VA Loan Home Requirements Inspection Explained

November 19, 2025

Is a VA loan home requirements inspection mandatory? We explain the critical difference between a VA appraisal and a home inspection for your loan.

So, you're using your VA loan benefit—that’s fantastic. But there's a common point of confusion that trips up a lot of military families: the home inspection. People often ask, "Is a special VA home inspection required?" The short answer is no, but the real answer is a bit more nuanced.

What the VA actually mandates is a VA appraisal. This is completely different from a standard home inspection, and knowing the distinction is key to a smooth and successful home-buying experience.

The VA Appraisal Versus The Home Inspection

Think of it this way: the VA loan process involves two different sets of eyes looking at your potential new home. One set works for the lender and the VA to protect their investment, while the other works just for you, protecting your investment and future peace of mind.

The VA appraiser is there to do two main things. First, they make sure the house meets the VA’s Minimum Property Requirements (MPRs), which is just a way of saying it needs to be safe, sanitary, and structurally sound. Second, they determine the home's fair market value to ensure the loan amount doesn't exceed what the property is actually worth.

A private home inspector, on the other hand, is your personal detective. You hire them to go through the home with a fine-tooth comb, digging into the details and uncovering potential issues that the VA appraiser might not even look for. They’re your advocate, spotting hidden problems that could turn into major headaches and expenses later on.

Who Is Responsible For What

To be crystal clear: the VA does not require you to get a home inspection. It does require a VA appraisal for every single loan. The appraisal is a high-level check focused on broad safety issues and, of course, the property's value.

Now, here’s where things can get a little blurry. If the VA appraiser spots a significant problem—like a leaky roof, faulty wiring, or a broken HVAC system—they can flag it and require repairs before the loan can close.

