What Is a USDA Loan? Your Guide to Zero-Down Mortgages

November 19, 2025

Wondering what is a USDA loan? This guide explains how this government-backed mortgage opens the door to homeownership with zero down payment in rural areas.

So, what exactly is a USDA loan? Think of it as a key to unlocking homeownership, specifically designed for families who want to buy in less populated areas. It’s a mortgage backed by the U.S. Department of Agriculture that lets you buy a home with absolutely zero down payment.

That’s right—it helps you sidestep the biggest financial hurdle most aspiring homeowners face.

Your Path to Homeownership With a USDA Loan

Picture yourself holding the keys to your dream home without having to save for years just to cover the down payment. For many people, that feels like a fantasy, but the USDA loan program makes it a genuine possibility.

The program was created with a straightforward mission: to build up America's rural and suburban communities by making it easier for people to buy homes there. By encouraging homeownership, it helps stimulate local economies and improve the quality of life outside of major cities.

Officially called USDA Rural Development loans, these mortgages have been helping families plant their roots since 1992. While people often refer to them as one thing, the program actually has a few different branches, but the one most people use is the Guaranteed Loan. This is where a private lender like a bank or mortgage company issues the loan, and the USDA guarantees it, reducing the lender's risk.

To give you a clearer picture right from the start, here’s a quick rundown of what makes a USDA loan unique.

USDA Loan Features at a Glance

Feature Description Down Payment 0% down payment required. You can finance 100% of the home's value. Geographic Area Homes must be in a USDA-designated rural or suburban area. Income Limits Borrowers must meet specific income eligibility requirements, which vary by region. Mortgage Insurance Requires an upfront and annual guarantee fee, which is typically lower than PMI. Credit Score Lenders often look for a score of 640 or higher, but requirements can be flexible. Loan Purpose For purchasing a primary residence only, not for investment properties or vacation homes.

What This Guide Covers

Mortgage talk can get confusing fast, but I've designed this guide to be your clear and simple roadmap. We're going to break down everything you need to know about USDA loans and how they can work for you.

Here’s a sneak peek at what’s ahead:

- Eligibility Deep Dive: We'll get into the nitty-gritty of who qualifies based on income, credit, and, most importantly, where the property is located.

- Key Benefits Explained: Find out how features like 100% financing and great interest rates can literally save you thousands of dollars.

- Loan Comparisons: I’ll show you a simple side-by-side of how USDA loans measure up against FHA and conventional mortgages.

- Application Roadmap: You'll get a step-by-step walkthrough of the entire process, from getting pre-approved to finally closing on your new home.

The real goal of a USDA loan is to break down financial barriers for regular people in specific parts of the country. It’s not just about getting you into a house; it’s about investing in communities and helping families build a stable future.

By the time you're done reading, you’ll feel confident enough to decide if this is the right move for you. Ready to start your journey? Let's dive in. If you want to get a head start, you can explore our dedicated resources at https://www.tigerloans.com/landing/usda-loans anytime.

Do You Qualify for a USDA Loan?

Alright, you've seen the incredible benefits of a USDA loan. Now for the million-dollar question: can you actually get one? It's a common stumbling block. Many homebuyers hear "USDA" and immediately think of farming or assume the rules are way too strict. But I'm here to tell you, the reality is much more welcoming.

Getting the green light for a USDA loan really comes down to three key things: your household's income, your credit background, and—most importantly—where the house is located. Let's break these down one by one so you can get a clear picture of where you stand.

Understanding the Income Requirements

First up, let's talk money. This program is built to help low-to-moderate-income families, but what the USDA considers "low-to-moderate" might surprise you. There isn't a single, nationwide income cap. Instead, the limits are tailored to the cost of living in your specific area and how many people are in your household.

The USDA looks at the total adjusted gross income for your entire household. That’s a crucial detail—it includes the income of every adult who will be living in the home, not just the names on the loan paperwork. This combined income has to be under 115% of the median household income for your county.

This local approach makes a huge difference. For example, the income limit for a family of four could be $110,650 in one part of the country but jump to over $140,000 in a pricier market. The only way to know for sure is to look up your specific area on the official USDA income limits page.

