VA Home Loan Income Requirements Explained

November 19, 2025

Unlock your dream home with our guide to VA home loan income requirements. We break down DTI, residual income, and what lenders are really looking for.

Worried you need a six-figure salary to even think about a VA loan? Let's clear that up right now. The truth is, when it comes to VA home loan income requirements, there’s no magic number you have to hit. The VA is far more interested in your overall financial picture and making sure you can actually afford your new home without being stretched thin.

Your Path to Homeownership With a VA Loan

Unlike a lot of conventional loans that can get fixated on a single income figure, the VA loan program takes a much more holistic and practical look at your finances. Think of it less like a rigid test you have to pass and more like a common-sense checkup to gauge your readiness for homeownership. The whole point is to set you up for success, not to put up roadblocks.

To do this, lenders zero in on two core pillars to decide if you can comfortably handle a mortgage payment month after month. These concepts are the foundation of your eligibility and are way more important than what your gross annual salary looks like on paper.

The Two Pillars of Affordability

The VA’s approach is built on a simple, powerful idea: you need enough money to not only cover your mortgage but also to live your life. This is where two key financial metrics come into play.

- Debt-to-Income (DTI) Ratio: This is a simple percentage that shows how much of your monthly income is already spoken for by existing debts.

- Residual Income: This is the cash you have left over each month after you’ve paid the new mortgage and all your other regular bills.

So, while there are no official income limits for a VA loan, the real requirement is demonstrating a steady, reliable income that can cover your monthly housing payment and other living expenses. Lenders do look at your DTI, and while the VA doesn't set a hard-and-fast rule, most lenders like to see a DTI of 41% or less. You can get more insights on what income counts at VeteransUnited.com.

The VA loan program was designed from the ground up to be one of the best homeownership tools for veterans and service members. Its flexible income guidelines are all about helping you build a future, not just approving a loan.

Ultimately, this two-pronged system makes the VA loan incredibly flexible. It’s a genuine pathway to owning a home, not an obstacle course designed to trip you up.

What Counts as Qualifying Income for a VA Loan?

When a VA lender looks at your income, they’re not just glancing at your latest pay stub. They're trying to understand your complete financial story. The three words they care about most are stable, reliable, and likely to continue. This perspective is a huge advantage for veterans, as it recognizes that your financial life might not fit into a neat, 9-to-5 box.

Think of it this way: your income qualification isn't just about one single number. It's a mosaic built from all your verified financial resources. Lenders are trained to look at this bigger picture, piecing together everything from your base pay to other consistent earnings to build the strongest possible case for your approval.

Accepted Income Sources

The good news is that the VA has a refreshingly broad view of what counts as income. As long as you can document it and it's reasonably expected to stick around for the next three years, it's probably fair game.

Here are some of the most common types of income lenders will happily count:

- Active-Duty Pay: This is more than just your base salary. It also includes entitlements like your Basic Allowance for Housing (BAH), hazard pay, and any specialty pay you receive.

- Civilian Employment: Your standard full-time or part-time job is a given. If you consistently work overtime or earn bonuses, that can often be included too, provided you can show a solid history.

- Self-Employment Earnings: For the entrepreneurs and freelancers out there, lenders will want to see proof of a steady business. Typically, this means having at least two years of tax returns to show a reliable income stream.

- Retirement and Disability Income: Pensions, Social Security payments, and both military retirement and VA disability benefits are seen as highly stable and dependable sources.

- Other Income: Money from other sources like alimony, child support, or even income from investment dividends or a rental property can also be counted if it's well-documented.

At the end of the day, the lender's goal is to see that your financial story adds up. They aren't just checking boxes; they're making sure your combined income creates a solid foundation for you to comfortably own a home.

Proving Your Income Is Stable

Showing that your income is reliable is where the rubber meets the road. To get approved, you need to prove your income is sufficient, stable, and will continue. Lenders will usually ask for documents that paint a clear picture of a consistent two-year employment and income history, which is most often done with W-2s and tax returns. You can discover more insights about these documentation standards on Military.com.