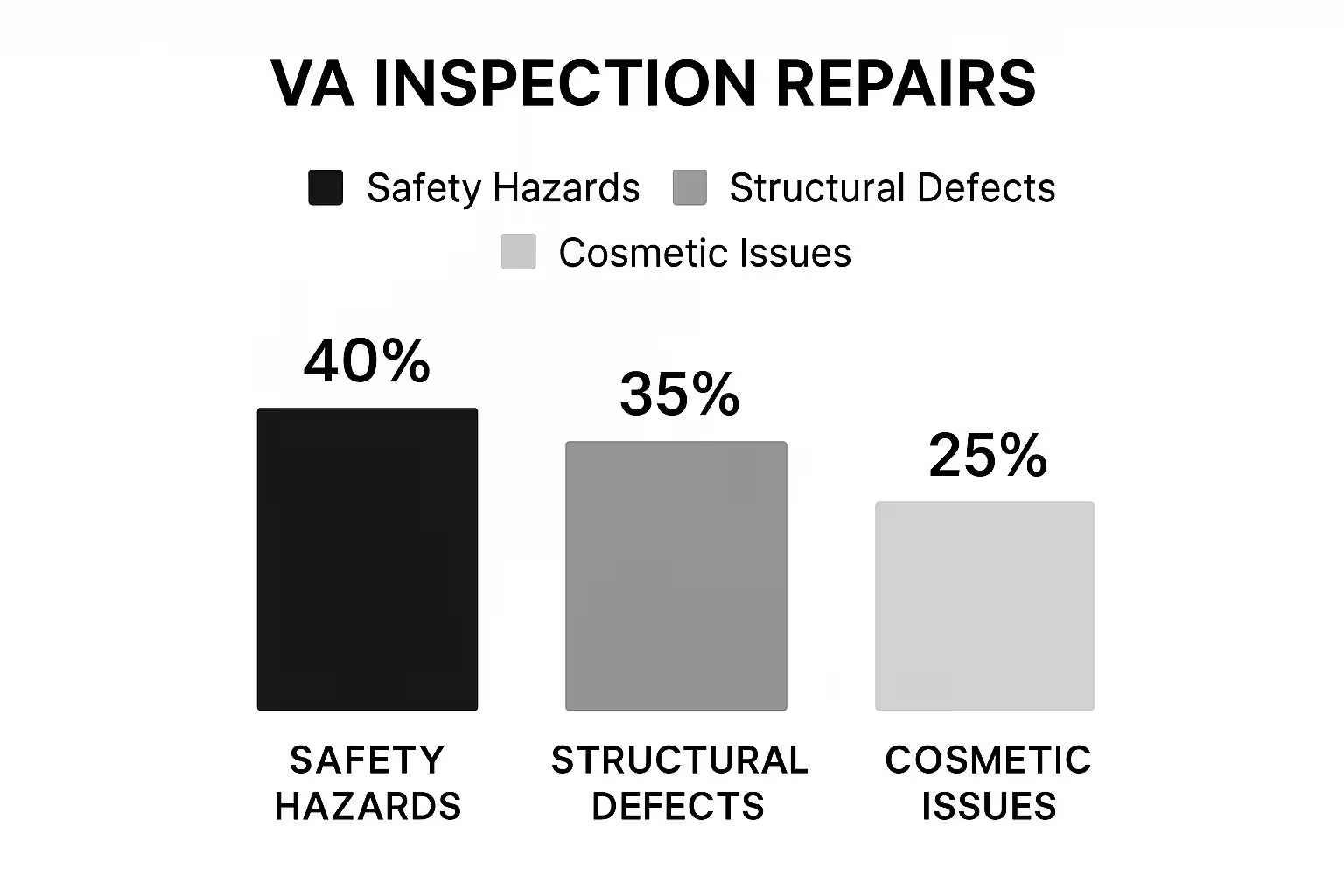

This is why it's so important to understand what appraisers focus on. Take a look at the most common issues they flag.

As you can see, their main concerns are major safety hazards (40%) and structural defects (35%). They aren't worried about scuffed paint or a cracked tile.

To help you keep these two crucial steps straight, here’s a quick breakdown.

VA Appraisal vs Home Inspection At a Glance

AttributeVA AppraisalHome InspectionPurposeTo determine fair market value and ensure the home meets VA Minimum Property Requirements (MPRs).To provide a detailed assessment of the home's overall condition, from the foundation to the roof.FocusGeneral safety, sanitation, structural soundness, and property value.In-depth analysis of all major systems: electrical, plumbing, HVAC, roofing, structure, and appliances.Who It's ForThe lender and the Department of Veterans Affairs.The homebuyer.Is it Required?Yes, always required for a VA loan.No, but highly recommended for the buyer's protection.Who Orders It?Your lender orders it through the VA's system.You, the buyer, hire an inspector of your choice.

Ultimately, both assessments play a vital role. The appraisal gets the property approved for the loan, but the inspection makes sure it’s the right home for you and your family.

The VA appraisal sets a baseline for the home’s safety and value. It is not—and was never intended to be—a substitute for a comprehensive home inspection. A private inspection gives you the detailed report you need to negotiate repairs, plan for future costs, and buy with total confidence.

Getting both done ensures you're covered from every angle. To see how these processes work together in more detail, check out our guide on understanding home inspection requirements for VA loan approval. It will give you a complete picture of the road ahead.

Decoding The VA's Minimum Property Requirements

To really get a handle on the VA appraisal, you first need to understand the VA's Minimum Property Requirements, or MPRs. Think of the MPRs as the VA’s bottom-line, non-negotiable checklist. If a home doesn't check all the boxes, it won't qualify for the loan.

The reason for this is simple: the VA wants to make sure the home you’re buying is a safe, structurally sound, and sanitary place to live. It's not about nitpicking paint colors or dated countertops. The appraiser's job is to protect both the veteran moving in and the lender backing the loan by confirming the house is fundamentally healthy.

The Three Pillars: Safe, Sound, And Sanitary

So what does "safe, sound, and sanitary" actually look like when an appraiser is walking through a property? It’s more practical than it sounds. Here’s a breakdown of what they’re trained to spot.

- Safe: The property needs to be free of anything that could pose a direct threat. We're talking about things like secure handrails on every staircase, an electrical system without sketchy, exposed wiring, and clear, safe access to and from the house, no matter the season.

- Sound: This is all about structural integrity. Is the home built on a solid foundation? The appraiser will look for big, scary cracks, a roof with plenty of life left in it, and any signs of serious water damage or rot.

- Sanitary: This covers the absolute essentials for healthy living. The home must have a dependable supply of clean drinking water, a working and sanitary sewage system, and a heating system that can keep the house at a livable temperature.

