VA Loan Pre-Approval vs. Pre-Qualification: Key Differences You Must Know

November 19, 2025

Learn the va loan pre-approval vs. pre-qualification: key differences to understand which step gives you an advantage in securing your home loan. Get informed today!

The biggest difference between a VA loan pre-qualification and a pre-approval comes down to one thing: verification. A pre-qualification is a quick estimate of what you might be able to borrow, based entirely on information you provide yourself. On the other hand, a pre-approval is a verified, lender-backed assessment of your actual purchasing power.

Think of it this way: a pre-qualification is like a casual chat about your finances, giving you a ballpark figure. A pre-approval is a full-on financial health check-up, complete with lab work. For a serious homebuyer, one is a rough guide, while the other is your golden ticket to making a competitive offer.

Your First Step in the VA Home Loan Journey

Starting the homebuying process is a huge step, and getting these initial stages right can make all the difference. Pre-qualification is the informal kickoff—usually just a quick conversation where you share estimates of your income, savings, and debts. It's a no-pressure way to get a feel for your budget without any major commitment.

Getting a VA loan pre-approval, however, is where things get serious. This is a formal application process where you'll need to submit real financial documents for the lender to scrutinize. We're talking pay stubs, W-2s, bank statements, tax returns, and your all-important Certificate of Eligibility (COE).

Quick Look Pre-Qualification vs Pre-Approval

Sometimes seeing the differences side-by-side makes it all click. Here’s a quick breakdown of how these two really stack up when you’re out there house hunting.

That distinction becomes crystal clear the moment you find a home you want to put an offer on. Sellers and their agents take pre-approval letters very seriously because it shows them you're a legitimate, financially vetted buyer. This instantly makes your offer more attractive and trustworthy.

A pre-qualification tells you where to start looking. A pre-approval gives you the power to actually buy.

So, which one is right for you? It really just depends on where you are in the process. If you're just kicking the tires and exploring what might be possible, a pre-qualification is a perfect, low-stakes first move. But once you’re ready to start touring homes and making offers, a pre-approval isn't just an advantage—it's essential.

To get the full picture of how to leverage your VA benefits from start to finish, be sure to check out this comprehensive Veterans Home Buying Guide.

What a VA Loan Pre-Qualification Really Means

Think of a VA loan pre-qualification as the first informal chat you have about buying a home. It’s that initial, low-stakes step you take when you're just starting to kick the tires on the idea, giving you a quick financial snapshot. It’s all about getting a ballpark figure of your borrowing power without any heavy lifting on your part.

The whole process is incredibly simple because it’s based on the financial picture you paint for the lender. They'll ask for some basic numbers—your income, what you owe on other debts, and your assets—and based on that conversation, they'll give you a rough estimate of what you might be able to borrow.

A Risk-Free First Look

One of the best things about getting pre-qualified is what it doesn't do to your credit. Lenders typically run a soft credit inquiry, which has zero impact on your credit score. This makes it a completely risk-free way to test the waters and see where you stand before you dive into a formal application.

This initial look gives you a rough roadmap for your house hunt. It helps you set a realistic budget and understand what price range you should even be looking at. But, and this is important, you have to remember what a pre-qualification isn't.

A VA loan pre-qualification is an estimate, not a promise. It provides a helpful starting point for your budget but does not represent a commitment from a lender to provide funding.

Essentially, pre-qualification answers the question, "What can I potentially afford?" It gives you the basic numbers to start browsing listings online and dreaming about your future home, all without the pressure of a full-blown loan application. For a deeper dive, our guide on the key differences between VA loan pre-approval vs. pre-qualification breaks down the entire journey.

The Speed of an Estimate

Because the process relies entirely on the information you provide—no deep dives into tax returns or pay stubs—it’s incredibly fast. In most cases, you can get your pre-qualification results within just one to three days.

This speed is a huge advantage early on. It lets you quickly adjust your expectations and start your home search with a much clearer, more informed perspective.

