Income Requirements for VA Loan: What You Need to Know

November 19, 2025

Discover the income requirements for VA loans and how they impact your eligibility. Learn key factors like DTI and residual income to secure your home loan.

Right off the bat, let's bust the biggest myth out there about VA loan income requirements: there is no official minimum income you need to earn. It’s a common misconception, but it’s just not true.

Unlike conventional loans that might slam the door shut if you don't hit a certain salary, the VA loan program is far more interested in your real-world ability to handle your mortgage payment. It’s a practical, flexible approach built for the diverse financial situations of our service members and veterans.

The Truth About VA Loan Income Requirements

When you sit down to apply for a VA loan, the lender isn't scanning your application for a specific six-figure salary. What they really want to see is proof of stable, reliable income and enough financial breathing room to manage homeownership without getting in over your head.

This is a huge departure from other types of mortgages and gets right to the heart of the VA's mission: helping veterans build lasting financial stability, not just get a house key.

To figure this out, lenders lean on two core pillars of your financial health. Together, these metrics paint a much clearer and more accurate picture of your ability to handle a mortgage than any simple income number ever could.

The Two Pillars of VA Income Qualification

Forget about a single income threshold. Your approval really hinges on how you stack up in two key areas:

- Debt-to-Income (DTI) Ratio: Think of this as a quick financial check-up. It's the percentage of your gross monthly income that’s already spoken for by other debt payments (like car loans or credit cards). It shows lenders how much of your paycheck is already committed elsewhere.

- Residual Income: This is the game-changer. It's the cash you have left over each month after you’ve paid your new mortgage payment and all those other debts. This is your money for groceries, gas, utilities, and life's little surprises. It's your financial safety net.

This two-pronged approach is really there to protect you, the borrower. It’s designed to ensure you not only qualify for the loan but can comfortably and successfully stay in your home for the long haul.

By looking at your whole financial story—not just a number on a W-2—the VA loan program makes homeownership a real possibility for a much broader group of deserving veterans and active-duty members.

Because of this flexibility, it doesn't matter if you're transitioning into a new civilian career or have been earning a steady income for years. You get a fair shot. The system is built to understand your unique situation, giving you a personalized path to buying your home. Ultimately, it’s less about how much you make and more about how well you manage the money you have.

