A Guide to Refinancing a Rental Property

September 6, 2025

Discover how to navigate refinancing a rental property. This guide offers expert strategies for securing better loan terms and maximizing your investment.

Deciding to refinance a rental property is a big move. You're likely weighing the potential upsides—like scoring a lower interest rate or pulling out cash for your next deal—against the hard realities of today's market. It’s a strategic play that can either turbocharge your portfolio's growth or, if timed poorly, saddle you with unnecessary financial strain. The trick is to look at the current lending environment and your own finances with a completely clear and objective eye.

Is Refinancing Your Rental Property a Smart Move Right Now?

Let's be blunt: the landscape for refinancing investment properties has gotten a lot more complicated. The days of rock-bottom interest rates and lenders practically handing out approvals are long gone. Today, real estate investors are navigating a much choppier sea of economic uncertainty, higher borrowing costs, and intense scrutiny from lenders.

To make the right call, you have to look past the simple appeal of a new loan. It’s crucial to understand the powerful forces shaping the market, as they directly affect your chances of getting favorable terms. This isn't just about your credit score anymore; it’s about your entire financial picture in a much tougher climate.

Confronting the Current Market Head-On

The biggest hurdle for investors right now? The dramatic shift in interest rates. Rates for investment properties—which are almost always higher than for a primary home—have jumped significantly. This spike can quickly wipe out any potential savings from a refinance, and in some cases, could even leave you with a higher monthly payment.

At the same time, while some real estate markets are still hot, many others have seen property value growth slow down or even dip. This has a direct impact on your loan-to-value (LTV) ratio, a number lenders watch like a hawk. If your property hasn't appreciated as much as you'd hoped, you might have a lot less equity to play with than you think.

A huge factor adding pressure right now is the sheer volume of real estate loans coming due. This so-called "wall of maturities" creates a hyper-competitive and challenging environment for anyone trying to secure new financing.

The data paints a pretty stark picture. A massive wave of real estate loans, estimated at a staggering USD 500 billion, is set to mature in 2025. Of those, about 14% are considered underwater, meaning the loan balance is higher than the property's current value. The rental apartment sector is feeling this acutely, with roughly USD 19 billion in maturing loans now at risk, making a successful refinance a tough mountain to climb.

Weighing Your Personal Investment Goals

Given this market backdrop, your personal strategy is more critical than ever. You have to get crystal clear on why you're thinking about a refinance in the first place. Your answer will tell you if now is the right time to pull the trigger.

- Rate-and-Term Refinance: Is your main goal to lower your interest rate and monthly payment? You absolutely must run the numbers. Calculate your break-even point—how long it will take for the monthly savings to finally cover your closing costs. If it takes five years to break even and you plan to sell in three, it's a bad deal.

- Cash-Out Refinance: Are you looking to tap into your equity for renovations or to fund a down payment on your next property? This can be an incredible wealth-building tool, but it's not without risk. You'll be taking on a larger loan in a higher-rate environment, which jacks up your property's monthly expenses and shrinks its cash flow.

- Accessing a Line of Credit: Sometimes, investors refinance just to get their hands on cash, when a home equity loan or HELOC might be a smarter, more flexible option. To help you figure it out, our guide on choosing between a refinance and a home equity loan offers a detailed breakdown.

Ultimately, there’s no simple "yes" or "no" answer to whether refinancing your rental is a smart move right now. It demands a realistic look at the market, a thorough crunching of the numbers, and an honest assessment of how this move aligns with your long-term vision as an investor.

How Lenders Will Evaluate Your Refinance Application

Before you even think about filling out a single form, you need to look at your investment property through the same critical lens a lender will. Let's be clear: refinancing a rental isn't like refinancing your home. Lenders treat this strictly as a business transaction, meaning they are going to put your entire financial situation under a microscope.

To get a "yes," you have to prove two things: that you’re a reliable borrower and that the property itself is a sound, profitable asset. It’s a two-part test, and you have to pass both.

First, They Look at You: The Investor

While your property’s performance is crucial, the underwriting process always starts with you. Lenders need to feel confident that you can manage your debts and have the financial footing to handle the loan, especially if your property sits vacant for a few months.

