Discover Veterans First Mortgage Rates – Save on Your Home Loan

November 19, 2025

Explore how to secure the best veterans first mortgage rates. Learn tips to get favorable VA home loan rates today. Click to start saving!

For any homebuyer, locking in a great mortgage rate is a huge win. But for veterans, the VA loan program gives you a distinct edge. The interest rate you ultimately secure isn't just a number pulled from a hat; it’s a direct reflection of your financial picture, the type of loan you choose, and, most importantly, the lender you work with.

Think of finding the best veterans first mortgage rates not as a daunting task, but as a real opportunity to save a serious amount of money over the life of your loan.

Your Roadmap to the Best VA Mortgage Rate

This guide is designed to be your roadmap, demystifying how VA mortgage rates are actually set. We'll cut through the jargon and financial-speak to show you exactly how to take control of the process. Once you understand the levers you can pull, you have the power to influence your rate for the better.

Why Your Rate Isn't Set in Stone

Picture this: two veterans with nearly identical service records both apply for a VA loan. One gets offered a rate of 6.25%, while the other is quoted 6.75%. What gives? The difference almost always comes down to their personal financial situations and the lender they chose.

Lenders like Tiger Loans look at the whole person, not just your honorable service. This is fantastic news because it means you aren't just a passenger on this ride—you're in the driver's seat.

What We Will Cover

We’ve built this guide to give you a clear, actionable game plan for securing the most competitive rate out there. We’ll walk you through every factor that matters, including:

- The VA Guarantee: We'll break down how the government's backing makes lenders feel more secure, which translates directly into better rates and terms for you.

- Your Financial Profile: A deep dive into how things like your credit score, debt-to-income ratio, and loan term directly shape the interest rate you're offered.

- Refinance Strategies: Getting clear on the difference between a streamlined rate reduction (IRRRL) and a cash-out refinance so you can pick the right tool for your financial goals.

- Choosing the Right Partner: Why working with a specialist VA lender like Tiger Loans can be a game-changer on your path to homeownership.

Our goal is to help you move from simply accepting the first rate you see to actively shaping the best possible outcome. By the end of this guide, you’ll have the confidence and knowledge to secure a mortgage that truly honors your service and builds your financial future.

This is about empowerment. With the right information and a partner who has your back, you can navigate the path to homeownership and lock in the excellent mortgage rate you've earned. Let’s get started.

How the VA Loan Program Delivers Better Rates

So, what’s the secret sauce that makes VA loans so much better than other options? It all comes down to one powerful element: the VA guarantee.

Think of it this way. If you were asking a bank for a big loan, and your wealthy, financially stable uncle offered to co-sign, the bank would breathe a sigh of relief. You'd instantly become a safer bet. That's exactly what the Department of Veterans Affairs does for you. The VA doesn't hand you the money directly, but by guaranteeing a portion of the loan, they give private lenders like us at Tiger Loans the confidence to offer you incredible terms.

This government backing is why veterans first mortgage rates are consistently some of the lowest on the market. It’s a partnership designed to translate your military service into real, tangible savings on your path to homeownership.

The Power of Zero Down Payment

Let's talk about one of the biggest hurdles in homebuying: the down payment. With a conventional loan, you're expected to bring a hefty chunk of cash to the table—typically 3% to 20% of the home's price. For many, that's a goal that takes years of disciplined saving to reach.

The VA loan throws that obstacle out the window. You can finance 100% of the home's value, meaning you can buy a home with zero money down. This is a game-changer, dramatically speeding up the timeline for service members and their families. The money you've worked hard to save can go toward moving costs, new furniture, or simply bolstering your emergency fund.

Freedom From Private Mortgage Insurance

Here's another massive financial advantage: no Private Mortgage Insurance (PMI). If you get a conventional loan and put down less than 20%, lenders will require you to pay for PMI every single month. This insurance protects them, not you, and it can easily add hundreds of dollars to your monthly payment without building a single dime of equity. It’s essentially a fee for having a smaller down payment.

Since the VA already provides a guarantee to the lender, PMI is completely unnecessary. This one feature alone can save you thousands upon thousands of dollars over the life of your loan, keeping your monthly payment as low as possible.