How Your DTI Ratio Shapes Your Loan Approval

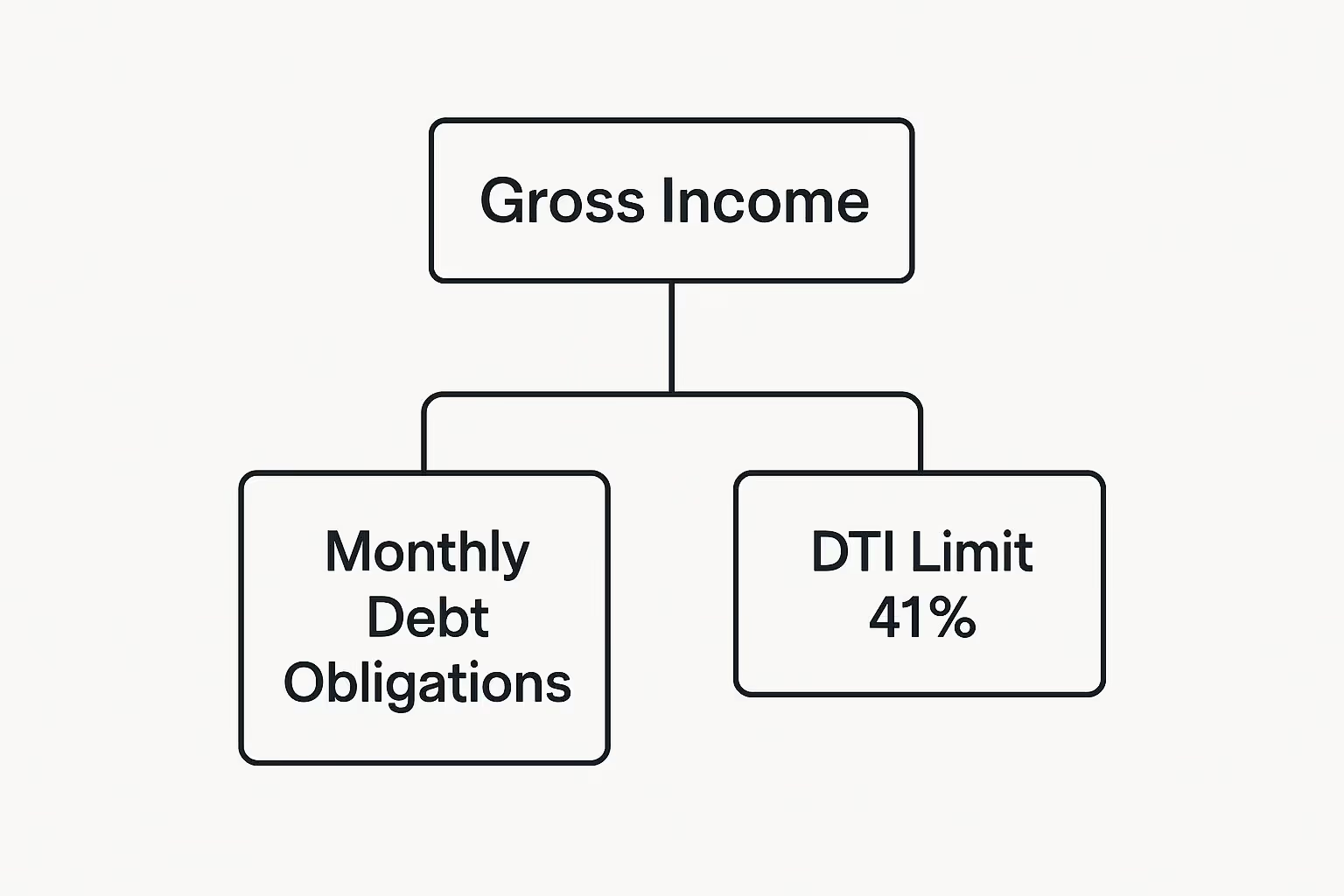

While the VA itself doesn't draw a hard line in the sand with a strict debt-to-income (DTI) limit, this number is one of the most critical pieces of your entire loan application. Think of it as a quick financial health checkup. It tells lenders exactly what slice of your monthly income is already spoken for by existing debts.

The math is pretty simple. Lenders will add up all your monthly debt payments—things like car loans, student loans, and minimum credit card payments—and divide that by your gross monthly income (your pay before taxes). The result gives them a clear, immediate snapshot of your financial commitments before they even consider adding a new mortgage to the mix.

The VA loan program is famous for its flexibility, but the lenders who actually fund the loans still need a solid way to measure risk. That’s where the 41% DTI guideline enters the picture. It’s not an absolute rule, but it’s a benchmark that almost every lender uses for a smoother, faster approval.

The 41% Guideline Explained

If your DTI ratio lands at or below 41% with your new mortgage payment factored in, you're in the sweet spot. Lenders look at that number and feel confident that you can comfortably handle your new house payment without stretching your budget too thin.

In the world of VA loan underwriting, this DTI percentage is a huge deal. The vast majority of approved VA loans go to borrowers who meet this 41% benchmark, which shows just how much lenders value that financial breathing room. For instance, if your household brings in $6,000 a month and your total debts (including the new mortgage) are $2,460, you have a DTI of exactly 41%—right on the money.

Here's the bottom line: A DTI over 41% isn't a deal-breaker. It’s more like a yellow flag that tells the lender, "Okay, let's dig a little deeper to make sure this loan is a responsible and sustainable fit for this Veteran."

This is where the VA loan really stands out. Your application doesn’t live or die by a single number. A higher DTI just triggers a closer look for what underwriters call compensating factors. You can get more context on this by checking out our complete guide to VA loan income requirements for 2025.

Overcoming a High DTI with Compensating Factors

So what are compensating factors? Think of them as aces up your sleeve—financial strengths that prove you’re a solid borrower, even if your DTI is a bit high. They paint a bigger picture for the lender, showing that you’re financially responsible in other ways.