Don't panic if you have a few gaps in your employment history. Just be ready to explain them. The VA is often very understanding of breaks in employment, especially if they were for pursuing education or specialized training that ultimately boosts your long-term career prospects.

By pulling together a complete and well-documented financial profile, you dramatically increase your chances of hearing "you're approved." To learn how this fits into the overall process, you might want to read more about understanding the income requirements for a VA loan in 2025.

Understanding Your Debt-To-Income Ratio

When a lender looks at your VA loan application, they’re trying to answer one big question: can you comfortably afford this new mortgage payment? One of the most important tools they use to figure this out is your debt-to-income (DTI) ratio.

Think of it as a quick financial health check. It’s a simple percentage that compares how much money you earn each month (your income) to how much you owe to creditors (your debt). A lower DTI tells a lender you have a healthy amount of breathing room in your budget, making you a less risky borrower.

How To Figure Out Your DTI

Getting your DTI number is pretty simple. First, you'll add up all your monthly debt payments. Then, you divide that number by your gross monthly income (what you make before taxes).

If you want a deeper dive, our comprehensive guide on how to calculate your debt-to-income ratio breaks it down step-by-step.

So, what debts count? Generally, it's any recurring payment that shows up on your credit report, plus your new estimated housing cost.

- Car loans

- Student loan payments

- Minimum payments on your credit cards

- Personal loans

- And, of course, your future mortgage payment (including taxes and insurance)