Essentially, the VA appraiser acts as the home's first line of defense, trained to see the red flags that might point to expensive, hidden problems.

The core principle behind the VA's Minimum Property Requirements is straightforward: a veteran’s home should not present any risks to their health, safety, or financial well-being. The VA is committed to ensuring the property is a secure investment from day one.

Spotting Potential MPR Issues Yourself

You don't need a clipboard and a license to develop a good eye for potential issues. As you tour homes, just keep that "safe, sound, and sanitary" mantra in your mind. It can help you screen properties and save you a lot of trouble down the line.

Look for the obvious stuff. Do you see big water stains on the ceiling? Does the basement have a musty smell that screams "mold"? Do the floors feel spongy or uneven when you walk on them?

Noticing these things can help you decide if a home is even worth making an offer on. For a much more detailed look at what an appraiser focuses on, you can get the full rundown in our guide on navigating the va loan home requirements inspection process. Catching problems early saves everyone time and stress, getting you that much closer to finding a great home that will sail through the VA appraisal.

Why a Private Home Inspection Is Your Best Ally

While the VA appraisal sets a baseline for safety and value, you shouldn't confuse it with a true home inspection. Think of the VA appraiser as a sentry at the gate, simply ensuring the property meets the minimum criteria for the loan. A private home inspector, on the other hand, is your personal detective—hired by you, working for you, and dedicated to uncovering the secrets a property might be hiding.

Their missions are worlds apart. The appraiser is checking boxes on a lender's form. The inspector is methodically pulling back the curtain to show you the home's true condition. This is your chance to look past the fresh paint and staging to see what’s really going on with the biggest investment of your life.

Going Deeper Than the Appraisal

A professional inspector’s work is vastly more thorough than the VA appraisal. They dive into the nitty-gritty details that an appraiser simply doesn't have the time or the mandate to cover. This deep dive is absolutely critical for understanding what you’re about to buy.

A comprehensive private inspection digs into the heart of the home:

- Structural Integrity: They’ll get into the crawl space, attic, and foundation, looking for signs of stress, water damage, or shoddy construction.

- Major Systems: The HVAC, plumbing, and electrical systems are all put to the test to gauge their age, performance, and the likelihood of expensive, imminent failures.

- Appliance Functionality: Every built-in appliance, from the dishwasher to the oven, is checked to make sure it’s in good working order.

- Exterior and Roofing: The inspector will look for problems with siding, drainage, and grading, and give you a solid estimate of the roof's remaining lifespan.

Ultimately, they provide you with a detailed owner's manual for your potential new home, highlighting its strengths and, more importantly, its weaknesses.

Your Most Powerful Negotiation Tool

That report you get after the inspection? It isn't just a laundry list of problems; it's your single greatest piece of negotiating leverage. Finding out the furnace is on its last legs or that there are tell-tale signs of a past plumbing leak gives you incredible power at the bargaining table.

An inspection report transforms you from a hopeful buyer into an informed investor. It provides the hard data you need to either negotiate for repairs, ask for a price reduction, or make the difficult—but wise—decision to walk away from a potential money pit.

This is a crucial part of navigating the overall va loan home requirements inspection process with confidence. Even though a private inspection isn't mandatory, it's a non-negotiable step for any savvy veteran. You can learn more about what a thorough inspection entails by reviewing these home inspection insights on QuickenLoans.com.

At the end of the day, this knowledge protects more than just your finances; it protects your family's safety and comfort in your new home. Skipping it is a gamble few can afford to take.

Common Red Flags That Can Stop a VA Loan in Its Tracks

Knowing what a VA appraiser looks for is like having the answers to the test before you walk into the classroom. It gives you the power to spot potential deal-breakers yourself, saving you the time, money, and sheer frustration of chasing a home that was never going to pass muster.

Think of it this way: when you can spot the difference between a simple cosmetic issue and a genuine roadblock, you become a much smarter home shopper. You’ll understand why peeling paint isn't just ugly or why a missing handrail is a complete non-starter. This expertise helps you zero in on homes that are actually viable contenders for your VA loan.

Most of these red flags fall into three buckets: safety hazards, structural problems, and pests.