Key Characteristics of VA Pre-Qualification:

- Financial Basis: Relies entirely on your self-reported income, debt, and asset figures.

- Credit Impact: Involves a soft credit pull, which will not lower your credit score.

- Purpose: Best for early-stage budgeting and getting a general idea of your borrowing capacity.

- Market Power: Does not carry significant weight with sellers or real estate agents.

Securing a Powerful VA Loan Pre-Approval

While pre-qualification is a good starting point, a VA loan pre-approval is what truly separates the serious homebuyers from the casual window shoppers. This isn't just a ballpark estimate based on what you tell a lender; it's a rigorous, in-depth review of your verified financial standing. Think of it as the lender’s official stamp of approval, confirming they've done their homework and are confident in your ability to buy.

This changes everything. When you submit an offer with a pre-approval letter in hand, sellers see a buyer who is ready to go. It’s not just a piece of paper—it’s a conditional commitment from a financial institution. In a competitive market where multiple offers are common, this single document can be the very thing that makes your offer stand out from the rest.

The Documentation You Will Need

Unlike the informal chat for a pre-qualification, getting pre-approved means it’s time to get down to business with a formal application and a stack of paperwork. Your lender needs to see the complete picture of your financial health to accurately determine how much they're willing to lend you.

Be ready to gather and submit these key documents:

- Proof of Service: Your Certificate of Eligibility (COE) is non-negotiable. It’s the cornerstone that confirms you've earned your VA loan benefit.

- Income Verification: Get your last two years of W-2s, your most recent pay stubs, and full federal tax returns ready to go.

- Asset Statements: Lenders will want to see the last couple of months of statements for all of your checking and savings accounts.

- Credit History: You'll need to authorize a hard credit inquiry, which gives the lender a complete look at your credit report and FICO scores.

This comprehensive review removes all the guesswork. The result is a precise loan amount, giving you a firm, realistic budget for your house hunt. For a full breakdown of every document and step, check out our guide on navigating the VA loan pre-approval process for a deeper dive.

Maintaining Your Pre-Approval Status

Getting that pre-approval letter is a huge win, but it’s not a blank check with an unlimited timeline. It’s a powerful tool with an expiration date and specific conditions you need to uphold.

A pre-approval letter is your golden ticket into the competitive housing market. It tells sellers you are not just a dreamer but a buyer with verified financial backing, ready to complete a transaction.

Typically, a pre-approval is valid for 60 to 90 days. If your search takes longer, you’ll likely need to provide updated financial documents to renew it. Most importantly, you must keep your financial situation stable during this time. That means no big career changes, no new car loans, and no large, unexplained cash deposits. Any sudden moves could throw a wrench in the works and put your final loan approval at risk. By keeping your finances steady, you ensure your pre-approval remains the powerful asset you need it to be when you finally find the right home.

Comparing the Process and Market Impact

Understanding the textbook definitions is one thing, but seeing how VA loan pre-approval and pre-qualification play out in the real world is another entirely. Think of it this way: one is like a casual chat about your finances, while the other is a formal, in-depth financial review. That difference is what determines whether sellers and their agents see you as a serious contender or just another window shopper.

Getting a VA pre-qualification is usually quick and painless. You'll likely hop on a short phone call or fill out a simple online form, providing your best guess for income, debts, and assets. The lender doesn't verify any of it. Because of this, you can get a rough estimate of what you might be able to borrow in just a few minutes.

On the flip side, getting a VA pre-approval is a much more formal affair. This is where you roll up your sleeves and prove you're a solid borrower. You’ll be submitting real documents: W-2s, recent pay stubs, bank statements, and, of course, your Certificate of Eligibility (COE). It’s a genuine underwriting process, so it can take a few days to get the final word.

Financial Verification and Credit Impact

The biggest split between these two paths is how your financial information gets treated. With a pre-qualification, the lender essentially takes your word for it. But for a pre-approval, a loan officer combs through every single document to confirm you have the financial backbone to handle the mortgage.