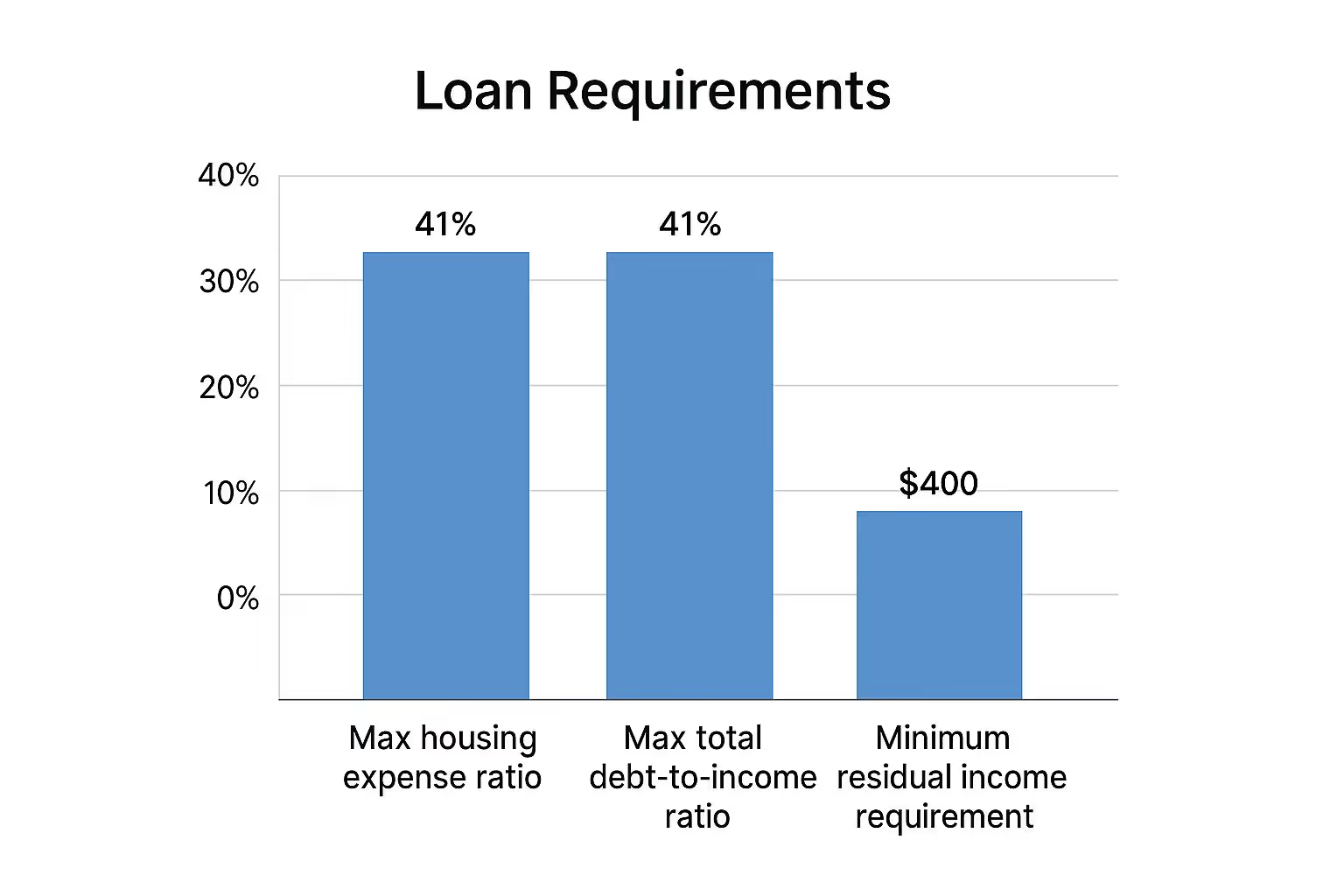

The 41% Guideline Everyone Talks About

You'll hear the number 41% thrown around a lot in the VA loan world. While the VA doesn't have a hard, official DTI limit, most lenders use 41% as a benchmark. It’s a guideline that suggests you're in a strong position to get approved.

For example, if you earn $5,000 a month before taxes, your total monthly debts (including your new mortgage) should ideally be under $2,050 to hit that 41% mark.

Don’t panic if your DTI is over 41%. This number is a guideline, not a rule set in stone. The VA loan program is famous for its flexibility.

This is where the VA loan truly shines. A high DTI isn't an automatic "no." Instead, lenders will look for what we call compensating factors. These are other positive aspects of your financial picture that help balance out the risk. Things like a great credit score, a healthy savings account, or a strong residual income can make all the difference and help you get across the finish line, even with a DTI above 41%.

The VA Loan's "Secret Weapon": Residual Income

While your Debt-to-Income (DTI) ratio is a big piece of the puzzle, it doesn’t give lenders the full picture. This is where the VA loan program introduces its most powerful and sensible financial metric: residual income. It's a cornerstone of the VA home loan income requirements and, frankly, what makes this benefit so different from almost any other mortgage out there.

Think of it this way: DTI is a backward-looking snapshot of your debts versus your income. Residual income, on the other hand, is a forward-looking projection of your actual cash flow. The VA isn't just concerned with the bills you already have; they want to know you'll have enough money left over each month to comfortably handle life after the mortgage is in place. This "leftover" money is what covers things like gas for your car, groceries, utilities, and all the other day-to-day costs of living.

More Than a Number—It's a Financial Safety Net

The VA’s emphasis on residual income is a testament to their commitment to your long-term success. The goal isn’t just to get you the keys to a house; it’s to ensure you can afford to live in it without constant financial stress. It’s a far more human and realistic way to gauge affordability than simply relying on a cold, hard DTI percentage.

A strong residual income is often the key that unlocks an approval, especially for borrowers with a DTI ratio that might be higher than the typical 41% guideline. It’s powerful proof that you can manage the real-world costs of homeownership.

This practical approach is a major reason why VA loans consistently have one of the lowest foreclosure rates on the market. The entire program is built to set you up for success, helping you build stability and wealth for your family.

This infographic breaks down the key financial benchmarks a VA lender will be looking at.

As you can see, residual income isn't just a suggestion; it's a distinct requirement that complements your DTI to create a holistic view of your financial readiness.

How Much Residual Income Do You Need?

So, what's the magic number? The VA sets minimum residual income thresholds, but they aren't one-size-fits-all. The figure is carefully tailored to your life, which is what makes the requirement so fair and effective.