A huge piece of this puzzle is your Debt-to-Income (DTI) ratio. For a rental property refinance, most lenders draw the line at a DTI of 45% or lower. They get this number by adding up all your monthly debt payments—your primary mortgage, car loans, credit cards, plus the proposed new payment on the rental—and dividing it by your gross monthly income.

But here’s a nuance that trips up many investors: when calculating your income, lenders will typically only consider 75% of your gross rental income. Why? They bake in a 25% vacancy factor to account for potential turnover, management fees, and surprise repairs. This conservative math can seriously impact your DTI, so you absolutely must run this calculation yourself before ever speaking to a loan officer.

Next, They Judge the Property's Financial Health

Beyond your personal finances, the property has to prove it can stand on its own two feet as an investment. This is where many people get stuck. They see the equity on paper and assume a refinance is a slam dunk, but lenders dig much, much deeper.

They’ll perform a deep dive into the property's real-world financial performance. A critical first step is figuring out how to find net operating income (NOI), as this is the number their entire analysis hinges on. The NOI—your rental income minus all operating expenses (but not the mortgage)—is what tells a lender if the property is actually making money.

At their core, lenders are risk-averse. They need to see that your property generates enough consistent cash flow to comfortably cover the new mortgage payment and still leave a healthy cushion. A property with thin or negative cash flow is a massive red flag.

Another non-negotiable metric is the Loan-to-Value (LTV) ratio. For a standard rate-and-term refinance, most lenders cap the LTV at 75% on a single-family rental. In plain English, you need at least 25% equity in the property. If you're hoping for a cash-out refinance, the bar is often set even higher.

Recent market volatility has made this a sticking point. With property values correcting in many areas since mid-2022, some investors have found their properties are now appraised for less than what they paid. This puts immediate pressure on LTV ratios and can stop a refinance in its tracks if your equity has evaporated. You can read detailed research on how market valuations impact refinancing feasibility to see how these global trends affect investors.

Lenders need a quick way to gauge the strength of your application. The table below outlines the key benchmarks they use to separate a low-risk investment from a high-risk gamble.

Key Lender Requirements for Rental Property Refinancing

Meeting these benchmarks doesn't guarantee an approval, but falling short on any of them can be an immediate deal-breaker.

Finally, Show Them the Money: The Importance of Cash Reserves

The last hurdle is proving you have enough cash on hand to weather a storm. Lenders call these cash reserves, and they want to see that you can cover mortgage payments during a vacancy or handle a costly surprise, like a new roof or HVAC system, without flinching.

So, what's the magic number?

- For investors with 1-4 financed properties: Lenders typically want to see at least six months of PITI (principal, interest, taxes, and insurance) payments in reserves specifically for the property you're refinancing.

- For seasoned investors with 5+ financed properties: The requirement often jumps to six months of PITI for every single mortgaged property in your portfolio.

These funds have to be liquid and accessible—think checking, savings, or a brokerage account. Your 401(k) usually won't count unless you can withdraw from it without penalty. Strong reserves send a powerful signal to a lender: you aren't just an owner, you're a prepared, professional investor. That makes you a much more attractive, and bankable, client.

Get Your Paperwork in Order for a Fast, Smooth Approval

If there’s one secret to a painless underwriting process, it’s this: have all your ducks in a row before you even start talking to lenders. Nothing slows down a refinance faster than a messy, incomplete application. It creates needless back-and-forth and can frustrate everyone involved.

Think about it from the lender's perspective. When you hand them a perfectly organized file, you’re not just giving them documents; you're showing them you’re a serious, professional investor. That simple act of being prepared can genuinely set a positive tone for the whole deal and get you to the closing table faster.

Your Personal Financial Story

First, the lender needs to get to know you. They need to see a clear picture of your personal financial health to feel confident in your ability to manage your debts. This is all about verifying your stability as the person behind the loan.

You'll need to pull together a few key personal items:

- Tax Returns: Lenders will almost always ask for your last two years of signed, personal tax returns—every single page. If you own the property in an LLC, get ready to provide two years of business returns, too.

