.avif)

When considering a Refinance loan, one of the most important decisions homeowners face is choosing between a fixed-rate mortgage and an adjustable-rate mortgage ARM. Each option has unique benefits and risks, and understanding the differences can help you select the right loan for your financial goals.

This article explains fixed and adjustable-rate refinancing, the advantages and disadvantages of each, and tips to help you make an informed decision.

What Is Fixed-Rate Refinancing?

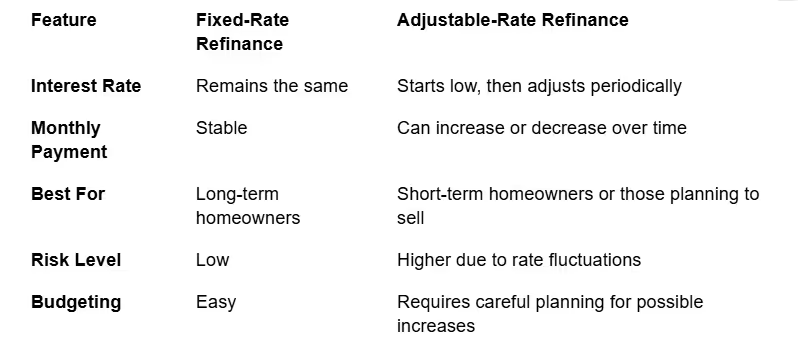

A fixed-rate Refinance loan has an interest rate that remains the same for the entire term of the mortgage. This provides stability and predictable monthly payments.

Benefits of Fixed-Rate Refinancing:

- Predictable payments: Your monthly principal and interest stay the same, making budgeting easier.

- Protection against interest rate increases: Even if market rates rise, your mortgage rate remains locked.

- Peace of mind: Knowing your payments won’t fluctuate reduces financial stress.

Considerations:

- Fixed rates are usually slightly higher than initial ARM rates.

- Lower rates may be available for shorter fixed terms, but payments will be higher.

What Is Adjustable-Rate Refinancing?

An adjustable-rate Refinance loan ARM has an interest rate that can change periodically based on market conditions. Typically, ARMs start with a lower initial rate for a set period, such as 5, 7, or 10 years, and then adjust annually.

Benefits of Adjustable-Rate Refinancing:

- Lower initial payments: ARMs often start with lower rates compared to fixed-rate loans.

- Potential savings if rates remain low: If interest rates do not rise, you may save money over the life of the loan.

- Good for short-term plans: If you plan to sell or refinance again before the rate adjusts, ARMs can be cost-effective.

Considerations:

- Payments can increase significantly after the initial period.

- Budgeting is more challenging due to fluctuating interest rates.

- Risk of higher long-term interest costs if rates rise.

Comparing Fixed and Adjustable-Rate Refinancing

When to Choose Fixed-Rate Refinancing

Fixed-rate Refinance loans are ideal for homeowners who:

- Plan to stay in their home long-term

- Prefer stable, predictable payments

- Want protection against rising interest rates

- Are comfortable with slightly higher initial payments in exchange for long-term stability

Fixed-rate refinancing is especially recommended during periods of historically low interest rates, as locking in a low rate can save substantial money over the life of the loan.

When to Choose Adjustable-Rate Refinancing

Adjustable-rate Refinance loans may be suitable for homeowners who:

- Plan to sell or move within a few years

- Want lower initial monthly payments

- Are willing to accept some risk for potential savings

- Have the ability to handle possible future payment increases

An ARM can be a strategic choice for those who want short-term savings or who anticipate declining interest rates in the future.

Tips for Choosing Between Fixed and Adjustable Rates

- Assess your time horizon

Determine how long you plan to stay in your home. Fixed rates are better for long-term homeowners, while ARMs can benefit short-term homeowners. - Evaluate your risk tolerance

Consider your ability to handle payment increases if rates rise. Fixed rates offer security, whereas ARMs carry more risk. - Compare total costs

Look at the total interest paid over the expected period. Sometimes an ARM may save money initially, but long-term costs could exceed a fixed-rate Refinance loan. - Check market conditions

Interest rate trends can influence your decision. A fixed-rate may be best during rising-rate environments, while an ARM could be advantageous if rates are expected to drop or remain low. - Consult a financial advisor

A professional can help evaluate your situation, goals, and risk tolerance to recommend the best option.

Conclusion

Choosing between a fixed-rate and an adjustable-rate Refinance loan is a critical decision that affects your monthly payments, long-term interest costs, and financial stability. Fixed-rate refinancing provides predictability and protection against rate increases, while adjustable-rate refinancing offers lower initial payments and potential short-term savings.

By understanding your goals, evaluating your financial situation, and comparing options, you can select the right refinance strategy that aligns with both your current needs and long-term financial plans.

A well-chosen Refinance loan can save you money, improve your cash flow, and strengthen your overall financial health.

Alex Chen

Alex Chen

Get in touch with a loan officer

Our dedicated loan officers are here to guide you through every step of the home buying process, ensuring you find the perfect mortgage solution tailored to your needs.

Options

Exercising Options

Selling

Quarterly estimates

Loans

New home

Stay always updated on insightful articles and guides.

Every Monday, you'll get an article or a guide that will help you be more present, focused and productive in your work and personal life.

.png)

.png)

.png)

.avif)

.avif)

.avif)

.png)

.png)

.png)

.avif)

.png)

.png)

.avif)

.png)

.avif)

.png)

.avif)

.avif)