When you combine no down payment with no PMI, the financial picture becomes crystal clear. Your upfront costs are lower, and your monthly payments are more affordable. Dive deeper into how these powerful VA loan benefits can stack up for you.

Competitive Rates in a Fluctuating Market

Even when the market gets a little turbulent, the VA guarantee helps keep interest rates stable and low for veteran borrowers. Lenders simply face less risk, and they pass those savings on to you in the form of better rates. It’s not uncommon to see VA loan rates beat out their conventional counterparts.

For instance, despite recent market shifts, VA loans remain incredibly competitive. In early July 2025, a 30-year fixed VA purchase rate was sitting around 5.875%. Refinancing options were just as strong, with a 30-year VA streamline refinance (IRRRL) at about 5.99% interest and a 30-year VA cash-out refinance around 6.5%. This structure is built to honor your service by giving you a real financial advantage in the housing market.

The Levers That Control Your VA Mortgage Rate

Securing the best veterans first mortgage rates isn’t about luck; it's about understanding what you can control. Your final interest rate isn’t some random number pulled out of a hat. Instead, it’s a direct reflection of a few key financial factors—factors you have more power over than you might think.

This is your chance to get in the driver's seat. By getting a handle on these levers, you can actively strengthen your financial profile before you even fill out an application. Let’s break down exactly what lenders like Tiger Loans look at, so you can walk in ready to secure the most competitive rate possible.

Your Credit Score: The Cornerstone of Your Rate

Think of your credit score as your financial handshake. It's a quick, powerful way for lenders to see how you've handled credit and debt in the past. A higher score tells them you're a reliable borrower, which almost always means a lower interest rate for you. It's that simple.

Now, the VA itself doesn't have a minimum credit score requirement, which is fantastic news. But the private lenders who actually issue the loans, including us at Tiger Loans, do. While VA guidelines are generally more forgiving than those for conventional loans, your score still carries immense weight.

The difference between a 640 score and a 740 score can be staggering, potentially saving you tens of thousands of dollars over the life of your mortgage. This is, without a doubt, the single most powerful lever you can pull to lower your long-term borrowing costs.

Demystifying Your Debt-to-Income Ratio

Your Debt-to-Income (DTI) ratio is the next critical piece of the puzzle. It’s just a simple percentage that shows how much of your monthly income is already spoken for by existing debts—think car payments, student loans, and minimum credit card payments.

Imagine your monthly income is a pie. Lenders want to see that your current debts are only taking up a small slice, leaving a hefty portion for your new mortgage payment and all of life's other expenses. A low DTI shows you aren't financially stretched and can comfortably take on a home loan.

Pro-Tip: You'd be surprised how much small actions can help. Paying down a credit card by $2,000 or knocking out a small personal loan before you apply can seriously improve your DTI. This instantly makes you a stronger, more attractive candidate for a great rate.

The Impact of Your Loan Term and Down Payment

The way you structure your loan also directly influences your interest rate. The two biggest choices you'll make here are the loan term (how long you take to repay it) and whether you make a down payment.