This verification difference extends to your credit. A pre-qualification typically involves a soft credit inquiry, which is just a glance at your credit profile and has zero impact on your score. A pre-approval, however, requires a hard credit inquiry because you are officially applying for a loan. This can cause your credit score to dip slightly for a short time.

Pre-qualification helps you browse homes online. Pre-approval helps you win the home you want.

That simple statement really gets to the heart of it. A pre-qualification is a fantastic tool for your own planning and budgeting. But a pre-approval? That’s your golden ticket. It’s a powerful negotiating tool that shows sellers your offer is solid and backed by a lender's conditional commitment, making you a much more attractive buyer.

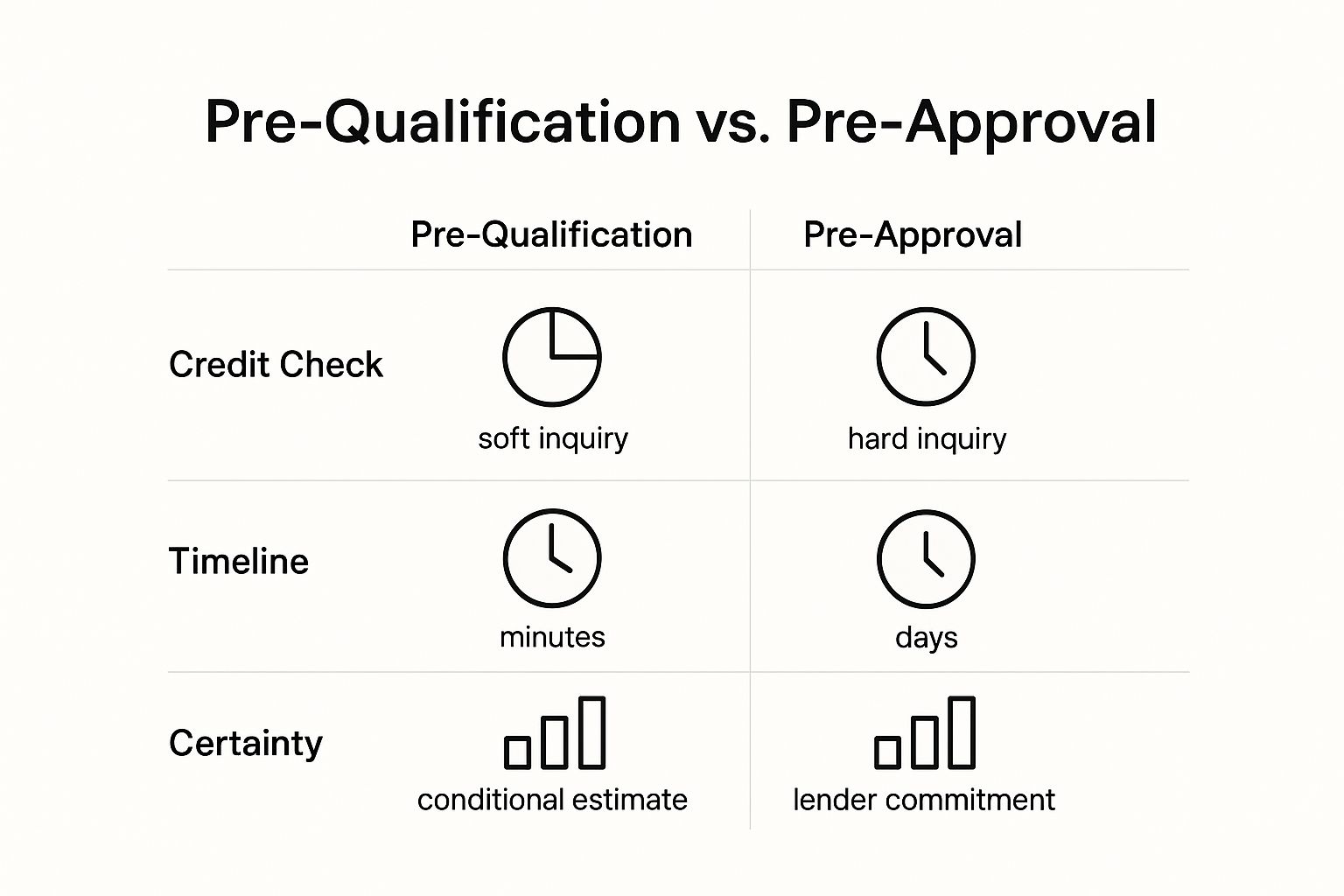

This infographic breaks down the essential differences in the process, from the credit check all the way to the level of certainty you walk away with.

As you can see, even though it takes more effort, the pre-approval process delivers a much higher degree of confidence and negotiating power.

The Application Experience Side-by-Side

To really drive the point home, let's look at what each process truly entails. This table offers a straightforward, side-by-side view of what separates getting pre-qualified from getting pre-approved for your VA loan.

Detailed Breakdown: Pre-Qualification vs. Pre-Approval

Here is a clear, practical comparison of the key differentiators between the two initial steps in the VA loan journey.

Ultimately, knowing the key differences between VA loan pre-approval and pre-qualification is what sets you up for success. One gets you ready for the house hunt; the other gives you the power to actually win the home you fall in love with. Choosing the right path at the right time is a strategic move that can shape your entire home-buying experience.

When to Choose Pre-Qualification vs. Pre-Approval

Deciding between a VA loan pre-qualification and a pre-approval is more than just paperwork. It’s a strategic move that needs to line up with your personal home-buying timeline. Understanding the real difference between them helps you pick the right tool for the job, and picking the right one at the right time can save you a world of stress.

Get it wrong, and you could miss out. A flimsy pre-qualification might get your offer ignored in a competitive market. On the other hand, jumping the gun on a pre-approval could start a 90-day clock ticking before you're even ready to start your search.

