VA Eligibility Loan Guide: Unlock Your Benefits Today

November 19, 2025

Learn about VA eligibility loan requirements, service criteria, and how to obtain your COE. Discover how to qualify for your military home loan benefit.

Think of buying a home as your next big mission. If that's the case, the VA loan is the most powerful tool in your arsenal—one you've rightfully earned to guarantee success. This isn't just another home loan; it’s a tangible thank you for your service, designed specifically to put the keys to a new home in your hand.

Your Mission To Homeownership Starts Here

Forget the dense, confusing banker-speak. Let's map this out like any successful operation: with a clear objective and a step-by-step plan. This guide is your briefing, breaking down every piece of the VA loan eligibility puzzle to make the whole process feel less intimidating and completely within your control.

The VA home loan program is a serious commitment from the nation to those who've served. The numbers speak for themselves. As of May 31, 2025, the Department of Veterans Affairs has backed over 259,000 VA loans across the country, totaling more than $100 billion. With an average loan amount hitting $387,461, it's clear this program is a major force helping military families plant their roots. You can even explore more data on VA loan trends to see the massive scale of its impact.

The Power Of Your Earned Benefit

The VA loan stands apart from conventional mortgages because it was built from the ground up with the military community in mind. Its core features aren't just minor perks; they are genuine game-changers.

Here’s what makes it so powerful:

- No Down Payment: This is the big one. For almost every qualified borrower, the ability to buy a home without a massive upfront investment is the single greatest hurdle cleared.

- No Private Mortgage Insurance (PMI): On other low-down-payment loans, you'd be stuck paying PMI every month. The VA loan eliminates this, saving you a significant amount on your monthly payment.

- Competitive Interest Rates: Because the loan is backed by the government, lenders see it as a lower-risk proposition. That often translates directly into better interest rates for you.

- Limited Closing Costs: The VA puts a cap on the closing costs lenders can charge, protecting you from excessive fees and keeping more of your cash in your pocket.

This isn't a handout; it's a benefit you earned through your service. Knowing how to leverage it is the first critical step toward securing a home for your family and building your future.

Consider this guide your official field manual. We're going to cover everything—from service time and credit scores to the exact paperwork you’ll need—giving you all the intel required to execute your homebuying mission with absolute confidence.

Confirming Your Service for VA Loan Eligibility

Before we can even start talking about interest rates or closing costs, we have to tackle the first and most fundamental question: does your military service make you eligible for a VA loan? Think of this as the gatekeeper to one of the most powerful homebuying benefits you've earned. It’s not about some bureaucratic checklist; it's about matching your unique service history—whether active duty, veteran, or in the Guard or Reserves—to the VA's guidelines.

The Department of Veterans Affairs has clear-cut criteria based on when and how you served. Let’s break it down so you know exactly where you stand.

Active Duty and Veteran Service Paths

For most folks, figuring this out is pretty straightforward. If you're currently on active duty, the path is simple: you generally qualify after just 90 continuous days of service. This is a huge advantage, allowing you and your family to put down roots and buy a home even while you're still serving.

For veterans, the main thing to look at is when you served. The VA often draws a line between "wartime" and "peacetime" service, and each has its own minimum time commitment.

Let's take a common example: Gulf War-era veterans (that's anyone who served from August 2, 1990, to the present). The standard requirement is 24 continuous months of service. But—and this is a big but—if you were called up for active duty during that time, the requirement plummets to only 90 days.

It's a classic misconception that you need to have served for years on end to qualify. The reality is, for many veterans, especially those who served during designated wartime periods, the requirement is much, much shorter than they think.

Knowing which bucket your service falls into clears up the confusion right away and tells you if you’ve got the green light to move forward.

Qualifying Through National Guard or Reserve Service

What if your service was in the National Guard or Reserves? Your path to a VA loan is just as valid, though the clock works a little differently. Instead of counting continuous active-duty days, eligibility is usually based on years of service.

The general rule of thumb is that you need six creditable years in the Selected Reserve or National Guard. Once you hit that six-year milestone and have an honorable discharge, you've officially met the service requirement.