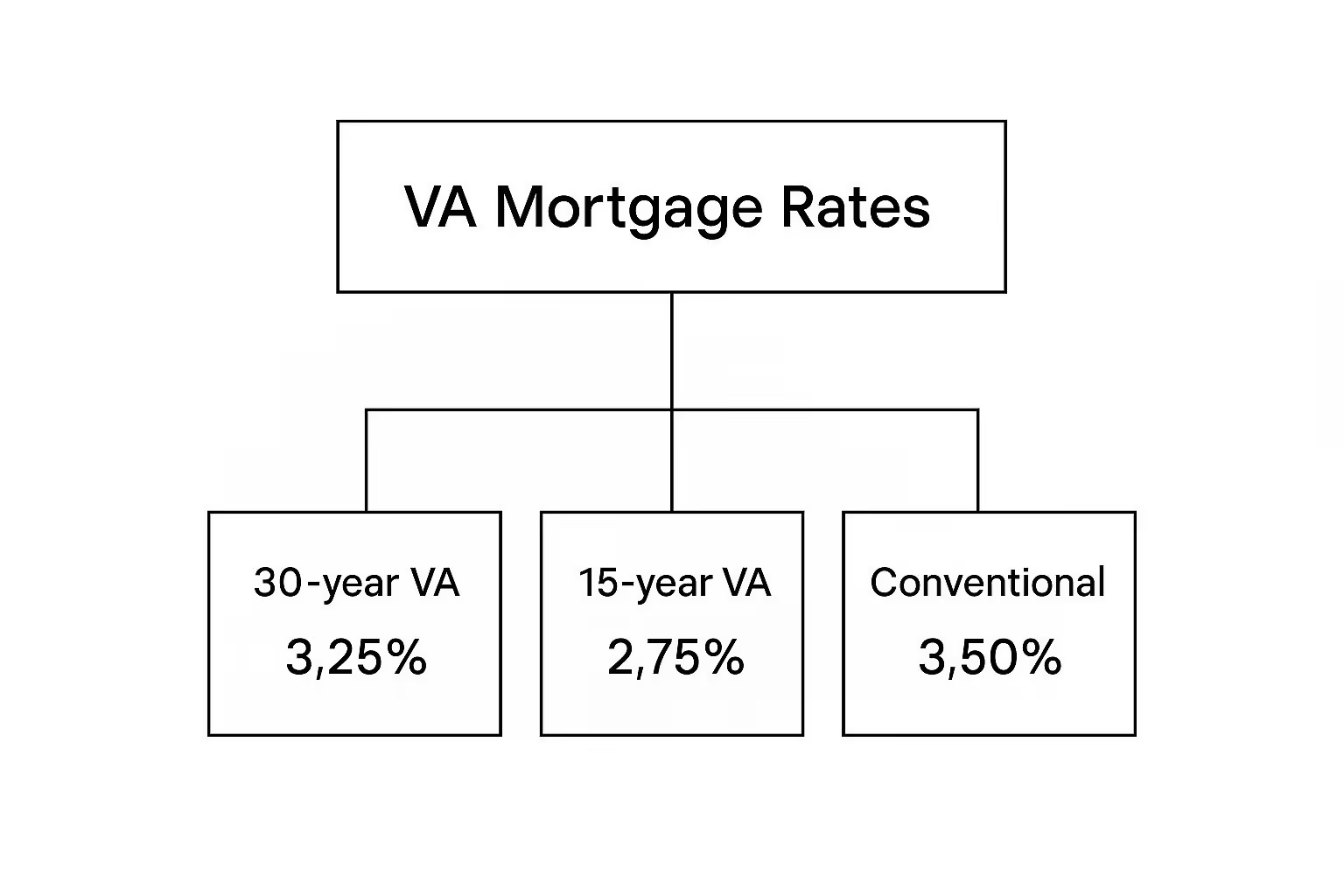

- Loan Term (15 vs. 30 Years): A 15-year mortgage will almost always land you a lower interest rate than a 30-year loan. Why? Because the lender gets their money back twice as fast, which means less risk for them. Your monthly payment will be higher, but you’ll build equity like crazy and pay dramatically less in total interest over time.

- Down Payment: One of the most celebrated benefits of a VA loan is the option for 100% financing—no down payment required. While this is an incredible advantage, putting some money down can still be a smart move. Even a small down payment lowers the lender's risk and can sometimes persuade them to offer you a more favorable rate.

This is a powerful concept to see in action.

As you can see, shorter-term VA loans often beat their 30-year counterparts on rate and can even be more competitive than conventional loan options.

How These Factors Work Together in the Real World

To truly understand how you'll be evaluated, it's crucial to see how these factors come together to form your complete financial picture. Lenders don't look at them in isolation; they build a profile. A stronger profile earns a better rate.

The table below gives you a clear, side-by-side look at how your financial health can directly influence the VA rate you’re offered.

How Your Financial Profile Impacts Your VA Rate

FactorLower Rate Scenario (e.g., 6.25%)Higher Rate Scenario (e.g., 7.00%)Tiger Loans Pro-TipCredit ScoreExcellent (740+)Fair (640-679)Aim for a score above 720. Even small improvements can unlock significant savings.DTI RatioBelow 36%Above 43%Pay down high-interest credit cards first to quickly lower your DTI.Down Payment5% or more0%While 0% down is a key VA benefit, a down payment can reduce fees and may lower your rate.Loan Term15-Year Fixed30-Year FixedIf you can afford the higher payment, a 15-year term offers massive long-term interest savings.