What Credit Score Do You Need?

Next, let's look at your credit. You absolutely do not need a perfect score to get a USDA loan. Lenders just want to see a solid track record of you paying your bills on time.

For most lenders working with USDA Guaranteed Loans, a credit score of 640 is the magic number. Hitting that mark usually gets you on the fast track for an automated, streamlined approval.

But what if your score is a little south of 640? Don't panic. This isn't necessarily a deal-breaker. Lenders have the ability to manually underwrite your loan, which means a real person will take a closer look at your whole financial picture. They'll look for other strengths, or "compensating factors," like:

- A low debt-to-income (DTI) ratio, showing you aren't overextended.

- A consistent job history that proves you have reliable income.

- Healthy savings or other assets, even if you aren't using them for the down payment.

And for USDA Direct Loans—the ones aimed at very low-income families—the credit guidelines are even more forgiving. The main focus is simply on your ability and commitment to repaying the loan.

Key Takeaway: You don't need a flawless financial record. The USDA program is designed to be accessible, and lenders are trained to look beyond a single number to see your overall financial stability.

Finding an Eligible Property Location

Finally, we get to the one requirement that makes a USDA loan truly unique: the property's location. The home has to be in an area the USDA designates as "rural." This is where the biggest myth about these loans comes from.

When you hear "rural," you're probably picturing a farmhouse surrounded by miles of cornfields. While those homes certainly qualify, the USDA's definition is way broader. It covers countless small towns, suburbs, and communities just outside of major city limits. In fact, a mind-boggling 97% of the U.S. landmass falls into a USDA-eligible zone.

Your perfect home might be much closer to everything you need than you think. The guesswork is completely gone.

The USDA has a fantastic tool to help you out: the Property Eligibility Map. Just pop in the address of any home you're considering, and it will tell you instantly if it qualifies. This map is your best friend in the home search, empowering you to zero in on areas where you can use this amazing zero-down loan.

The Real Benefits of a USDA Home Loan

So, you know the basics of what a USDA loan is and who it's for. But let's get to the good stuff—why this loan is such a big deal for so many homebuyers. These aren't just minor perks; they're powerful advantages that can completely change the game, turning the dream of owning a home into a reality.

Think of a USDA loan as more than just a mortgage. For many people, it's the key that unlocks the door to homeownership years sooner than they ever thought possible. It's often the difference between signing another lease and starting to build your own wealth.

The Ultimate Advantage: Zero Down Payment

Let's start with the headline feature, the one that gets everyone's attention: 100% financing. That’s right. With a USDA loan, you can buy a home with absolutely no money down. This single benefit smashes the biggest wall that stands between most people and their first home.

Saving up a down payment is a long, hard slog. You're trying to put money aside while juggling rent, car payments, and everything else life throws at you. A conventional loan might demand 5%, 10%, or even 20% down—we're talking tens of thousands of dollars. The USDA loan lets you skip that monumental hurdle entirely.

What this really means is you can stop paying your landlord's mortgage and start building your own equity, all without having to drain your life savings just to get the keys.

Highly Competitive Interest Rates

Here’s another huge plus: USDA loans often come with some of the best interest rates you can find. How? It's simple, really. The U.S. government guarantees a slice of the loan for the lender, which takes a lot of the risk off their plate.

Because the loan is less risky for them, lenders are willing to pass those savings on to you in the form of a lower interest rate.

A small dip in your interest rate might not sound like much, but over the 30-year life of a mortgage, it adds up to a mountain of savings. We're talking about tens of thousands of dollars in interest you won't have to pay.

Just to give you an idea, some specialized USDA direct loans offer incredibly low rates. As of January 2025, rates for certain direct farm loans can be as low as 1.625%, and for very low-income residential buyers, USDA Direct Loans can have rates as low as 1%. You can explore more about these incredible USDA lending rates to see just how much of an impact this can make.

This government backing acts like a safety net for lenders, giving them the confidence to offer you better borrowing terms. You get a more affordable mortgage, and the lender gets a secure investment.