However, just like with veterans, there's a major exception that can speed things up considerably. If you were called to active duty service under federal orders (specifically Title 10), the rules change to mirror your active-duty counterparts. Members of the Guard and Reserves who were activated for at least 90 continuous days can qualify much sooner. This is the VA’s way of recognizing that so many in the Guard and Reserves have served shoulder-to-shoulder with regular military personnel in combat zones.

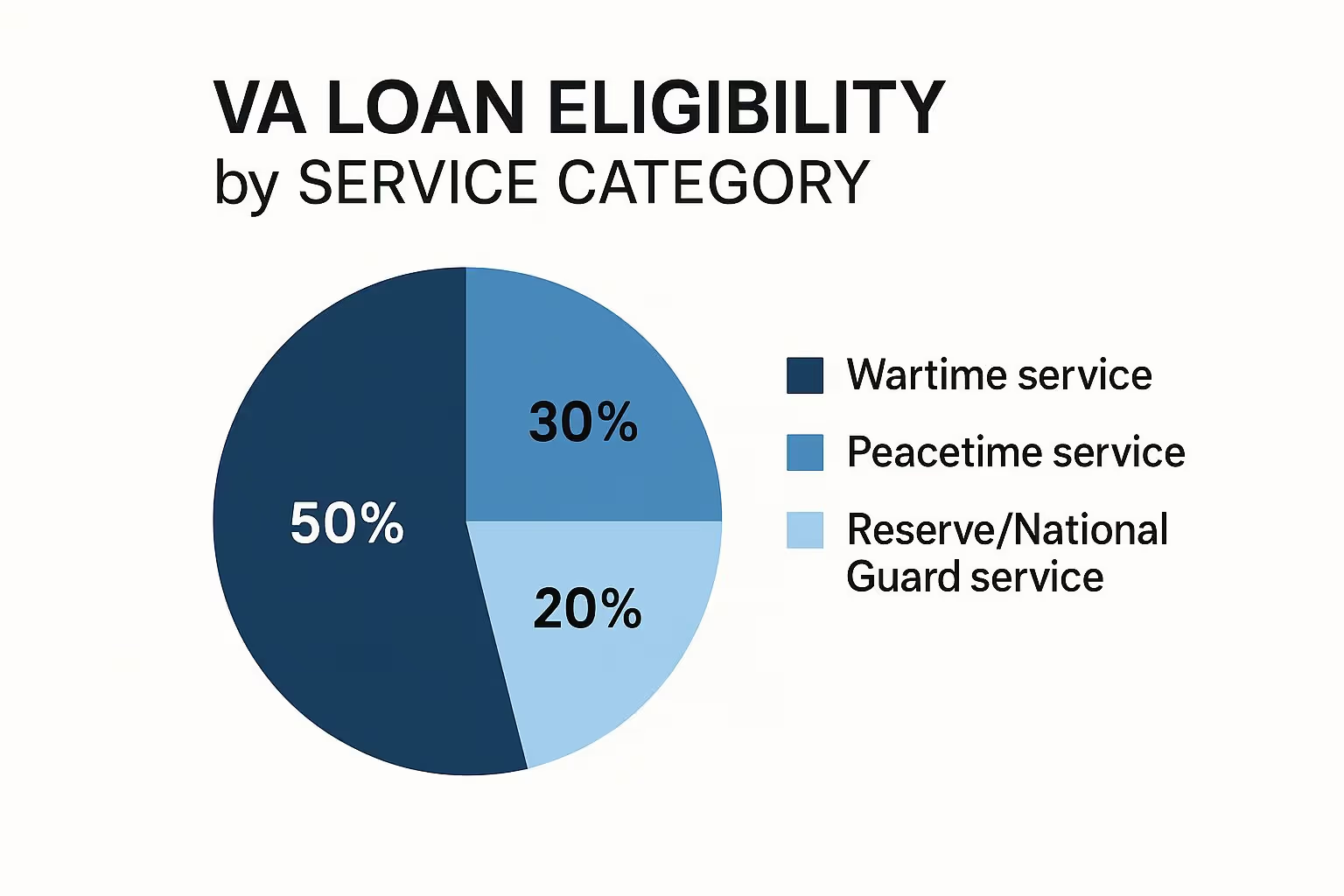

This visual gives you a good sense of how different service types contribute to the overall program.

