staging and focused on what truly fits your life.

Knowing who you’re up against is also key. Younger Millennials (ages 18 to 25) are a major force in the market, with a whopping 71% buying their first home last year. Most buyers—about 75% in fact—are snapping up detached single-family homes, typically in the suburbs. Understanding this landscape helps you and your agent build a smart, competitive strategy. You can dive deeper into these numbers in the 2025 Home Buyers and Sellers Generational Trends Report.

From Wishlist to Winning Offer

Once you find a house that hits all your high notes, it's time to shift gears from house hunter to serious buyer. Crafting a compelling offer is a genuine art form, a careful balance of price, timing, and terms. Remember, the highest price doesn't always win the day; a clean, well-thought-out offer can be much more attractive to a seller.

Your offer is a complete package, not just a number. It has several crucial parts:

- The Price: This is what you're offering to pay.

- Earnest Money Deposit (EMD): A good-faith deposit, usually 1-3% of the sale price, that proves you're serious.

- Contingencies: These are conditions that must be met for the sale to proceed.

- Closing Date: Your proposed timeline to seal the deal.

Think of your offer as your opening argument. A strong earnest money deposit shows you have skin in the game, and a flexible closing date might be just the thing that makes your offer stand out to a seller with a specific timeline.

Insider Tip: Try writing a personal letter to the seller. It doesn’t always work, but sharing what you love about their home can forge a human connection. I’ve personally seen it tip the scales in my client's favor more than once when the offers were practically identical.

The Power of Smart Contingencies

Contingencies are your escape hatches. They are clauses in the purchase contract that give you a legal out if something goes wrong, usually allowing you to get your earnest money back. For a first-time buyer, they are your single most important tool for financial protection.

Here are the most common ones you'll see:

- Inspection Contingency: Gives you the right to have the home professionally inspected and then walk away or renegotiate if you uncover major problems.

- Appraisal Contingency: Protects you if the bank's appraisal comes in lower than your offer price.

- Financing Contingency: Lets you off the hook if your mortgage loan doesn't get final approval.

These clauses are designed to reduce your risk by making the contract conditional on these key events. In a competitive market, you might feel pressure to waive them to make your offer look better. Be extremely careful here. Giving up these protections is a high-stakes gamble.

Always, always talk through the worst-case scenarios with your agent before you even consider it. The goal isn't just to win a bidding war; it's to make a sound, secure investment in your future.

Alright, your offer was accepted! Pop the champagne, do a happy dance—you’ve earned it. This is a massive milestone. But before you start packing, know that the race isn't quite over. You've just entered the final, and arguably most critical, leg of the journey: the escrow period.

This is typically a 30 to 60-day window where a neutral third party, the escrow company, acts as the referee. They hold onto your deposit and all the important legal documents, making sure everyone plays by the rules laid out in the contract. Nothing becomes final until every single condition is met.

Think of this time as your last chance to peek behind the curtain. You'll be doing your due diligence, finalizing your mortgage, and making absolutely certain this is the right home for you before you sign on the dotted line for good.

The Home Inspection: Your Financial Safety Net

One of the very first calls you or your agent should make is to a home inspector. I can't stress this enough: do not skip the inspection, no matter how pristine the house looks. This is one of the most powerful tools a buyer has. Your agent will know some reputable, certified inspectors, so lean on their experience.

A good inspector will spend a few hours combing through the property, looking at all the big-ticket items that can cost a fortune to fix later. They're checking:

- The Bones: Foundation, roof, walls, and attic.

- The Guts: HVAC, plumbing, and the electrical system.

- The Essentials: Major appliances that come with the home.

- The Dangers: Red flags like mold, hidden water damage, or sketchy wiring.

You'll get a detailed report back in a day or two, usually packed with photos. Don't let the length of the report freak you out—every house has a list of flaws, even brand-new ones. Your job is to focus on the serious stuff: health and safety issues or major systems on their last legs.

Real-World Scenario: Let's say the inspector finds the furnace is 20 years old and running on fumes. This is where your inspection contingency gives you leverage. You can go back to the seller and ask them to replace it before closing. Or, you could ask for a $5,000 credit, letting you pocket the cash and handle the replacement yourself after you move in.

The Appraisal and Final Loan Gauntlet

While you're dealing with the inspection, your lender is setting up their own big step: the home appraisal. They’ll hire an independent appraiser to determine the home's fair market value. This isn't for you—it's for them. The bank needs to be sure the property is worth the loan amount they're giving you.

But what if the appraisal comes in low? It happens. Say you agreed to pay $350,000, but the appraiser says the home is only worth $340,000. The lender won't finance that $10,000 gap. At this point, you've got a few paths: negotiate with the seller to drop the price, cover the difference with your own cash, or, if your contract has an appraisal contingency, you can walk away from the deal and get your deposit back.

Once the appraisal checks out and you've navigated any inspection negotiations, your loan file heads to underwriting for the final verdict. The underwriters will comb through your finances one last time. Heads up: this is not the time to make any big financial moves. Don't go finance a new car or run up your credit cards on furniture. Any sudden change to your debt-to-income ratio could put your entire mortgage in jeopardy right at the finish line.