- Income Verification: This means your most recent pay stubs covering a 30-day period and your W-2s from the past two years. If you're self-employed, a current year-to-date profit and loss (P&L) statement is standard.

- Asset Statements: Plan on providing your most recent two months of statements for every account where you hold money—checking, savings, brokerage, 401(k)s, you name it. Be prepared to explain any large, out-of-the-ordinary deposits.

My Pro Tip: I learned this the hard way. Create a folder on your computer named "Refinance Docs." Inside, make two subfolders: "Personal" and "Property." Scan everything and give it a clean, logical name like "J.Smith - 2024 W2.pdf." This bit of organization is a massive time-saver.

Managing a high volume of documents is a core skill in real estate. It's worth learning how professional data room real estate deals are handled, as the principles of secure, organized document sharing apply directly here.

The Property's Financial Profile

Now for the property itself. The lender needs proof that your rental is a sound investment that actually makes money. This next set of documents is all about the asset—its income, its expenses, and its overall financial viability. An underwriter is going to pore over these to make sure the numbers work.

Here’s the essential paperwork for the property:

- Lease Agreements: A fully signed, current copy of the lease for every single tenant. This is the ultimate proof of your rental income. It's non-negotiable.

- A Solid Rent Roll: This is a simple summary listing each unit, the tenant's name, their monthly rent, and their lease expiration date.

- Proof of Insurance: You’ll need the "declarations page" from your current landlord or hazard insurance policy.

- Current Mortgage Statement: Your most recent statement from the loan you’re refinancing.

- Property Tax Bill: The latest statement showing what you pay in property taxes annually.

- HOA Statement (if it applies): If your property is in a homeowners association, provide a statement showing the current dues.

Look at yourself as the CEO of your rental business. Assembling this file is like building a business case for your lender. When you present this level of detail and organization, you project confidence and competence, which drastically improves your chances of a quick and successful refinance.

Matching the Right Loan to Your Investment Playbook

So, you've run the numbers and confirmed refinancing your rental property is a smart move. Fantastic. Now comes the crucial part: picking the right loan. This isn't just about finding the lowest rate; it's a strategic decision that needs to align perfectly with what you’re trying to accomplish as an investor.

Are you looking to free up monthly cash flow? Or are you trying to pull out capital to jump on your next deal? The loan you choose is the tool that will get you there. Picking the wrong one can be a costly mistake, tying up your capital and limiting your growth. Let's walk through the main options so you can make a choice that powers your strategy forward.

Rate-and-Term vs. Cash-Out: What's Your Primary Goal?

This is the first and most important fork in the road. While both are types of refinancing, they serve completely different purposes for an investor.

A rate-and-term refinance is the simplest play. You're swapping your old mortgage for a new one, usually to lock in a lower interest rate or change the loan's duration (e.g., from a 30-year to a 15-year). If your main goal is to lower your monthly payment and beef up your property's cash flow, this is your go-to move. It’s clean, straightforward, and focused on improving your existing asset's performance.

A cash-out refinance, on the other hand, is how you tap into the equity you've built. With this option, you take out a new loan for more than you owe and get the difference as a lump sum of cash.

Imagine your rental is worth $400,000 and you have a $200,000 mortgage balance. A lender might offer you a new loan for $300,000 (at a 75% loan-to-value). You'd use $200,000 to pay off the old loan and walk away with $100,000 in tax-free cash.

This is an incredibly powerful tool for scaling your portfolio. That cash can become the down payment on another property or fund significant value-add renovations. But remember, it's not free money—your loan balance and monthly payment will increase, so you need a solid plan to put that capital to work profitably.

For investors who are purely focused on accessing capital, it's smart to weigh all your options. A cash-out refi isn't the only game in town. Our guide comparing a home equity loan vs. refinance breaks down the pros and cons to help you decide which is better for your specific financial picture.

To help you visualize the best path, here’s a quick comparison of the most common loan types for real estate investors.

Comparing Refinance Loan Types for Investors

This table offers a side-by-side look at the most common refinancing options for rental properties to help you decide which fits your investment strategy.