As you can see, while wartime service is a common route, peacetime and Reserve/Guard members make up a huge portion of those who qualify, showing just how broad this benefit really is.

Key Service Eras and Requirements

To make this crystal clear, let's lay out the minimums based on specific service periods. This table is a great cheat sheet for pinpointing your eligibility. If you want an even more detailed breakdown, I highly recommend reading our full guide on understanding your VA housing loan eligibility.

VA Loan Minimum Service Requirements

Here’s a quick summary of the active-duty service time needed to qualify, depending on when you served.

Service PeriodMinimum Service Requirement (Veterans)Active Duty MembersGulf War (Aug 2, 1990 - Present)24 continuous months or at least 90 days of active duty90 continuous daysPost-Vietnam (May 8, 1975 - Sep 7, 1980)181 continuous days90 continuous daysVietnam War (Aug 5, 1964 - May 7, 1975)90 total days90 continuous daysKorean War (Jun 27, 1950 - Jan 31, 1955)90 total days90 continuous days

This table simplifies the time-in-service rules, but remember the other critical piece of the puzzle: your discharge status.

No matter when you served, the character of your discharge is non-negotiable. To be eligible for a VA loan, you must have a discharge that is anything other than dishonorable. For most, this means an honorable or general discharge. If you received a different type of discharge, you aren't automatically disqualified, but the VA will need to make a "character of service" determination before you can proceed.

Once you’ve lined up your service history with these guidelines, you can move forward with confidence. You’ll know you’ve cleared the first and most important hurdle on your path to owning a home.

Getting Your Certificate of Eligibility (COE)

Alright, so you’ve confirmed your service history lines up with the VA's requirements. What's next? You need to get the official document that proves it: the Certificate of Eligibility (COE).

Think of the COE as your golden ticket for the VA loan process. It’s the one piece of paper that tells a lender, “Yes, this person has absolutely earned their VA eligibility loan benefit.”

This isn't just bureaucratic red tape. The COE is the key that unlocks the whole program, turning your theoretical eligibility into a real-world tool you can use to buy a home. Without it, a lender simply can’t move forward with a VA-backed mortgage.

The good news? Getting your COE is often much quicker and easier than you might think. You've got a few ways to tackle it, and one method is built for pure speed.

The Fastest Path: Let Your Lender Do the Work

By far, the most efficient route is to let your VA-approved lender grab the COE for you. Lenders who specialize in VA loans have direct access to a dedicated portal called the VA's Web LGY (Loan Guaranty) system.

In many cases, they can plug in your details and get your COE back in minutes—sometimes almost instantly. This takes the task completely off your plate and folds it right into the loan application itself. There's a reason this is the preferred method: it's fast, it's simple, and it means less paperwork for you.

Your Golden Ticket: Don't look at the COE as another hurdle. See it as your official pass—the document that proves to lenders you have VA loan eligibility and are ready to go.

Now, sometimes the VA’s automated system hits a snag and can't verify eligibility instantly. This can happen in more complex situations, like those involving certain types of National Guard service or a surviving spouse. If that’s the case, you’ll just need to provide the documentation yourself.

Applying for Your COE Directly

If your lender can’t pull the COE instantly, or if you'd just rather handle it on your own, you can apply directly with the VA. The process is still straightforward, but you’ll need to have the right documents ready to go based on your specific service status.

1. For Veterans and Service Members:The key document here is your DD Form 214, the Certificate of Release or Discharge from Active Duty. It contains everything the VA needs to see, like your service dates and the character of your discharge.

If you're still on active duty, you'll need a statement of service instead. This must be signed by your commander or a personnel officer and include your full name, Social Security number, date of birth, active duty entry date, any lost time, and the name of your command.

2. For National Guard or Reserve Members:You'll need to submit your latest annual retirement points statement along with proof of your honorable service. If you were ever activated under federal orders, you may need your DD Form 214 as well.