These are the kinds of strengths that can turn a "maybe" into a "yes":

- Excellent Credit: A high credit score is proof of your track record. It shows you’ve consistently managed debt well over time.

- Significant Savings: Having a healthy amount of cash in savings or other assets demonstrates you have a safety net for life’s curveballs.

- Stable Employment: A long and steady job history in the same industry speaks volumes about your income stability.

- Growing Income: If you can show a clear path of career advancement or have a new job lined up with a pay raise, that can also tip the scales in your favor.

By highlighting these strengths, you can build a powerful argument for your approval, proving that you’re more than just a number on a spreadsheet. It’s all about showing your overall financial stability.

Mastering Residual Income: The VA's Financial Safety Net

While your DTI ratio gives a bird's-eye view of your finances, residual income is where the VA gets up close and personal. Think of it as the VA's secret weapon—a financial safeguard designed to ensure you can actually enjoy your new home, not just struggle to pay for it.

It’s a far more practical measure of affordability. Simply put, residual income is your "money left for living." After your new mortgage payment, property taxes, insurance, and all other monthly debts (like car loans and credit card payments) are accounted for, this is the cash left over. It’s what you’ll use for groceries, gas, utilities, and all of life's other necessities.

How The VA Calculates Your Cushion

The VA doesn't just pull a number out of thin air. Instead, it builds a personalized financial safety net based on your specific life circumstances. This customized approach is a huge reason why the income requirements for a VA loan are often more flexible and realistic than other loan types.

Your lender will figure out your minimum required residual income by looking at three main things:

- Your Family Size: It makes sense, right? A larger family has higher living expenses, so you'll need a bigger cushion.

- Your Geographic Location: The cost of living isn't the same everywhere. The VA uses regional charts to account for the difference between living in, say, San Diego versus Des Moines.

- Your Proposed Loan Amount: Larger loans also factor into the calculation, though to a lesser degree.

This first step—assessing your income against your debts—sets the stage for the all-important residual income calculation.

As you can see, once the basic DTI guideline is met, the real focus shifts to making sure you have enough breathing room for your day-to-day life.

Why Location and Family Size Are So Important

This tailored approach really shows the VA’s commitment to setting you up for long-term success. It’s a commonsense recognition that a family of four in the pricey Northeast needs a much larger financial buffer than a single veteran living in the more affordable Midwest.

The VA’s residual income calculation isn't a rigid rule designed to shut you out. It’s a flexible guideline meant to protect you from becoming "house poor"—a situation where your home payment eats up so much of your income that there's nothing left for anything else.

To give you a clearer picture, here’s a sample of how these requirements can change based on your family and where you plan to live.

Sample VA Residual Income Requirements by Region

According to the VA's guidelines, a single veteran buying a home in the West needs at least $450 in monthly residual income, whereas a family of four in the Midwest requires $1,003. This incredible flexibility is a major reason why VA loans have historically had some of the lowest default rates in the industry.

And if your numbers come up a little short at first, don't panic. In 2023, about 12% of VA applications were initially flagged for residual income concerns. The key takeaway? Most of those were resolved by making small adjustments, not by outright denial. An underwriter will look for compensating factors or suggest ways to get you across the finish line, proving the VA is truly invested in helping you find a path to homeownership.

What Counts as Verifiable Income for a VA Loan?

When a VA lender looks at your income, they’re really asking two simple questions: Is it stable, and is it reliable? They want to see a dependable history of earnings that looks like it will stick around for at least the next three years. This focus on consistency is great news, because it means a traditional W-2 salary isn't the only way to unlock this incredible home loan benefit.

Think of your verifiable income less like a single pay check and more like a complete financial story. The VA program is designed to read that whole story, even if it has a few different chapters. As long as you can back it up with documentation, many different income streams can help you qualify.

Beyond the Traditional Pay check

Lenders are fully prepared to look at a wide range of income sources. This flexibility is what opens the door to homeownership for so many veterans with diverse careers and financial lives.