As you can see, the path to a lower rate is paved with strong financial habits. A veteran with an excellent credit score above 720 and a low DTI is in a prime position to secure a rate on the low end of the current market spectrum, which has been floating between 6.25% and 7.25% for a 30-year fixed loan through 2024 and 2025. On the flip side, a borrower with a score below 620 could see a rate that's 0.125% to 0.25% higher.

For a deeper dive into improving your financial standing, check out our guide on how to secure the best interest rates for your housing loan. By focusing on these key areas, you empower yourself to achieve the homeownership dream on the best possible terms.

Choosing Your VA Refinance Strategy

If you're a veteran homeowner, don't think of your mortgage as something set in stone. It's a powerful financial tool you can adjust as your life and goals change. Refinancing can be a game-changing move, and the VA gives you two distinct paths to get it done. Figuring out which one is right for you is the key to making the most of your hard-earned benefits.

One path is all about speed and simplicity. The other is about flexibility and tapping into your home’s value. The best choice depends entirely on what you’re trying to accomplish, and it will directly shape your veterans first mortgage rates and your financial future.

The IRRRL: A "Streamline" Rate-Cutter

Your first option is the Interest Rate Reduction Refinance Loan, but almost everyone in the business just calls it an IRRRL (pronounced “Earl”). Think of the IRRRL as a quick and easy tune-up for your mortgage. It has one simple, focused mission: to lower your interest rate and, in turn, your monthly payment.

The magic of the IRRRL is just how simple it is, which is why it’s nicknamed a "Streamline" refinance. For most veterans, this means way less paperwork than when you first bought your house. You typically don't need a new appraisal, and lenders often have much lighter income verification rules. It's built to be fast, easy, and stress-free.

An IRRRL is your go-to when your only goal is to save money. If mortgage rates have dropped since you closed on your home, a Streamline is the fastest way to lock in that lower rate and start keeping more cash in your pocket every month.

The main catch? You have to be refinancing an existing VA loan into a new one. It's the perfect play for homeowners who love their home but would love their interest rate to be lower.

The Cash-Out Refinance: Tapping Into Your Home's Equity

Your second path is the VA Cash-Out Refinance. This isn't just a tune-up; it's a complete financial overhaul. With this option, you replace your existing mortgage with a new, larger loan and get to pocket the difference in cash. You’re essentially turning the equity you've worked hard to build into real, spendable money.

This move opens up a ton of possibilities. We see veterans use the cash from a refinance to tackle all sorts of important life goals:

- Wipe Out Debt: Pay off high-interest credit cards or car loans with a single, lower-interest mortgage payment.

- Fund Home Improvements: Finally get that new kitchen, fix the roof, or build the deck you've always wanted.

- Cover Education: Pay for college tuition for yourself or your kids without taking out separate student loans.

- Make Big Moves: Seize a business opportunity or make a major investment you believe in.

Because you’re pulling cash out and taking on a bigger loan, the approval process is more detailed than an IRRRL. It’s a lot like when you first bought your home—expect a full credit check, income verification, and a new appraisal to confirm your home’s current value. While the rate on a cash-out loan might be a touch higher than an IRRRL, it’s often a much smarter financial move than racking up personal loan or credit card debt.

Making the Right Choice for Your Goals

So, how do you pick a path? It all comes down to what you need to do right now. This decision will impact not just your monthly payment but your entire financial picture.

Here's a quick side-by-side to make it clear:

FeatureIRRRL (Streamline)Cash-Out RefinancePrimary GoalLower your interest rate & payment.Access your home's equity as cash.Loan AmountLimited to your existing loan balance plus some fees.A new, larger loan based on your home's current value.AppraisalUsually not required.A new appraisal is mandatory.PaperworkMinimal documentation; a "streamlined" process.Full documentation, just like a new home purchase.Typical RateTends to be the lowest available refinance rate.Slightly higher than an IRRRL or purchase rate.

If your only mission is to shrink your monthly housing costs, the IRRRL is your clear winner. But if you have bigger plans that require funding—from consolidating debt to renovating your home—the Cash-Out Refinance gives you the power and flexibility you need.

Navigating these options is much easier when you have an expert in your corner. Understanding the complete picture of VA home loan requirements is the first step, and our specialists at Tiger Loans are here to help you map out the absolute best strategy for your family and your future.