Safety-Related Red Flags

First and foremost, the VA is looking out for the Veteran. Anything that poses a direct threat to your health and safety is going to be called out and will need to be fixed before closing. The good news is these are often the easiest issues for you to spot during a walkthrough.

A perfect example is peeling or chipping paint in any house built before 1978. This isn't a cosmetic preference; it's a serious flag for lead-based paint, which is toxic. The paint will have to be scraped, removed, and repainted. Another classic is any staircase with four or more risers that doesn't have a sturdy handrail—that's a major fall risk and an automatic repair item.

The electrical system also gets a hard look. An appraiser will immediately flag things like:

- Frayed or exposed wiring (a major fire hazard).

- Missing covers on outlets or junction boxes.

- Old, notoriously unsafe electrical panels. Federal Pacific Electric (FPE) panels, for instance, are known for their high failure rates and will almost always need to be replaced.

Structural and System Integrity Problems

Beyond immediate safety issues, the appraiser is there to confirm the house is fundamentally sound. They're making sure the home’s core systems work and that you won't be blindsided by massive, bank-breaking repairs the day after you get the keys.

Water is public enemy number one for a home's structure, so any sign of it is a huge red flag. This includes an actively leaking roof, those tell-tale water stains on a ceiling, or any dampness in the basement or crawl space. These are often symptoms of bigger problems like rot and mold that can eat away at a home's integrity.

A damp, musty smell in a basement is more than just unpleasant—it's a signal to a VA appraiser that there could be underlying moisture issues, poor drainage, or foundation problems that require professional assessment before a loan can be approved.

Other major structural deal-breakers include:

- A failing roof: If a roof is clearly at the end of its life—think curled, missing, or crumbling shingles—it's going to need attention.

- Foundation cracks: While small settling cracks are common, large horizontal cracks in the foundation are a much more serious concern.

- Wood-destroying pests: Any sign of termites, from their distinctive mud tubes on the foundation to visibly damaged wood, must be addressed. The VA loan home requirements inspection process is incredibly strict here and will typically demand a separate, official pest inspection report and proof of treatment and repairs.

Budgeting For Your Appraisal And Inspection

When you're zeroing in on a VA loan, it's natural to get caught up in the big-ticket items like the purchase price and your interest rate. But there are two other critical numbers you need to have on your radar: the VA appraisal and the private home inspection. Think of them less as costs and more as essential investments in your future home and financial well-being.

These two services are often confused, but they have very different jobs and separate price tags. Getting a handle on these expenses early on means no sticker shock later, allowing you to walk into closing with total confidence. As the buyer, you’ll typically cover both, so building them into your budget from the get-go is a smart move.

Breaking Down The Fees

The price for these assessments isn't set in stone; it can shift based on a few key things. The size and age of the house, plus where you're located, all factor into the final cost.

- Private Home Inspection: This is your chance to get a really detailed look under the hood of the property. You should plan on spending somewhere between $400 and $600, though you might pay more for a particularly large or historic home.

- VA Appraisal: This is the assessment required by the VA to confirm the home's value and ensure it meets basic safety standards. This fee usually lands in the $500 to $1,000 range, depending on the official fee schedule for your specific state.

The VA appraisal, for instance, is a non-negotiable part of the process, built to protect you and the government's investment. An appraisal in one county in California might be $1,000, while just a county over, it could be $750. You'll usually pay for this upfront or see it included in your closing costs. For a deeper dive, you can find more details about these costs and the VA loan inspection process on MilitaryMoney.com.

It can be tempting to skip the private inspection to save a few hundred bucks, but that's a gamble I'd never recommend. The cost of a thorough inspection is a drop in the bucket compared to discovering a nightmare issue—like a cracked foundation or ancient wiring—after the keys are in your hand.

By budgeting for both the appraisal and the inspection, you're arming yourself with professional insights. It's the best way to ensure you're making a sound decision that will protect your family and your investment for years to come.

Your Action Plan For A Successful Home Purchase

Buying a home can feel like a huge undertaking, but don't let the process intimidate you. When you break it down into a clear action plan, you can tackle each step with confidence, moving smoothly from that first house hunt all the way to closing day.

Your very first move? Get the right people in your corner. Find a real estate agent who truly specializes in VA loans, not just someone who's done a few. Their expertise is gold—they know the ins and outs of the va loan home requirements inspection and appraisal, and they can spot potential winners (and losers) from a mile away.