Here are some of the most common types of income that work:

- Standard Employment: This is the most straightforward. If you have a full-time or part-time job, you'll generally need your last 30 days of pay stubs and W-2s from the past two years.

- Military Income: Of course! All your active-duty pay counts, including special pay and allowances like your Basic Allowance for Housing (BAH) and Basic Allowance for Subsistence (BAS).

- Self-Employment Income: Absolutely. If you're a business owner or freelancer, you can definitely qualify. Lenders will typically want to see at least two years of tax returns and profit-and-loss statements to establish a stable monthly average.

- Retirement and Disability Benefits: Income from pensions, Social Security, and VA disability compensation is considered very stable and can be a huge asset to your application.

- Other Verifiable Sources: This can include income from rental properties, alimony, or child support, as long as you can show a history of consistent payments and a strong likelihood they will continue.

Proving Your Income Is Rock-Solid

Regardless of where your money comes from, it’s up to you to prove it’s reliable. One of the best things about VA loans is that, unlike many other government-backed mortgages, they've never had a maximum income cap. For 2025, the focus remains entirely on stability, not a specific salary, which helps both modest and high-earning veterans qualify.

Instead of income limits, lenders analyze your complete financial picture. They generally prefer a debt-to-income (DTI) ratio below 41% and will verify that you meet the residual income standards for your region. For example, a veteran with a family of four in the Northeast needs to have at least $1,025 left over each month after paying major bills. You can discover more insights about these unique requirements and how they work.

The core principle is simple: Can you prove this income has been consistent in the past and is likely to be consistent in the future? For any non-traditional income, strong documentation is your best friend.

A part-time job you've held for several years is going to look much more stable than one you just started last month. It's all about demonstrating that your financial footing is solid, no matter what your career looks like. This common-sense approach is what makes the path to homeownership accessible based on your true financial capability.

Alright, let's get your finances squared away so you can walk into a lender's office with total confidence. Knowing the rules for VA loan income is the first step, but the real magic happens when you start actively shaping your financial picture. This is where you put that knowledge to work.

Think of it like preparing for a mission. Before you go, you run through your checklist, making sure every piece of gear is in top shape. By tuning up your finances before you apply, you’re setting yourself up for a much smoother, faster approval process. We’ll focus on the two big players here: your DTI ratio and your residual income.

Get Your Debt-to-Income Ratio in Check

Lowering your DTI is probably the single most powerful move you can make. Your income is what it is, at least in the short term. The quickest way to move the needle is to shrink your monthly debt payments. It’s simple math, really.

Here are a few tried-and-true tactics that work:

- Attack High-Interest Debt: Go after your credit card balances first. They usually have brutal interest rates, and paying them down directly reduces the minimum monthly payments that count against you.

- Think About Debt Consolidation: Juggling multiple credit cards or personal loans? Rolling them into one consolidated loan could drop your total monthly payment. This one move can give your DTI a significant, immediate boost.

- Freeze All New Debt: This is a big one. Seriously. Do not—I repeat, do not—go finance a new truck, buy a roomful of furniture on credit, or open new store cards. Every new payment you add is a step in the wrong direction. Just put a pin in it until after you close on the house.

Beef Up Your Residual Income

Next up is your residual income—the cash you have left after all your major bills are paid. Lenders love to see a healthy buffer here because it proves you can handle unexpected costs without missing a mortgage payment. This isn't necessarily about earning more; it’s about being smart with what you already have.

The best way to do this? Create a real, honest-to-goodness household budget. It’s not about restricting yourself; it’s about knowing exactly where your money is going.

A budget isn't a financial straitjacket—it's your command center. It gives you the intelligence you need to find pockets of cash you can redirect to savings or debt, which directly pumps up your residual income.

Once you see the numbers laid out, you’ll be surprised at where you can trim the fat. A few canceled subscriptions here, a few less takeout orders there... it all adds up. Finding a better deal on your car insurance alone can free up a surprising amount of cash each month. Every single dollar you save goes straight to your bottom line.