3. For Surviving Spouses:As a surviving spouse, you’ll need to complete a specific form (VA Form 26-1817). You'll also have to provide the veteran's DD Form 214, your marriage license, and the veteran's death certificate.

Once your documents are in order, you can apply online through the VA’s eBenefits portal or mail in a paper application (VA Form 26-1880). The online route is always faster, but having your paperwork correct from the start is what really makes the difference.

This is a step more and more veterans are taking, particularly younger ones. Veteran homebuyers from Generation Z have helped fuel a major increase in VA loan use. In the first half of Fiscal Year 2025, total VA loans shot up by 45% over the previous year, and refinance loans exploded by an incredible 150%. You can read more about the impact Gen Z is having on VA loans.

Getting your COE makes your VA eligibility loan status official. It signals to everyone—your real estate agent, your lender, and the seller—that you are a serious, qualified buyer. It’s the definitive green light for your homeownership mission.

Meeting Lender Credit and Income Standards

Alright, so you’ve got your Certificate of Eligibility (COE) in hand. That’s a huge step—it means the VA has officially confirmed your service meets the requirements. Think of it as your golden ticket. Now, the spotlight shifts from your service history to your financial picture. This is where your lender comes in to make sure you can truly afford the home you want.

Let's clear up one of the biggest misconceptions right out of the gate: the VA itself does not have a minimum credit score requirement. That's a core benefit of the VA eligibility loan program. However, the private lenders—the banks and mortgage companies actually providing the money—absolutely do have their own credit standards.

This is where you'll hear the term "lender overlays." It's a simple concept. The VA sets the baseline rules for the loan, but lenders can add their own, stricter rules on top to protect their investment. A minimum credit score is the most common overlay, and for most lenders, that magic number is around 620.

The Unofficial Benchmark: The 620 Credit Score

So, why 620? In the eyes of most lenders, a 620 score is a pretty solid indicator that you manage your finances responsibly. It signals a lower risk. While it isn't a hard-and-fast rule from the VA, it has become the standard benchmark in the industry for getting a VA loan with good terms.

Does a score below 620 automatically mean you're out of the running? Not at all. Some fantastic lenders specialize in working with veterans who have a few dings on their credit. But, being honest, a score north of that number will open more doors and make the whole approval process a lot smoother.

If your score isn't quite there yet, don't sweat it. Here are a few things you can do right now to polish your credit profile:

- Be Your Own Detective: Grab your free credit reports from the big three bureaus—Equifax, Experian, and TransUnion. Go through them with a fine-tooth comb and dispute any errors you find. A mistake on your report isn't your fault, and fixing it can sometimes give you a quick score bump.

- Attack High-Interest Debt: Zero in on paying down credit card balances. This lowers your credit utilization ratio (how much you owe vs. your total credit limit), which is a massive factor in your score.

- Consistency is Key: Your payment history is the king of credit factors. Make it a mission to pay every single bill on time. Every time.

These small, disciplined habits show lenders you're reliable, and that can make all the difference.

Understanding Your Debt-to-Income Ratio

Beyond your credit score, lenders will get out their calculators and look at your debt-to-income (DTI) ratio. It’s just a percentage that shows how much of your monthly income goes toward paying your debts. The math is simple: your total monthly debt payments divided by your gross monthly income. As a general rule, the VA likes to see a DTI of 41% or less.

Picture your monthly income as a pizza. Lenders want to see that after you’ve handed out slices for your car payment, student loans, and credit cards, there’s still a big enough piece left over for your new mortgage and all the other costs of living. A DTI under 41% tells them you're not stretched too thin.

But here's what truly sets the VA loan apart: the VA encourages lenders to look beyond just the numbers. They want to see your whole financial story to determine if you can truly succeed as a homeowner, focusing on real-world affordability over a simple credit score.

This holistic approach leads us to the VA loan’s most powerful and unique financial requirement.