Next, hire your own home inspector. Think of this person as your personal advocate. While the VA appraisal protects the lender, your inspector works for you, giving you the unvarnished truth about the home's condition. Their report is your most powerful negotiating tool.

Turning Inspection Findings Into Action

Once that inspection report is in your hands, it’s time to sit down with your agent and map out your next move. You'll comb through every detail, separating minor cosmetic fixes from the major red flags that could impact the home's safety, structure, and value.

This detailed insight gives you real leverage and three clear paths forward:

- Request Repairs: You can present a list of issues to the seller and ask them to make the fixes before you close the deal.

- Ask for Credits: If the seller can't or won't do the repairs, you can negotiate for a credit at closing. This puts cash back in your pocket to handle the work yourself after you move in.

- Walk Away: Sometimes, the best move is no move at all. A thorough inspection gives you the confidence to walk away from a potential money pit without a second thought.

When the VA appraisal uncovers a mandatory repair—think safety hazards or structural problems—the game changes. These aren't suggestions; they're requirements for the loan to go through. This is where your agent’s negotiation skills become absolutely critical.

Finally, get ready for the appraisal. By having a solid grasp of the VA’s Minimum Property Requirements, you and your agent can spot and handle potential issues ahead of time. This proactive approach dramatically increases your chances of a smooth appraisal, putting you on the fast track to owning a safe, solid home you can be proud of.

Common Questions About VA Property Standards

Even when you know the rules, the real world of home buying can throw some curveballs. It's completely normal to have questions pop up along the way. Let's tackle a few of the most common ones we hear from veterans so you can move forward with confidence.

Can I Use a VA Loan to Buy a Fixer-Upper?

The short answer is generally no, not with a standard VA loan. The VA loan program is set up to finance homes that are safe, sound, and ready for you to move into right away. By its very nature, a "fixer-upper" needs major repairs and will almost certainly not meet the VA’s Minimum Property Requirements (MPRs).

But don't lose hope if you have your heart set on a project. A VA Renovation Loan is the perfect tool for this exact scenario. It's a special type of loan that rolls the purchase price and the cost of the necessary renovations into one single mortgage, letting you bring that diamond in the rough up to code.

What Happens if the VA Appraisal Comes in Low?

It can be a gut punch when the appraiser's valuation is lower than the price you and the seller agreed upon. When this happens, it creates a funding gap because the VA will only back a loan up to the home's appraised value. Think of it as a safety net. You've got a few solid options here:

- Go Back to the Table: Your agent can renegotiate with the seller to see if they'll lower the price to match the appraisal. It often works.

- Cover the Difference: If you have the cash, you can choose to pay the difference between the sales price and the appraised value yourself at closing.

- Walk Away: This is where an appraisal contingency in your contract becomes your best friend. It allows you to cancel the deal and get your earnest money deposit back without penalty.

Does the Seller Have to Make the Required Repairs?

Legally, the seller isn't required to fix anything. But here’s the reality: if they want to sell their home to you using your VA loan, those repairs identified by the appraiser must be completed before the loan can close.

This becomes a key negotiation point. A seller's refusal to make repairs means the deal, as it stands, is dead. Your real estate agent is your champion here, helping you persuade the seller, explore other ways to cover the repair costs, or decide if it's time to find a property that's a better fit.

For a deeper dive into everything the VA looks for in a home, our VA home loan requirements guide has you covered from top to bottom.

At Tiger Loans Inc, we specialize in helping veterans navigate every step of the VA loan process with clarity and confidence. Let us guide you home.

Alex Chen

Alex Chen

Get in touch with a loan officer

Our dedicated loan officers are here to guide you through every step of the home buying process, ensuring you find the perfect mortgage solution tailored to your needs.

Options

Exercising Options

Selling

Quarterly estimates

Loans

New home

Stay always updated on insightful articles and guides.

Every Monday, you'll get an article or a guide that will help you be more present, focused and productive in your work and personal life.

.png)

.png)

.png)

.avif)

.avif)

.avif)

.png)

.png)

.png)

.avif)

.png)

.png)

.avif)

.png)

.avif)

.png)

.avif)

.avif)