Finally, and this is crucial, stable employment is the foundation of your entire application. Lenders want to see consistency and predictability. Try to avoid jumping to a new job—especially if it’s in a totally different field or moves you to a commission-only structure—right before or during the loan process. A steady paycheck is what holds it all together.

Common Questions About VA Loan Income

Even after you get a handle on DTI and residual income, it’s completely normal to have questions about how your specific financial life fits into the VA loan puzzle. The VA program is designed to be flexible, but that same flexibility can sometimes create nuanced questions based on your unique circumstances.

Let's walk through some of the most common—and important—questions we hear from veterans and service members every day. Getting straight answers here will build your confidence and clear up any final uncertainties before you move forward.

Can I Get a VA Loan with Self-Employment Income?

Yes, you absolutely can. For self-employed borrowers, the name of the game is proving you have a stable and reliable income history. Lenders aren't looking for a traditional W-2; they're looking for consistency.

You’ll typically need to show them at least two full years of financial records. This means handing over your federal tax returns (both personal and business) and your profit-and-loss statements. From there, the lender will calculate an average monthly income they can depend on for your qualification. Meticulous record-keeping is your best friend in this scenario.

Can My Spouse's Income Help Me Qualify?

This is a powerful and very common strategy to strengthen your application. The answer is a big yes—your spouse's income can be included to help you qualify, as long as they are a co-borrower on the loan.

Their income just has to meet the same stability and reliability standards as yours. It doesn't matter one bit if your spouse is a non-veteran; their verifiable income gets added right on top of yours. This combined household income is then used to calculate your DTI and residual income, which can give your borrowing power a serious boost.

Key Takeaway: Combining incomes is one of the single most effective ways to improve your financial profile. It often allows you to qualify for a larger loan and shows the lender a much lower-risk financial picture.

By joining forces financially, you and your spouse present a much stronger case, making the path to homeownership smoother and more accessible.

What Credit Score Do I Need for a VA Loan?

This is a crucial point that trips a lot of people up. While the Department of Veterans Affairs itself doesn't set a minimum credit score, the private lenders who actually fund the loans do.

Most VA-approved lenders are looking for a minimum credit score somewhere in the 620 to 640 range. Think of your credit score as a vital part of your financial story—it tells lenders how responsibly you've handled debt in the past.

A strong score can also act as a powerful compensating factor. This means it can help you get approved even if your DTI is a little over the typical 41% guideline. It works together with your stable income to paint a well-rounded, low-risk picture for the underwriter. For a deeper dive, you can explore the full picture of VA loan eligibility requirements in our other guides.

What If My Income Falls Short of the Guidelines?

Don't panic. Coming in just under the residual income guideline is not an automatic "no." The VA loan process was built with real-world flexibility, always keeping its mission to help veterans achieve homeownership in mind.

First, an underwriter will double-check every calculation to make sure there wasn't a simple error. If a small shortfall still exists, they'll immediately start looking for those valuable compensating factors we mentioned, such as:

- A high credit score

- Significant savings or other assets

- A consistent history of paying rent that is equal to or higher than the new mortgage payment would be

If those factors aren't quite enough to bridge the gap, your lender will work with you to find a solution. That might mean looking at a slightly less expensive home to lower the loan amount or paying off a small credit card to free up that last bit of necessary monthly cash. The goal is always to find a secure and sustainable path forward.

Ready to turn your homeownership dream into a reality? At Tiger Loans Inc, our team of experts is dedicated to guiding you through every step of the VA loan process. We provide the personalized support and competitive financing you need to secure your home. Get started with your pre-approval today!

Alex Chen

Alex Chen

Get in touch with a loan officer

Our dedicated loan officers are here to guide you through every step of the home buying process, ensuring you find the perfect mortgage solution tailored to your needs.

Options

Exercising Options

Selling

Quarterly estimates

Loans

New home

Stay always updated on insightful articles and guides.

Every Monday, you'll get an article or a guide that will help you be more present, focused and productive in your work and personal life.

.png)

.png)

.png)

.avif)

.avif)

.avif)

.png)

.png)

.png)

.avif)

.png)

.png)

.avif)

.png)

.avif)

.png)

.avif)

.avif)