Ultimately, the right loan is the one that directly supports your next move. Whether you're playing defense by boosting cash flow or offense by pulling out capital, clarity on your goal is the first step.

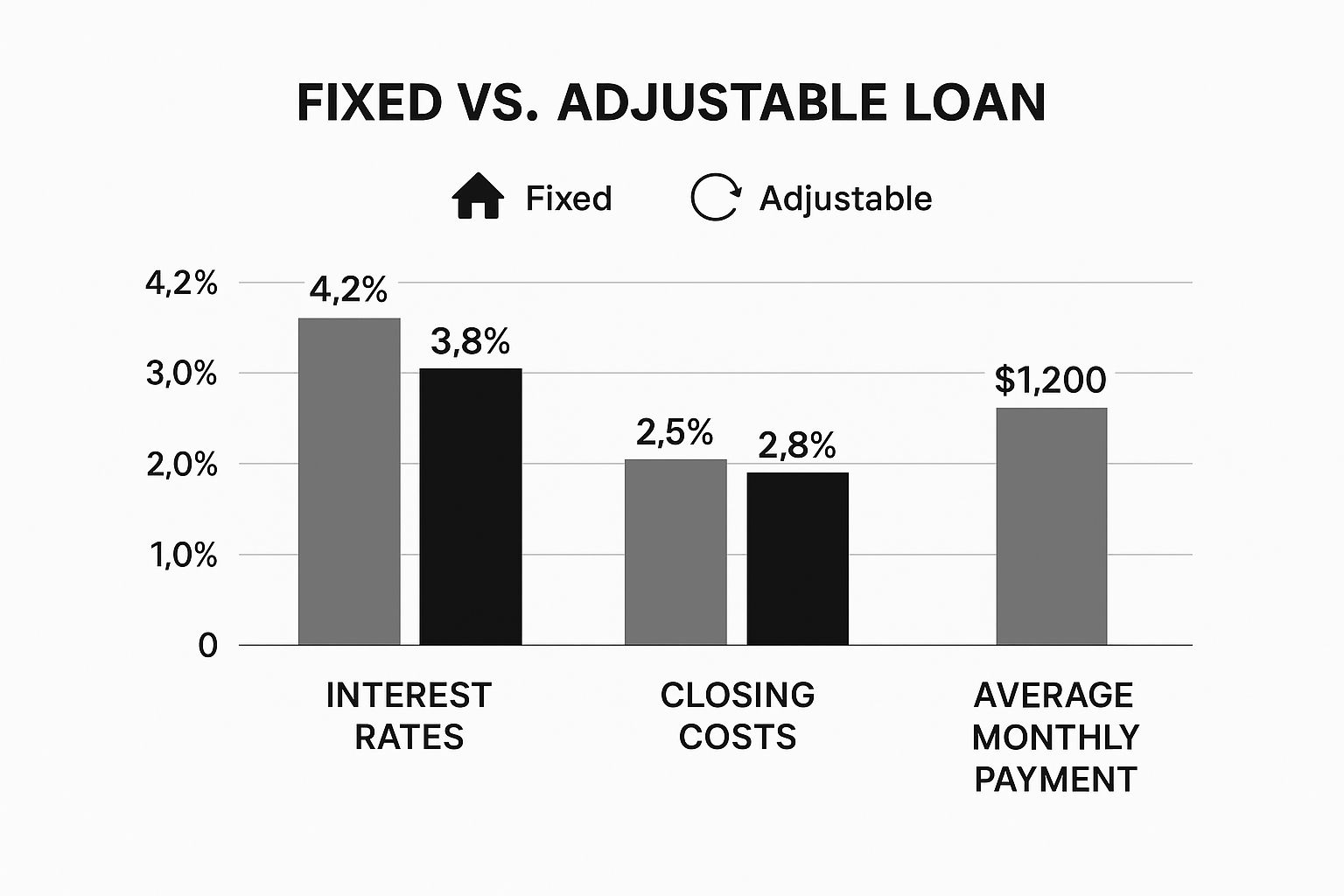

Fixed-Rate vs. Adjustable-Rate: How Much Risk Can You Stomach?