Residual Income: The VA’s Secret Weapon

This is where the VA eligibility loan really flexes its muscles. Unlike almost any other mortgage, the VA requires lenders to calculate your residual income. This is the money you have left in your pocket after you’ve paid all your major monthly bills—we’re talking the new mortgage payment, property taxes, insurance, and all your other loan payments.

Think of it as your family's financial safety net. It’s the cash you have on hand for the day-to-day essentials: groceries, gas, clothes, and those unexpected emergencies that life loves to throw at us. The VA even sets specific minimum residual income amounts you must have, which change based on your family size and where you live. This ensures you can not only afford the mortgage but also live comfortably.

For example, a family of four living in the Midwest might need to show they have at least $1,003 left over each month. This is a real-world stress test of your budget, and frankly, it's far more practical than just a DTI ratio. It proves you have the breathing room to handle life’s curveballs without putting your home at risk.

To get ready for this part of the process, start gathering documents for all your income sources—your primary salary, BAH, any part-time work, or disability benefits. When you present a clear and complete picture, you help your lender see your true financial strength.

How VA Loan Entitlement Maximizes Your Benefit

One of the biggest misconceptions about the VA loan is that it's a one-and-done deal. That couldn't be further from the truth. The real power behind your VA benefit lies in something called entitlement.

Think of your entitlement as a personal guarantee the VA provides to your mortgage lender. It’s like the VA is co-signing for a portion of your loan, telling the bank, "We've got your back on this." This guarantee is the magic ingredient that makes the famous $0 down payment possible. Understanding how this works is the key to using your VA loan benefit over and over again.

Full Entitlement vs. Remaining Entitlement

When you’re a first-time VA loan user, you start with "full entitlement." This is the maximum guarantee the VA offers. With full entitlement, there's no official VA loan limit. As long as you have the income and credit to qualify with a lender, you can buy a home at any price with $0 down.

But what happens after you’ve bought that first home? This is where “remaining entitlement” becomes your best friend. If you already have a VA loan, your benefit isn’t tapped out. You simply have a remaining balance you can use for another purchase. This is a game-changer for military families who get PCS orders and need to buy a new home without selling their old one first.

Your VA loan entitlement is a lifelong benefit designed for reuse. By understanding how to restore it or use your remaining balance, you can leverage it again and again to build wealth through real estate.

How Entitlement Works in the Real World

So, let's get into the numbers. Every eligible service member, veteran, or surviving spouse starts with a basic entitlement of $36,000. But that’s not the whole story. The VA also provides a secondary layer of entitlement, which effectively guarantees up to 25% of your total loan amount.

This 25% guarantee is where county loan limits come into play—not as a hard cap on what you can borrow, but as a benchmark for calculating your remaining benefit. For 2025, these limits got a significant boost to keep pace with the housing market. The standard limit for most counties jumped to $806,500, while some high-cost areas can go as high as $1,209,750. You can explore the VA loan limits in your specific county to see the exact figures for your target area.

Let's walk through an example of calculating your borrowing power with remaining entitlement:

- Find the County Loan Limit: Let’s say the limit in your desired county is $800,000.

- Calculate the Max VA Guarantee: The VA will guarantee 25% of this, which comes out to $200,000. This is your total entitlement for that area.

- Determine Your Used Entitlement: Imagine you have an existing VA loan for $300,000. The entitlement used for that loan is 25% of its value, or $75,000.

- Calculate Your Remaining Entitlement: Now, just subtract the used amount from the maximum guarantee: $200,000 - $75,000 = $125,000. This is what you have left to work with.

- Find Your No-Down-Payment Limit: To find out how much house you can buy with $0 down, multiply your remaining entitlement by four. In this scenario, $125,000 x 4 = $500,000.

Just like that, you've figured out you can buy a second home for up to $500,000 with no money down, all while keeping your first property. For more information on how this benefit functions, you might be interested in our comprehensive guide on how the VA loan works.

Once you grasp this calculation, you're no longer just a borrower; you're a strategic homebuyer ready to make the most of this incredible, lifelong benefit.

Got Questions About VA Loan Eligibility? Let's Clear Things Up.