The Best Time for a VA Loan Pre-Qualification

Think of a pre-qualification as dipping your toe in the water. It’s the perfect first move when you’re just starting to think about buying a home and want a quick financial reality check without any real commitment.

A pre-qualification makes sense in these situations:

- You're Just Starting Out: If buying a home is still 6-12 months away, a pre-qualification is a great, no-pressure way to see where you stand.

- You Want to Set a Budget: It gives you a rough estimate of what you can afford, which helps you browse online listings in the right price range.

- You're Not Ready for a Hard Credit Inquiry: Because it only involves a soft credit pull, your credit score won’t be affected. It's a completely risk-free way to test the waters.

A pre-qualification is your private planning tool. It’s for you and you alone, helping you map out a plan before you ever step into the competitive real estate arena.

Pre-qualification gives you the knowledge to plan. Pre-approval gives you the power to make a winning offer. This distinction is everything when it comes to timing your next move.

For instance, a service member who is thinking about buying a home after their next promotion would get a lot of value from a quick pre-qualification. It helps them set a savings goal and get a feel for their budget without kicking off the formal loan process too soon.

When a VA Loan Pre-Approval Is Essential

When your house hunt gets serious—moving from "just looking" to "ready to buy"—it’s time to bring out the heavy artillery. A VA loan pre-approval isn't just nice to have; it's essential if you want to be seen as a serious buyer.

You absolutely need a pre-approval in these cases:

- You Are Ready to Make Offers: Most real estate agents won't even submit an offer for you without a pre-approval letter in hand.

- You Are in a Competitive Market: In a seller's market, an offer without a pre-approval is often dead on arrival. It’s the proof sellers need that you're financially vetted and ready to close the deal.

- You Have a Tight Timeline: Think about a military family on a tight Permanent Change of Station (PCS) schedule. They need to move fast. A pre-approval lets them make a strong, confident offer the second they find the right house, cutting out potential delays.