Lower Mortgage Insurance Costs

If you’ve looked into other loans with small down payments, you've probably run into PMI, or Private Mortgage Insurance. It's a hefty fee tacked onto conventional loans when you put down less than 20%. FHA loans have a similar charge that's often even more expensive.

USDA loans do things differently—and more affordably. Instead of PMI, they have something called a "Guarantee Fee." It works in two parts:

- An Upfront Fee: This is a small percentage of your loan amount. But here's the best part: you can almost always roll this fee right into your mortgage. That means you don’t have to cough up extra cash for it at the closing table.

- An Annual Fee: This is paid in small increments with your monthly mortgage payment. Crucially, this fee is almost always significantly lower than what you'd pay in PMI on a conventional loan or MIP on an FHA loan.

This more affordable structure is a huge win for your monthly budget. It keeps your payment lower, which means more money in your pocket for savings, emergencies, or just living your life.

How Do USDA Loans Stack Up Against FHA and Conventional Mortgages?

Choosing the right mortgage can feel overwhelming. You've got USDA, FHA, and conventional loans all vying for your attention, and it's easy to get lost in the financial jargon. But let's cut through the noise.

Think of it this way: each of these loans is a different tool designed for a specific job. Your goal is to find the one that fits your unique situation. We'll break them down by what really matters—down payments, credit scores, and the long-term costs you'll actually pay.