Even after you've got the basics down, it’s natural to have questions. The VA loan process has a lot of moving parts, and everyone's situation is a little different. Let's walk through some of the most common questions I hear from veterans and service members to give you the confidence you need to move forward.

One of the biggest anxieties I see revolves around credit. So many people I talk to are convinced that a few financial missteps in the past will completely shut them out of this benefit. But that's usually not the case.

Can I Still Get a VA Loan with Bad Credit?

Here's the deal: the VA itself doesn't have a magic credit score number you have to hit. The score requirements actually come from the private lenders who fund the loans, and most of them look for a score around 620.

But don't panic if your score is a little south of that. The VA loan is famous for its flexibility.

Lenders are trained to look at your whole financial picture, not just one three-digit number. A lower credit score can often be balanced out by other strong points, like a steady job, not too much other debt, and healthy residual income (that's the money you have left over each month after paying your major bills).

The best thing you can do is talk to a lender who really knows VA loans. They can look at your specific situation and give you a real game plan for strengthening your application. A "no" today doesn't have to be a "no" forever.

What if My COE Application Gets Denied?

Getting a denial on your Certificate of Eligibility (COE) can feel like hitting a brick wall, but it’s rarely the end of the road. More often than not, it's a paperwork problem that can be fixed. Your first move is to read the denial letter from the VA carefully—it will tell you exactly why you were denied.

Usually, it comes down to one of these things:

- Not enough service time: The VA’s records might be out of date or incomplete.

- A dishonorable discharge: This is generally the one thing that will disqualify you.

- Missing paperwork: You might have forgotten to include a specific form or proof of service.

If you know the denial was a mistake, you absolutely have the right to appeal. This might mean digging up your DD-214 or other service records to prove your history. Getting help from a Veteran Service Organization (VSO) can be a huge advantage here; they're experts at navigating the VA's appeal system. For a closer look at the documents and rules, our detailed guide on VA home loan requirements is a fantastic place to start.

Are Surviving Spouses Eligible for a VA Loan?

Yes, they are. This is a critical part of the VA loan benefit, designed to support the families of our fallen heroes. As a surviving spouse, you can qualify for this powerful homebuying tool if you haven't remarried and your spouse was a veteran who met one of these conditions:

- Died in service or from a service-connected disability.

- Was listed as Missing in Action (MIA) or was a Prisoner of War (POW).

- Passed away from non-service-related causes but was rated as totally disabled for a certain amount of time before their death.

The rules here are very specific. The most important step is to get your own Certificate of Eligibility to confirm you qualify. A lender who understands the nuances of this process can be your best ally in gathering the right documents, like the veteran's DD-214 and death certificate.

Can I Use My VA Loan Benefit More Than Once?

Absolutely! This is one of the best-kept secrets and most powerful features of the VA loan. Think of it as a lifelong benefit that you can use over and over again.

When you buy a home with a VA loan and then sell it later, paying off the loan completely, your full entitlement is restored. You're ready to go again on your next home, with $0 down.

What’s even better? You don't always have to sell the first house. If you get PCS orders, for example, you can often use your "remaining entitlement" to buy a home at your new duty station while keeping the first one as a rental property. Learning how to restore and reuse your VA eligibility loan is a fantastic strategy for building wealth over your lifetime.

Ready to see how your VA loan benefit can work for you? At Tiger Loans Inc, our mortgage experts live and breathe VA loans. We're here to guide you through every single step, from getting your COE to getting the keys to your new home. We’re committed to giving you the dedicated, personalized support you've earned.

Alex Chen

Alex Chen

Get in touch with a loan officer

Our dedicated loan officers are here to guide you through every step of the home buying process, ensuring you find the perfect mortgage solution tailored to your needs.

Options

Exercising Options

Selling

Quarterly estimates

Loans

New home

Stay always updated on insightful articles and guides.

Every Monday, you'll get an article or a guide that will help you be more present, focused and productive in your work and personal life.

.png)

.png)

.png)

.avif)

.avif)

.avif)

.png)

.png)

.png)

.avif)

.png)

.png)

.avif)

.png)

.avif)

.png)

.avif)

.avif)