How Tiger Loans Delivers a Better Borrower Experience

Getting a great veterans first mortgage rate is a huge win, but it’s really only half the battle. The lender you choose to work with can make or break your entire home-buying experience. Let's be honest, not every lender gives VA loans the focus and expertise they deserve. That’s where you’ll feel the Tiger Loans difference.

We’re not just paper-pushers. We’re your dedicated partners, with you every step of the way on your path to homeownership. It’s about building a real relationship, one based on trust and genuine know-how.

Specialized Expertise That Actually Matters

Think about it this way: would you rather hike a tricky trail with a guide who has a generic tourist map, or one who’s walked that path a hundred times and knows every shortcut, viewpoint, and hidden pitfall? That’s the difference between a big-box lender and a true VA loan specialist. Our loan officers live and breathe the VA program.

This deep focus means we know the ins and outs of its specific rules. We spot opportunities that general lenders often overlook, which can save you a surprising amount of time, money, and stress. Our goal is simple: make this process feel straightforward and clear, not overwhelming and confusing.

We believe every veteran deserves a champion in their corner. That’s why we take the time to really get to know you—your financial picture, your family’s needs, and where you want to be in the future.

This isn’t about just getting a loan closed. It’s about giving you advice that fits you, so you feel confident and supported from the moment you apply until you’re holding the keys to your new home.

A Partnership You Can Count On

Trust is everything to us. We make it a priority to pull back the curtain on the mortgage process, explaining what’s happening in plain English. You'll never be left guessing about your loan's status or what the next step is.

We bring that same transparency to our rates and loan structures. We’ll walk you through all the moving parts so you can make smart decisions for your financial future. It’s a team effort, and that collaborative spirit is what truly sets us apart.

When you look at lender performance, you see how this commitment plays out. For instance, in 2023, data on a major VA lender, Veterans First Mortgage, showed an 89.3% approval rate. What's telling is that less than half of their approved borrowers had a DTI under 40%, and the average loan-to-value was 81.2%. This shows a lender willing to find solutions for a wide range of veteran profiles. You can explore the full LendingTree lender analysis to see how different lenders stack up.

At Tiger Loans, we share that same dedication to serving the entire veteran community.

Our Mission: Veteran Homeownership

At the end of the day, our work isn’t done just because a loan is funded. We’re passionate advocates for veteran homeownership and the financial security it builds for families. A home is so much more than four walls and a roof—it’s a foundation for your future and a legacy for your loved ones.

Choosing Tiger Loans means you’re choosing a team that honors your service. We are absolutely committed to delivering the exceptional experience and competitive rates you have earned.

Your Game Plan for Locking in the Best Possible Rate

Alright, we've covered a lot of ground. But knowing what affects your rate is one thing; actually getting a great rate is another. This is where the rubber meets the road.

Let’s turn all that knowledge into a simple, actionable game plan. Follow these steps, and you’ll walk into the application process with the confidence of a well-prepared borrower, ready to secure the most competitive veterans first mortgage rates out there.

Step 1: Get Your Paperwork in Order

First things first: let's get your documents lined up. Lenders need to see your financial picture, and having everything ready from the start makes you look organized and serious. It also dramatically speeds up the process.

The absolute must-have document is your Certificate of Eligibility (COE). This is the official proof for the lender that you've earned your VA loan benefit.

Beyond the COE, you’ll need the usual financial paperwork:

- Your most recent pay stubs (the last 30 days should do it).

- W-2 forms from the last two years.

- Your federal tax returns, also from the past two years.

- A couple of months' worth of bank statements.

Think of this as your homebuying toolkit. Having it ready to go shows you mean business.

Step 2: Know Your Credit Score—Inside and Out

Your credit score is the single biggest lever on the interest rate you'll be offered. Don't fly blind. You have the right to a free credit report every year from each of the three main bureaus: Equifax, Experian, and TransUnion.

Get those reports and go through them with a fine-tooth comb. Look for mistakes—an account that isn’t yours, a late payment that was actually on time. Finding and fixing even one small error can bump up your score, and that little bump can translate into thousands of dollars saved over the life of your loan. Seriously, don't skip this step.