Gearing Up for Closing Day

Roughly three business days before you're scheduled to close, a very important document will hit your inbox: the Closing Disclosure (CD). This five-page form lays out all the final, official numbers for your mortgage—your interest rate, monthly payment, and a full list of your closing costs.

Read this document line by line. Compare it to the Loan Estimate you got at the beginning of the process. The figures should be very close. It's easy for fees to add up, so understanding exactly what you're paying for is key. To get a better handle on what to expect, it's a good idea to review the 5 hidden costs of buying a home so there are no last-minute shocks.

Right before you head to the closing itself, you'll do one last final walkthrough. This is your chance to confirm the property is in the same condition you agreed to buy it in and to make sure the seller has completed any repairs they promised to make.

And then, it's here—closing day. You’ll sit down with your agent and a closing agent or attorney to tackle a mountain of paperwork. Be sure to bring your government-issued ID and a cashier's check for the down payment and closing costs.

Once the last page is signed and the money has been officially transferred, you'll get the keys. Just like that, it's real. The house is yours. Congratulations, homeowner

Answering Your Biggest First-Time Home Buyer Questions

The path to your first home is exciting, but let’s be honest—it’s also filled with new lingo and steps you’ve never taken before. It’s completely natural for questions to bubble up, and feeling a little uncertain is part of the process.

Think of us as your experienced guide. We’ve heard every question in the book from first-time buyers, and we've put together answers to the most common ones. Our goal is to replace that hesitation with confidence so you can make smart decisions when it counts.

How Much Do I Really Need for a Down Payment?

Let's bust a huge myth right away: you absolutely do not need to put 20% down to buy a home. It's an old, outdated rule of thumb. While a 20% down payment does let you skip Private Mortgage Insurance (PMI), it's not a realistic starting point for most first-time buyers.

The truth is, modern lending has some incredibly flexible options.

- FHA Loans: A favorite among new buyers, these government-backed loans often require just 3.5% down.

- VA & USDA Loans: If you're an eligible veteran or are buying in a qualifying rural area, you could get a loan with 0% down. It's a true game-changer.

- Conventional Loans: Even standard mortgages now offer options for as little as 3-5% down for qualified borrowers.

The secret is to explore these different loan types with your lender. Also, be sure to ask about Down Payment Assistance (DPA) programs. These state and local grants or low-interest loans are designed specifically to help new buyers cover their upfront costs.

What if the Home Inspection Uncovers Big Problems?

First off, take a breath. It is completely normal for a home inspection to find issues—in fact, it means your inspector is doing a great job! This is precisely why you have an inspection contingency in your offer; it gives you leverage.

When the report comes back with some red flags, you have a few solid options. You can ask the seller to make the repairs before you close. Or, you could negotiate a credit, which reduces your closing costs and leaves you with the cash to handle the repairs yourself after you move in.

If the problems are truly deal-breakers, like a cracked foundation or major mold, your inspection contingency allows you to walk away from the purchase entirely and get your earnest money back. This is where your real estate agent becomes your best ally, helping you navigate the negotiations for a fair outcome.

An Inspection Report Isn't a Pass/Fail Test. Think of it more like a detailed owner's manual for your new home. It points out what needs attention now and what you should budget for down the road, empowering you to be a proactive homeowner from day one.

How Long Does This Whole Process Really Take?

While every home-buying journey is unique, a good ballpark estimate is anywhere from 3 to 6 months from start to finish. This timeline gives you enough room to breathe and avoid feeling rushed into one of the biggest financial commitments of your life.

Here's a rough breakdown of that timeline. The initial phase—getting your finances in order, finding a lender, and actively searching for a home—usually takes about 1 to 2 months. Once your offer is accepted, the closing process (escrow) typically takes another 30 to 60 days.

In a hot market, the house hunt itself might take a bit longer. The single best way to keep things moving and prevent delays? Get that mortgage pre-approval locked in early and have all your financial documents ready to go. To stay on top of everything, a detailed first-time homeowner checklist can be an invaluable tool to make sure you’re prepared for every stage.

Is a Mortgage Pre-Approval Really That Important?

Yes. It's not just important—it's absolutely essential. Don't confuse it with a pre-qualification, which is just a rough estimate based on numbers you provide. A pre-approval is a serious commitment from a lender, issued only after they've verified your income, assets, and credit.

In today's competitive housing market, showing up with a pre-approval letter tells sellers you are a serious, vetted buyer who can actually close the deal. It gives your offer instant credibility and puts you in a much stronger negotiating position from the very beginning.

At Tiger Loans Inc, we specialize in guiding first-time buyers through every single step of this process. From securing that crucial pre-approval to finding the right loan for your situation, our team is here to give you the clarity and support you deserve. Ready to take the next step with confidence? Explore your mortgage options with us today!

Alex Chen

Alex Chen

Get in touch with a loan officer

Our dedicated loan officers are here to guide you through every step of the home buying process, ensuring you find the perfect mortgage solution tailored to your needs.

Options

Exercising Options

Selling

Quarterly estimates

Loans

New home

Stay always updated on insightful articles and guides.

Every Monday, you'll get an article or a guide that will help you be more present, focused and productive in your work and personal life.

.png)

.png)

.png)

.avif)

.avif)

.avif)

.png)

.png)

.png)

.avif)

.png)

.png)

.avif)

.png)

.avif)

.png)

.avif)

.avif)