The next big decision is whether to lock in your rate for the long haul or take a chance on a variable rate. Your answer should depend entirely on your holding strategy and risk tolerance.

- A Fixed-Rate Mortgage (FRM) is the definition of stability. Your interest rate is set in stone for the entire loan term. This means your principal and interest payment will never change. For most buy-and-hold investors, this is the gold standard. It provides predictable expenses, making it easy to calculate cash flow for years to come.

- An Adjustable-Rate Mortgage (ARM) offers a bit of a gamble. You'll get a lower, "teaser" interest rate for an initial period—typically 5, 7, or 10 years. After that, the rate adjusts up or down with the market. An ARM can be a savvy move if you plan to sell or refi the property before that initial period ends. You get the benefit of lower payments now without exposure to future rate hikes.

This image gives you a sense of how the payments and costs can differ.

The trade-off is clear: an ARM can save you money upfront, but it introduces uncertainty down the road. A fixed rate costs a little more in the beginning but gives you priceless peace of mind.

Advanced Tools for the Seasoned Investor

Once you have a few properties under your belt, you unlock more sophisticated financing options that aren't available to rookie investors.

One of the best tools for scaling is a portfolio loan. Instead of getting a separate loan for each property, a portfolio loan is a single, blanket mortgage that covers multiple assets. This streamlines everything—one application, one set of underwriting, and one monthly payment.

Lenders who offer these loans are often more flexible. They're looking at the health of your entire portfolio, not just a single property's DTI or LTV. If you have a strong track record and a collection of cash-flowing rentals, a portfolio loan can be a game-changer.

The bottom line is simple: start with your end goal in mind. Figure out exactly what you want this refinance to do for you, and then work backward to find the loan that will get the job done.

Getting to the Finish Line: Appraisal and Closing

You’ve wrestled with the paperwork, your lender has given you the pre-approval, and the finish line is in sight. Congratulations! This is a huge milestone when you're refinancing a rental property. But don't start celebrating just yet. You’re now heading into the two most critical phases: the property appraisal and the closing table.

This is where the rubber truly meets the road. These final steps are notorious for throwing curveballs, so knowing exactly what’s coming is your best defense against last-minute headaches. The focus now shifts from your personal finances to the nitty-gritty details of the property and the legal transfer.

Nailing the Investment Property Appraisal

An appraisal on a rental property isn't like the one for your own home. It’s a completely different animal. While a tidy appearance helps, the appraiser is there to answer one core question: What is this property worth as a cash-flowing asset? Their final number will make or break your deal, directly impacting the loan amount the lender puts on the table.

Appraisers have a few tools in their belt, but for investment properties, they lean heavily on the "income approach." This means they're scrutinizing comparable rental rates—or "rent comps"—in your neighborhood to land on a fair market rent. This is why having your rent roll and current lease agreements buttoned up is non-negotiable.

You can—and absolutely should—prep your property to get the best valuation possible:

- Wipe Out Deferred Maintenance: That drippy faucet in the bathroom? The wobbly fence post? The peeling paint on the trim? Fix them. Small repairs tell an appraiser you run a tight ship.

- Create a "Brag Sheet": Put together a simple one-page summary of every major upgrade you've made. List the improvement, when you did it, and what it cost. A new roof in 2022 or a new HVAC system last year are major value-adds, so make sure they know.

- Dial-Up the Curb Appeal: It sounds simple, but a freshly mowed lawn, neat bushes, and a clean walkway set a powerful first impression. It shows you care.

As you get ready for the appraiser's visit, digging into various strategies to increase your property's value can pay off big time. A higher valuation strengthens your loan-to-value (LTV) ratio, which is your single biggest point of leverage with the lender.

Getting Through the Closing Process and Costs

Once the appraisal comes back clean and the underwriter gives the final green light, it's time to head to closing. This is the formal meeting where you'll sign a mountain of paperwork and your new mortgage officially pays off and replaces the old one.

You’ll receive a document called the Closing Disclosure (CD) at least three business days before your closing appointment. This five-page form is critical; it itemizes every single final, exact cost and term of your loan.