At the end of the day, a pre-approval changes the game. You go from being a window shopper to a buyer with real leverage. It sends a clear signal to sellers that you have the financial muscle to back up your offer, giving it the credibility it needs to get accepted.

Answering Your Top VA Loan Approval Questions

Walking the path to a VA loan can bring up a lot of questions. It's totally normal. Getting straight answers is the best way to build your confidence, avoid common headaches, and put yourself in a winning position when it's time to make an offer.

Let's dig into the questions I hear most often from veterans and service members about getting pre-approved for a VA loan and what that really means for their home search.

Can I Get a VA Loan Pre-Approval with a Lower Credit Score?

This is a big one, and the answer is more nuanced than a simple yes or no. The Department of Veterans Affairs itself doesn't actually set a minimum credit score. That's a common misconception. But, you're not borrowing from the VA; you're borrowing from a private lender who is backed by the VA.

Because of this, individual lenders set their own standards for risk. Most lenders draw the line somewhere around a 620 credit score. But that number isn't set in stone across the board. Some lenders who specialize in VA loans might have more wiggle room.

If your score is a bit shy of that mark, your best bet is to work on strengthening your credit before you apply for pre-approval. Focus on paying down high-balance credit cards, check your report for errors you can dispute, and keep a perfect record of on-time payments. A higher score doesn't just boost your approval odds—it unlocks better interest rates, saving you a lot of money over the life of the loan.

Does Pre-Approval Guarantee I Get the VA Loan?

A VA loan pre-approval is a game-changer, but it isn't a blank check or a final guarantee. It's better to think of it as a strong, conditional commitment from your lender. It means they've dug into your finances—your income, debt, and credit history—and have committed to lending you a certain amount of money as long as a few final conditions are met.

These conditions are the last hurdles before you get the keys:

- A Solid Property Appraisal: A VA-approved appraiser has to inspect the home. The appraisal value must be at least the loan amount, and the property has to pass the VA's Minimum Property Requirements (MPRs).

- A Clean Title Search: The lender will confirm the property has a clear title, meaning no one else has a claim to it and there are no outstanding liens.

- No Big Financial Changes: Your financial situation needs to stay consistent from pre-approval to closing day. That means no new car loans, no maxing out credit cards, and no changing jobs without talking to your lender first.

A pre-approval is what makes your offer stand out and gets your foot in the door. Fulfilling these final conditions is what gets you across the finish line.

How Many Lenders Should I Get Pre-Approved With?

Shopping around for a mortgage is one of the smartest things you can do. While getting a bunch of pre-qualifications won't hurt your credit (they're just soft pulls), you need to be more deliberate with pre-approvals because they trigger a hard credit inquiry.

So, what's the sweet spot? Aim to get pre-approved with two to three lenders you feel good about. The trick is to submit all of your applications within a short period. Credit scoring models like FICO and VantageScore understand that people shop for the best rates on big loans, so they typically bundle multiple mortgage inquiries made within a 14- to 45-day window and treat them as a single event.

This approach lets you compare official Loan Estimates and lock in the best interest rate and terms, all without trashing your credit score. Knowing your numbers is crucial, and you can learn more about VA home loan income requirements to feel fully prepared for those lender conversations.

Ready to turn your homeownership dream into a reality? The experts at Tiger Loans Inc are here to guide you through every step of the VA loan process. Get your free pre-approval today!

Alex Chen

Alex Chen

Get in touch with a loan officer

Our dedicated loan officers are here to guide you through every step of the home buying process, ensuring you find the perfect mortgage solution tailored to your needs.

Options

Exercising Options

Selling

Quarterly estimates

Loans

New home

Stay always updated on insightful articles and guides.

Every Monday, you'll get an article or a guide that will help you be more present, focused and productive in your work and personal life.

.png)

.png)

.png)

.avif)

.avif)

.avif)

.png)

.png)

.png)

.avif)

.png)

.png)

.avif)

.png)

.avif)

.png)

.avif)

.avif)