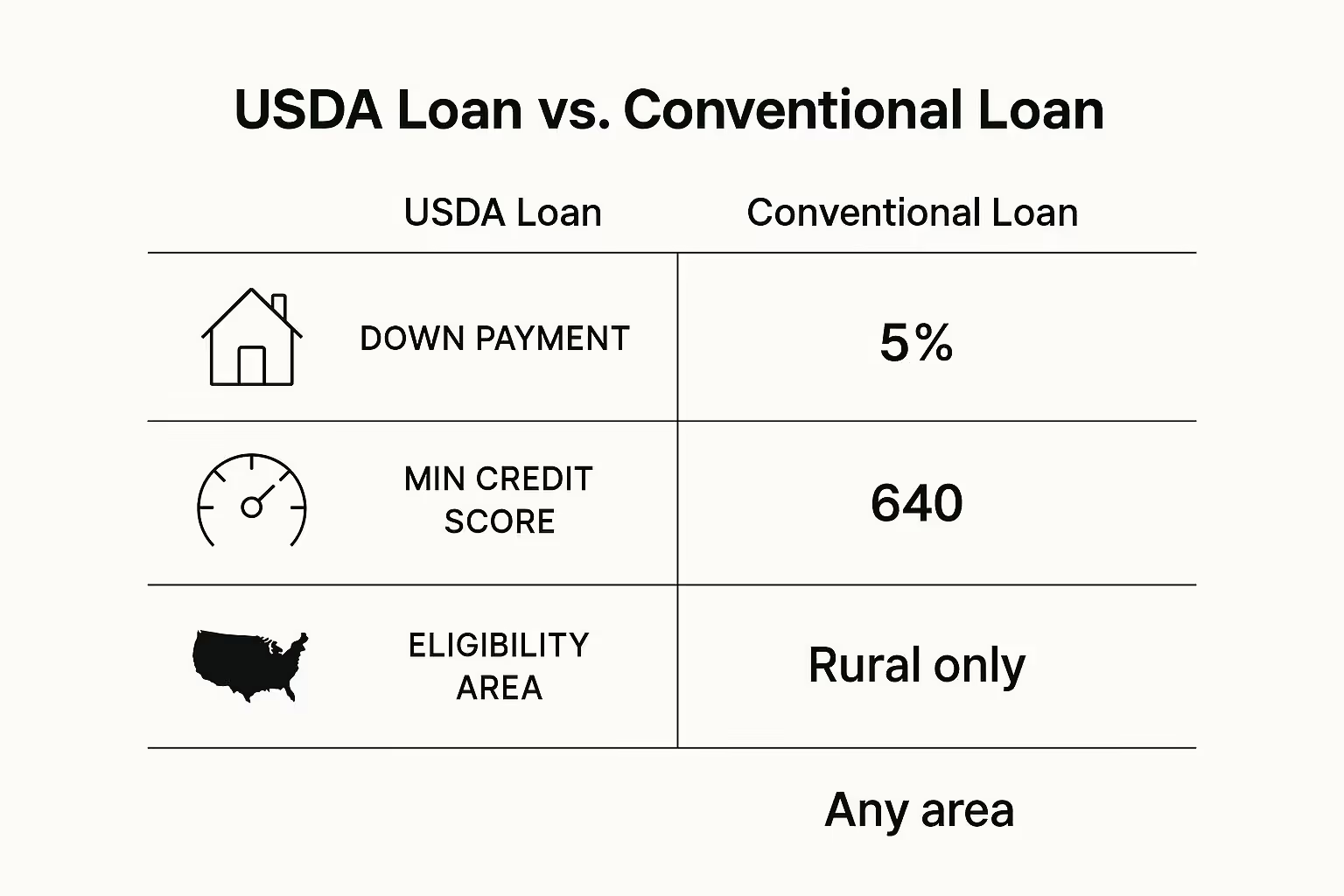

The Down Payment Showdown

For most aspiring homeowners, the biggest roadblock isn't finding the right house; it's saving up for the down payment. This is precisely where the USDA loan blows the competition out of the water.

- USDA Loan: Requires 0% down. That’s the big one. You can finance the entire home price without spending years scraping together a down payment.

- FHA Loan: Asks for a minimum of 3.5% down. That's still accessible, but on a $300,000 home, it's a check for $10,500.

- Conventional Loan: The gold standard is 20% down to avoid mortgage insurance. While some programs let you in the door with as little as 3% to 5%, you'll pay for it in other ways.

Being able to buy a home with nothing out of pocket is a massive advantage, putting the dream of homeownership within reach for many families far sooner than they thought possible.

This visual gives you a quick snapshot of how a USDA loan stands apart by removing the down payment barrier, though it does come with its own geographic rules.

Credit Score and Financial Requirements

Okay, so you've cleared the down payment hurdle. Next up: your credit score. Lenders use this three-digit number to figure out how risky you are, and each loan program plays by different rules.

The good news? You don't need a flawless credit history to qualify for a government-backed mortgage.

- USDA Loan: Most lenders are looking for a credit score of at least 640. Hitting this number usually means you'll breeze through an automated approval system. If your score is a little lower, a good lender might still work with you if you have other financial strengths, like a stable job or savings.

- FHA Loan: This is the most forgiving of the bunch. The FHA program officially accepts scores as low as 580 (with 3.5% down).

- Conventional Loan: These are a bit more sensitive to credit. You'll typically need a 620 just to get in the door, and if you want the best interest rates, you'll need a score north of 700.

If you're weighing the two most common options, you can see our full breakdown of a conventional loan vs FHA mortgage to help you decide.

The True Cost of Mortgage Insurance

When you put less than 20% down, lenders require you to pay mortgage insurance. It’s their safety net in case you can't make your payments. But what it's called, how much it costs, and how long you have to pay it varies wildly between loan types.

Don't just gloss over this part. The type of mortgage insurance you have directly impacts your monthly payment and how much you'll pay over the entire life of your loan. It's a huge deal.

A USDA loan calls its version a "Guarantee Fee," and it's almost always cheaper than the alternatives. It comes in two pieces: a small upfront fee that gets rolled into your loan balance (so you don't pay it out of pocket) and a very low annual fee that's broken up and added to your monthly payments.

FHA loans have a Mortgage Insurance Premium (MIP). Like the USDA's fee, it has an upfront portion and a monthly one. The catch? The monthly premium is usually higher, and for most borrowers, you pay it for the entire life of the loan.

Conventional loans use Private Mortgage Insurance (PMI). It can be pricey, but it has one killer feature: once you have 20% equity in your home, you can request to have it removed.

USDA vs FHA vs Conventional Loan Comparison

To make things even clearer, here’s a side-by-side look at the three main loan types. Seeing the details in one place can really help you pinpoint the best fit for your budget and goals.