Investor Tip: Treat your Closing Disclosure like a legal document—because it is. Compare it line-by-line against the Loan Estimate you got at the beginning. If a number looks off, call your loan officer immediately. This is your last chance to fix errors before they’re set in stone.

Be prepared: closing costs for an investor refinance typically run higher than for a primary home, usually between 2% to 5% of the loan amount. These fees cover a wide range of services from the lender and other third parties.

Here’s a look at what you’re likely paying for:

- Loan Origination Fees: What the lender charges for creating and processing your loan.

- Appraisal Fee: The cost for that all-important property valuation.

- Title Insurance Fees: Protects the lender from any future claims against the property's title.

- Escrow and Attorney Fees: Charges for coordinating the closing and managing the legal paperwork.

- Prepaid Expenses: Your first payments for things like property taxes and homeowners insurance.

You need to budget for these costs carefully. For a $300,000 refinance, you could easily be looking at $9,000 in closing costs. Having those funds ready to go is crucial to avoid derailing the entire deal at the last minute. It’s a stark reminder that the long-term math on the refinance has to make sense.

Common Questions About Refinancing a Rental Property

Even the most seasoned investors have questions when it comes to refinancing a rental. It's a process with a lot of moving parts. Let's clear up some of the most common hurdles and sticking points I see investors grapple with all the time.

Getting these answers straight will give you the confidence to make the right moves for your portfolio.

How Soon Can I Refinance After Buying a Rental?

I get this question almost every day. The answer boils down to what lenders call "seasoning." They want to see a track record of ownership and payments before they'll give you a new loan.

For a simple rate-and-term refinance, you're usually looking at a six-month waiting period. But if you're planning a cash-out refinance, lenders get a bit more conservative. For those, expect to wait a full 12 months before most banks will even look at your application. While some niche portfolio lenders might offer a little wiggle room, six to twelve months is the solid rule of thumb you should plan for.

Will Refinancing Affect My Property Taxes?

This is a huge source of confusion for investors. The good news is, a standard refinance—where you just change your rate or term—almost never triggers a reassessment of your property taxes. You're simply swapping out one loan for another, which has no bearing on the value your county tax assessor uses.

A cash-out refinance is a bit different, but not in the way most people think. The money you pull out is not taxable income. It’s a loan, not a profit. The real impact on your taxes comes from the mortgage interest deduction. Your new, larger loan balance and different interest rate will change the amount you can deduct each year.

Important Takeaway: The cash you take out isn't taxed, but your annual interest deduction will change. It's always a smart move to have a quick chat with your tax advisor to see exactly how a cash-out refi will play out on your specific return.

Can I Refinance a Vacant Rental Property?

This one is tough. With most lenders, trying to refinance a vacant property is a non-starter. Why? Because underwriters rely on proven rental income to approve the loan and calculate your debt-to-income ratio. No tenant means no income, which looks like pure risk on their end.

Your best—and often only—path forward is to secure a fully executed, signed lease agreement. If the property is empty, your first job is to find a qualified tenant. Get that lease signed and a security deposit in hand, and then circle back with your lender. That lease is the proof of income they absolutely need to see.

Before you get too far down the road, it pays to be prepared. Check out our guide on the 10 essential questions to ask before refinancing to make sure you're not missing any crucial details. A little prep work now can save you a world of headaches later.

Ready to explore your refinancing options and see how you can leverage your property's equity? The expert team at Tiger Loans Inc is here to guide you through every step, from assessing your eligibility to finding the perfect loan product for your investment goals. Get started with a free consultation today!

Alex Chen

Alex Chen

Get in touch with a loan officer

Our dedicated loan officers are here to guide you through every step of the home buying process, ensuring you find the perfect mortgage solution tailored to your needs.

Options

Exercising Options

Selling

Quarterly estimates

Loans

New home

Stay always updated on insightful articles and guides.

Every Monday, you'll get an article or a guide that will help you be more present, focused and productive in your work and personal life.

.png)

.png)

.png)

.png)

.png)

.png)

.png)

.png)

.png)

.png)

.png)

.png)

.png)

.png)

.png)

.png)

.png)

.png)

.png)

.png)

.png)

.png)

.png)

.png)