The amount you'll need depends on two key factors:

- Your Family Size: It makes sense, right? A larger family is going to have higher daily living expenses, so the requirement goes up for each person in your household.

- Your Geographic Region: The cost of living isn't the same in Boise as it is in Boston. The VA accounts for this by setting different targets for the Northeast, Midwest, South, and West.

This table provides a glimpse into how these minimums can vary.

Sample Monthly Residual Income Requirements By Region

For instance, a single veteran in a lower-cost area in the South has a much different target than a family of four living in a high-cost city out West. Your lender will use an official VA chart to pinpoint the exact figure for your situation, ensuring your new home payment is truly manageable. It's just one more way the VA loan is designed to be a blessing, not a burden.

How Real Veterans Get Approved

Alright, let's move away from the textbook definitions and see how this all plays out in the real world. The numbers and rules behind VA home loan income requirements really click when you see them in action. Walking through a few common scenarios shows how veterans with very different financial pictures can all arrive at the same amazing destination: homeownership.

These stories bring the calculations to life. They're designed to help you see where you might fit in and give you a clearer picture of your own path forward.

Scenario 1: The High DTI, High Residual Income Veteran

First, meet Sergeant Miller, a single veteran living in a Midwest city. She’s doing well, bringing in a gross monthly income of $6,000. Her existing monthly debts, like a car loan and student loans, add up to $1,500. The home she has her eye on comes with an estimated mortgage payment of $1,900.

- Total Monthly Debt: $1,500 (existing) + $1,900 (mortgage) = $3,400

- DTI Calculation: ($3,400 / $6,000) = 56.7%

On paper, that 56.7% DTI is way over the 41% guideline. With most other loans, that would be an immediate red flag. But with a VA loan, the underwriter looks deeper. After her $3,400 in total monthly payments are covered, Sergeant Miller still has $2,600 left over. The VA's minimum residual income for a single person in her region is just $579.

Because her leftover income is over 4.5 times the required minimum, the lender can clearly see she can handle the mortgage payment without financial stress. This powerful compensating factor is exactly what gets her loan approved.

Scenario 2: The Self-Employed Veteran

Now, let's look at Petty Officer Davis. After leaving the service, he launched a successful freelance business and now wants to buy a home in the South for his family. For any entrepreneur, proving your income is the biggest hurdle, since lenders are trained to look for steady paychecks.

To show his income is stable and reliable, Davis provides the right paperwork:

- Two full years of complete business and personal tax returns.

- A current, year-to-date profit and loss statement (P&L) to show his business is still thriving.

- Recent business bank statements that demonstrate consistent cash flow.

His averaged monthly income over the last two years comes out to $7,500. Better yet, his family has kept their debts low, giving him a DTI of just 28%, even with the new mortgage payment. By providing a clear, documented history of his self-employment income, he sails through the VA's requirements. Knowing what documents to gather is half the battle; for a full checklist, take a look at our guide on the essential VA home loan requirements.

Scenario 3: The Modest Income, Low Debt Veteran

Finally, let’s consider Corporal Chen. He has a solid, dependable job that earns him $4,200 per month. He’s been smart with his money—he has no car payment and no credit card debt. His only monthly obligation is a small $150 student loan payment. The mortgage for his target home is $1,600.

- Total Monthly Debt: $150 (student loan) + $1,600 (mortgage) = $1,750

- DTI Calculation: ($1,750 / $4,200) = 41.6%

His DTI is perfectly in line with the guideline, and his residual income of $2,450 is way more than his regional minimum. Corporal Chen’s story is a fantastic example that you don’t need a six-figure salary to buy a home. By focusing on keeping his debts low, he demonstrated incredible financial discipline, which made his path to a VA loan approval smooth and simple.

Common VA Loan Income Myths Debunked

When you're trying to buy a home, the last thing you need is bad information. Unfortunately, when it comes to VA home loan income requirements, there are a lot of myths and outdated ideas floating around that can cause serious stress and make you second-guess your options.

It's time to set the record straight. The truth is, the VA loan was specifically created to be one of the most accessible and helpful home financing tools for our nation's service members. Once you understand the facts, you can move forward with real confidence.