FeatureUSDA LoanFHA LoanConventional LoanMinimum Down Payment0%3.5%3% - 20%Minimum Credit Score640 (typically)580620Property LocationMust be in an eligible rural areaAnywhereAnywhereIncome LimitsYes, based on household size and locationNoNoMortgage InsuranceGuarantee Fee (Upfront & Annual)MIP (Upfront & for loan life)PMI (canceled at 20% equity)Best ForLow-to-moderate income buyers in rural/suburban areasBuyers with lower credit scores or smaller down paymentsBuyers with strong credit and a sizable down payment

Looking at this chart, you can see the USDA loan carves out a fantastic niche. It offers a lower-cost mortgage insurance than an FHA loan while completely eliminating the down payment needed to avoid PMI on a conventional loan. By weighing these pros and cons, you can move forward with confidence, knowing you’ve chosen the mortgage that truly works for you.

Your Step-by-Step Guide to the USDA Loan Process

So, you're sold on the incredible benefits of a USDA loan. Now you’re probably asking, "What does it actually take to get one?" The path from application to getting those house keys might feel a bit mysterious, but it’s more straightforward than you think.

Let's break down the entire journey into a simple, step-by-step roadmap. Knowing what’s coming will help you navigate the process with confidence, not confusion.

Step 1: Find a USDA-Approved Lender

Your first step isn't house hunting—it's finding the right partner for the journey. Not every lender on the block handles USDA loans; they have their own unique set of rules and quirks. You’ll want to team up with a USDA-approved lender who lives and breathes this program.

Think of them as your expert guide. They know the shortcuts, the potential pitfalls, and exactly what it takes to get your application smoothly across the finish line. Starting with an expert will save you a world of headaches down the road.

Step 2: Gather Your Docs and Get Pre-Approved

With a great lender on your team, it’s time for a crucial milestone: pre-approval. This is the step that proves to sellers you’re a serious, qualified buyer. To get there, your lender needs to get a full picture of your finances.

You’ll need to pull together a few key documents:

- Proof of Income: Typically your last two years of W-2s and recent pay stubs.

- Asset Information: Bank statements are needed to show you have funds for closing costs or reserves.

- Debt Information: A list of any monthly payments you have, like a car loan or student debt.

- Personal Identification: Your driver's license and Social Security number.

Your lender will take this info, review your credit, and tell you exactly how much home you can comfortably afford. That pre-approval letter is your golden ticket to start shopping.

Step 3: Find an Eligible Home and Make an Offer

Now for the fun part! With your budget locked in, you can start the house hunt. Just remember two key rules: the home must be in a USDA-eligible area, and it has to meet some basic living standards.

Once you find "the one," your real estate agent will help you put together an offer. If the seller accepts, you’ll sign a purchase agreement, which is the official document that gets the mortgage process rolling.

Heads Up: The USDA is particular about property conditions. They want to see a home that’s safe, sound, and functional. An appraiser will check the home's value and make sure it meets these common-sense requirements.

Step 4: Navigate the Dual Underwriting Process

Here’s where USDA loans are a little different. Your application actually gets approved twice in a system called dual underwriting.

First, your lender's own underwriter will comb through your file—your income, credit, the property details, everything. Once they sign off, they bundle it all up and send it over to the USDA for round two.

A USDA official then does a final review to make sure you and the property tick every box for the program. This two-step process is what allows the government to guarantee your loan, but it can add a little more time to your closing. To see how this fits into the bigger picture, take a look at our complete guide to the home buying process timeline.

Step 5: Close on Your New Home

Once the USDA gives its final blessing, you’re in the home stretch! You've got the "clear to close," and it's time to schedule the final meeting with your lender and a title company.

On closing day, you’ll sign the last of the paperwork, pay any closing costs, and get the keys to your new home. It’s an incredible moment—you’re officially a homeowner, and you did it all with a zero-down-payment loan.

USDA Loans Can Do More Than You Think

When most people hear "USDA loan," they immediately think of buying a house in the country. And while that’s a huge part of what they do, it's really just scratching the surface. The USDA's real mission is much bigger: it’s about nurturing the economic health and long-term stability of America's rural communities.