Step 3: Nail Down Your Debt-to-Income Ratio

Next up is your Debt-to-Income (DTI) ratio. This is just a fancy way for lenders to measure how much of your monthly income is already spoken for by debt. To figure it out, just add up all your monthly debt payments (car loan, credit cards, etc.) and divide that number by your pre-tax monthly income.

If your DTI is inching above 41%, it's time to take action before you apply. Start by aggressively paying down any high-interest credit card debt or knocking out smaller loans. Lowering your DTI, even by a little, makes you a much more attractive borrower and can open the door to a better rate.

By taking these steps, you're no longer just a bystander waiting for a rate quote. You're actively influencing the outcome. You're showing lenders you are a responsible, low-risk borrower—and that’s how you get the best terms.

Step 4: Talk to a Tiger Loans VA Specialist

Once you’ve got your financial house in order, it's the perfect time to bring in an expert. A Tiger Loans VA specialist is more than just a loan officer; we're your guide through this entire process.

We’ll sit down with you, look at your complete financial snapshot, and lay out your options in plain, simple terms. Our team lives and breathes VA loans, and we’re deeply committed to serving the veteran community. Let us help you find the loan that truly honors your service and sets you up for a strong financial future.

Common Questions We Hear About VA Loans

Stepping into the world of home loans can feel like learning a new language. That's completely normal. To help you get comfortable and confident, we've put together answers to the questions we hear most often about VA loans and veterans first mortgage rates.

Are VA Mortgage Rates Guaranteed to Be Lower Than Conventional Rates?

It's a common belief that VA rates are always lower, but that's not the full picture. While the VA's guarantee often leads to some of the most competitive rates on the market, they aren't automatically the lowest in every single situation. A lot depends on your specific financial situation and the lender's day-to-day pricing.

But here’s where the VA loan truly flexes its financial muscle: the overall cost. The ability to purchase a home with $0 down is a game-changer. On top of that, you get to skip paying for private mortgage insurance (PMI) every single month. This alone can save you hundreds, making your total borrowing cost significantly lower, even if the interest rate is neck-and-neck with a conventional loan.

Think of it this way: the interest rate is just one piece of the puzzle. Avoiding PMI is a massive, built-in savings that keeps your monthly payment smaller for the entire life of your loan.

What if My Credit History Isn't Perfect? Can I Still Get a VA Loan?

Yes, you absolutely can. This is one of the most powerful and compassionate features of the VA loan program. The Department of Veterans Affairs itself doesn't have a hard-and-fast credit score minimum, which opens the door for so many.

Now, the private lenders who actually provide the funds, like us here at Tiger Loans, will have their own credit requirements. The great news? These are almost always more flexible and understanding than the rigid standards for conventional financing. We believe in looking at your whole story, not just a three-digit number. While a higher score will definitely help you lock in a better rate, we successfully help veterans with scores in the low-600s all the time. The most important step is simply starting an honest conversation with a VA loan specialist.

What's This VA Funding Fee I Keep Hearing About?

The VA Funding Fee is a one-time fee paid to the Department of Veterans Affairs. It’s not a lender fee; it's what keeps this incredible loan program funded for future generations of service members, veterans, and their families.

It's crucial to understand that this fee does not change your interest rate. It does, however, impact your total loan amount. Most veterans choose to roll it right into the loan balance, which is a great option because it means you don't need extra cash at closing. The exact percentage of the fee depends on a few things, like the size of your down payment (if any) and if you're a first-time or subsequent user of the benefit.

And, most importantly, veterans receiving VA disability compensation are completely exempt from paying this fee.

Ready to get clear, personalized answers to your own questions? The experienced team at Tiger Loans is ready to walk you through the entire VA loan process, step by step. Start your journey to homeownership today.

Alex Chen

Alex Chen

Get in touch with a loan officer

Our dedicated loan officers are here to guide you through every step of the home buying process, ensuring you find the perfect mortgage solution tailored to your needs.

Options

Exercising Options

Selling

Quarterly estimates

Loans

New home

Stay always updated on insightful articles and guides.

Every Monday, you'll get an article or a guide that will help you be more present, focused and productive in your work and personal life.

.png)

.png)

.png)

.avif)

.avif)

.avif)

.png)

.png)

.png)

.avif)

.png)

.png)

.avif)

.png)

.avif)

.png)

.avif)

.avif)