Myth 1: The VA Has a Secret Minimum Income Level

This is probably the most common myth I hear, and it's completely false. The VA itself does not have a secret income chart or a minimum salary you must earn to qualify. It just doesn't exist.

Instead, lenders focus on your real-world ability to handle the monthly mortgage payment. They look at your debt-to-income ratio and, most importantly, your residual income. This is about making sure the loan is a responsible and sustainable fit for your life, not about hitting some arbitrary income target.

The VA’s goal is to prevent financial strain on veterans, not to create roadblocks with a magic income number. It all comes down to affordability, which is measured by your actual cash flow—the money you have left after your bills are paid.

Myth 2: You Cannot Get a Loan If You Are Self-Employed

Absolutely untrue. While it’s true that qualifying as a self-employed veteran takes a bit more paperwork than if you had a W-2 job, it’s a path many veteran entrepreneurs successfully take every year.

As long as you can document a steady and reliable income stream—usually with a solid two-year history shown on your tax returns—you are very much in the game for a VA loan. Don't let your entrepreneurial spirit stop you from pursuing homeownership.

Myth 3: You Need Perfect Credit to Qualify

While great credit is always a plus, the VA loan is famous for its flexible and forgiving credit standards. The VA doesn't actually set a minimum credit score.

Individual lenders will have their own credit score requirements, but they are often much lower than what you'd need for a conventional loan. More importantly, strong residual income can often help balance out a credit score that has a few dings and dents, opening the door to homeownership when you might have thought it was closed.

Your Top Questions About VA Loan Income Answered

Even after getting a handle on the basics, you probably still have a few specific questions bouncing around your head about VA home loan income requirements. It's completely normal. Let's walk through some of the most common ones so you can feel confident about where you stand.

Can My Spouse's Income Help Me Qualify?

You bet it can. Whether your spouse is a veteran or a civilian, lenders can absolutely count their income toward your qualification. Bringing your incomes together can make a huge difference, often boosting your borrowing power by strengthening both your DTI and residual income numbers.

There's just one little catch if your spouse isn't a veteran. In that case, the VA's guarantee only applies to your half of the loan. This might mean you'll need a small down payment, but it’s still a fantastic strategy to qualify for the home you really want.

How Do Lenders Look at Part-Time or Commission-Based Pay?

When it comes to income, lenders are all about stability and reliability. If you have a part-time job, earn commissions, or get regular overtime, the magic number is usually two years. You'll need to show a consistent track record of earning that money for at least that long.

Think of it from the lender's perspective. The two-year history proves this isn't just a temporary boost but a dependable part of your financial life they can count on continuing.

Do I Really Need to Have Money in Savings?

The VA loan's zero-down-payment feature is legendary, but that doesn't mean you should walk in with an empty bank account. While there isn't a strict, mandatory savings amount, having some cash reserves is a very smart move. Lenders want to see you can comfortably cover closing costs and have a buffer for a few mortgage payments.

This financial safety net is what we call a "compensating factor." It shows you’re truly prepared for the responsibilities of owning a home and can be a game-changer, especially if your DTI is a bit higher than ideal.

Ready to put your numbers to the test? The team at Tiger Loans Inc lives and breathes this stuff. We can give you a personalized look at your income situation and walk you through the entire VA loan process. Take the first step toward your new home by visiting us at https://www.tigerloans.com today.

Alex Chen

Alex Chen

Get in touch with a loan officer

Our dedicated loan officers are here to guide you through every step of the home buying process, ensuring you find the perfect mortgage solution tailored to your needs.

Options

Exercising Options

Selling

Quarterly estimates

Loans

New home

Stay always updated on insightful articles and guides.

Every Monday, you'll get an article or a guide that will help you be more present, focused and productive in your work and personal life.

.png)

.png)

.png)

.avif)

.avif)

.avif)

.png)

.png)

.png)

.avif)

.png)

.png)

.avif)

.png)

.avif)

.png)

.avif)

.avif)