This isn't just about handing out mortgages. Think of the USDA as a foundational support system, working behind the scenes to make sure these areas are great places to live—safe, vibrant, and full of opportunity. It's a holistic, ground-up approach to building strong communities.

More Than Just Mortgages

One of the program's best-kept secrets is the Section 504 Home Repair program. This is a game-changer, offering loans and grants to very low-income homeowners to help them stay right where they are.

These funds are earmarked for critical repairs—the kind that fix serious health and safety issues. We’re talking about helping an elderly resident replace a leaky roof they can't afford, or enabling a family to add a wheelchair ramp for a disabled child. Section 504 makes these essential, life-altering improvements a reality, allowing people to age in place and live safely.

By helping existing homeowners maintain their properties, the USDA strengthens the entire neighborhood's housing stock. That stability directly benefits new buyers, because you’re moving into a community that's being invested in from the inside out.

Strengthening Local Economies

The USDA's reach extends far beyond front doors and picket fences. The agency is a powerhouse for local economies, pumping life into them through a variety of business and agricultural loans designed to create jobs and spark growth.

Take the USDA Farm Service Agency (FSA), for instance. It's playing a vital role in raising the next generation of American farmers. In fiscal year 2023 alone, the FSA backed over 22,000 loans for farmers and ranchers, totaling a massive $4.7 billion. What’s truly incredible is that 60% of that funding went to beginning farmers, showing a real commitment to cultivating new talent. You can dig into the numbers yourself in the 2025 USDA budget summary.

When you start to see this bigger picture, it changes everything. Getting a USDA loan isn’t just a transaction for a piece of property. You're planting roots in a community where the federal government is an active partner, invested in seeing it succeed—from helping the farm down the road expand its operations to making sure a local shop can keep its doors open. It's a shared investment in a brighter future.

Still Have Questions About USDA Loans?

It's completely normal to have a few questions swirling around even after learning about the incredible benefits of a USDA loan. Let's tackle some of the most common ones we hear from homebuyers just like you.

Do I Have to Be a First-Time Homebuyer?

This is a big one, and the answer is a firm no. While USDA loans are a fantastic on-ramp to homeownership for first-timers, they aren't exclusive. As long as you meet the income and location rules and plan to live in the home as your primary residence, you’re welcome to apply, even if you’ve owned a home before.

What's the Deal with Closing Costs?

The zero-down payment feature is the star of the show, but what about the other expenses? You'll still have closing costs—things like appraisal fees, title insurance, and other administrative charges. But here's the good news: USDA loans often let you roll these costs right into your total loan amount, as long as the home appraises for a high enough value. This can dramatically lower the amount of cash you need to have on hand at closing.

How Long Does a USDA Loan Take to Close?

Patience is key here. Because a USDA loan has to be approved by both your lender and the USDA itself, the process can take a bit longer than a conventional loan. You should generally plan on a timeline of 30 to 60 days from application to closing day. It’s not instant, but it’s definitely worth the wait.

Are There Strict Rules About the House Itself?

The USDA isn't expecting a palace, but they do have standards. Their main goal is to ensure you're buying a safe, sound, and sanitary home.

The property has to meet what are called "minimum property standards." Think of it as a basic safety check: the roof can't leak, the plumbing and electrical systems must work properly, and the foundation has to be solid.

This isn't meant to be a roadblock. It's a layer of protection for you and your family, making sure your new home is a secure investment from day one. An appraiser will check these things out as part of the process.

Ready to see if a zero-down USDA loan is your key to homeownership? The expert team at Tiger Loans Inc can guide you through every step. Start your journey today.

Alex Chen

Alex Chen

Get in touch with a loan officer

Our dedicated loan officers are here to guide you through every step of the home buying process, ensuring you find the perfect mortgage solution tailored to your needs.

Options

Exercising Options

Selling

Quarterly estimates

Loans

New home

Stay always updated on insightful articles and guides.

Every Monday, you'll get an article or a guide that will help you be more present, focused and productive in your work and personal life.

.png)

.png)

.png)

.avif)

.avif)

.avif)

.png)

.png)

.png)

.avif)

.png)

.png)

.avif)

.png)

.avif)

.png)

.avif)

.avif)